How to Teach Kids About Money by Age

Financial habits are largely established by age seven, meaning parents must move beyond simply teaching mathematics and focus on building executive function and behavioral norms. By matching financial concepts - from physical coin counting in early childhood to navigating digital microtransactions in adolescence - with a child's cognitive developmental stage, parents can bridge the significant gap between theoretical financial knowledge and real-world financial behavior.

The Developmental Science of Financial Capability

For decades, financial education was treated as a purely mathematical endeavor. The prevailing assumption was that if a child understood addition, subtraction, fractions, and percentages, they were by definition financially literate. However, modern developmental cognitive psychology reveals a far more complex reality. Financial capability is less about mathematics and significantly more about behavioral psychology, impulse control, and executive function 12.

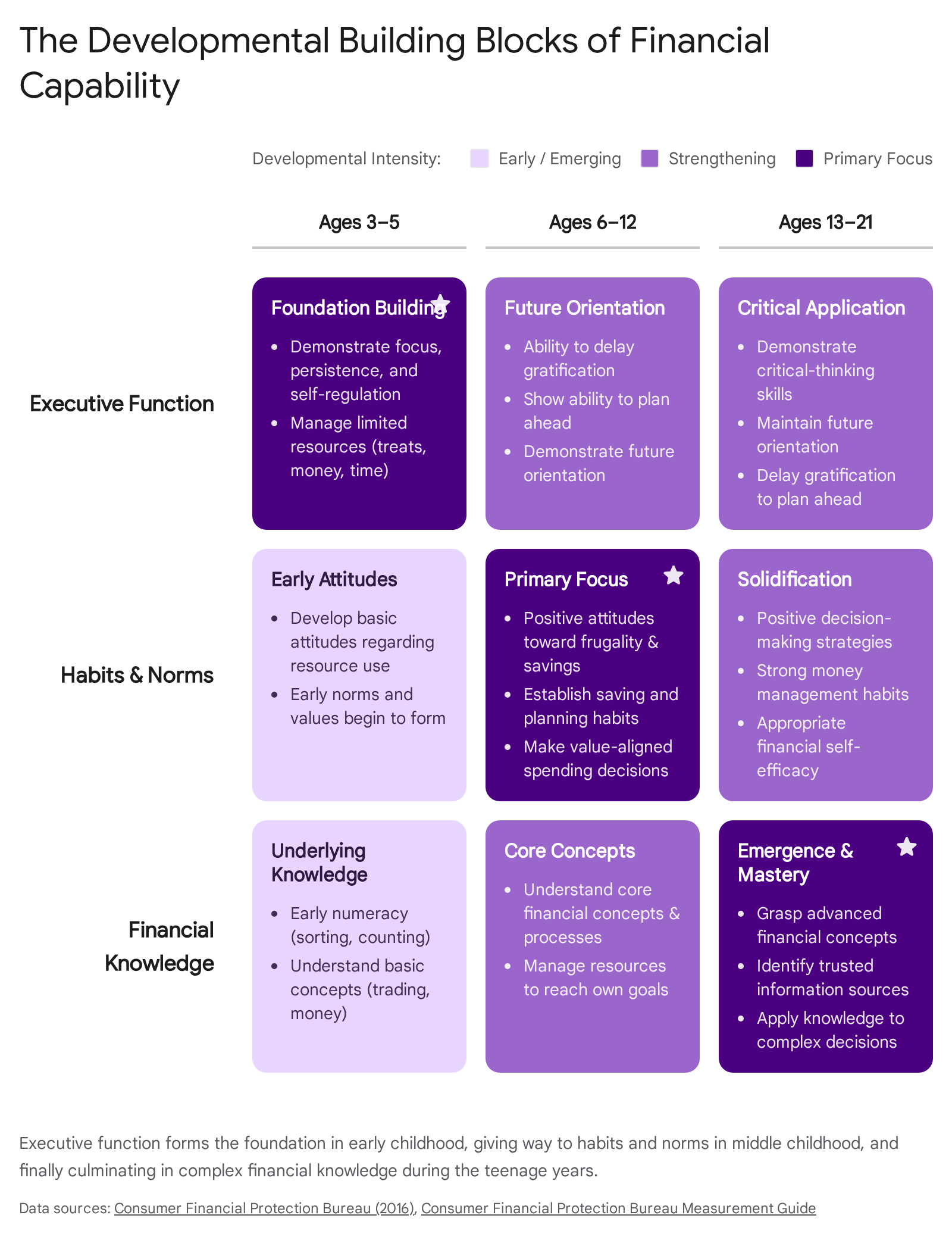

According to a pivotal study commissioned by the University of Cambridge and the Money Advice Service, the core "habits of mind" that influence how children approach complex problems and financial decisions are largely determined in the first few years of life 3. The researchers concluded that simply imparting factual information to young children is highly ineffective for long-term behavioral change. Instead, human financial capability rests on three interlocking developmental building blocks that emerge sequentially as a child's brain matures 14.

The first and most critical building block is executive function, which develops significantly during early childhood and continues to refine itself into young adulthood. Executive function acts as the brain's air traffic controller. It encompasses working memory, the ability to manage mental distractions, and, crucially for financial health, the capacity for self-regulation and delayed gratification 15. Without a robust executive function, an individual cannot adhere to a long-term budget, regardless of how well they understand the underlying arithmetic. A child must be able to hold a future goal in their mind while suppressing the immediate urge for a present reward 15.

The second building block consists of financial habits and norms, which primarily develop during middle childhood, although the foundational values begin taking shape much earlier. These are the automatic mental shortcuts, rules of thumb, and culturally absorbed values regarding consumption, saving, and the sharing of resources 14. Because the brain relies on heuristics to reduce cognitive load, establishing healthy financial defaults - such as automatically saving a portion of any received money - creates a behavioral safety net that protects an individual when active willpower is depleted.

The final building block is financial knowledge and decision-making skills. This block typically does not emerge fully until adolescence and young adulthood. It involves understanding complex, abstract concepts such as compound interest, credit utilization ratios, taxation, and the accurate comparison of multi-featured financial products 14. This stage requires advanced critical thinking and the ability to evaluate the reliability of various information sources before committing to a financial decision 6.

To teach children about money effectively, parents and educators must align their pedagogical methods with the child's specific stage of cognitive development. The theories of Jean Piaget, a pioneering developmental psychologist, provide an essential roadmap here. Piaget demonstrated that children's brains do not merely possess less information than adult brains; they operate using fundamentally different logic structures 78. A preschooler cannot conceptualize a retirement account or an inflation rate, but they can conceptualize the effort required to wait for a larger reward. Therefore, financial education must evolve in tandem with a child's neurological maturation.

Early Childhood (Ages 3 to 5): Making the Invisible Tangible

During Piaget's preoperational stage, which spans roughly from ages two to seven, children begin using symbols and language but continue to struggle with pure logic and abstract thought 78. They are highly egocentric, meaning they find it difficult to view situations from the perspective of others, and they interpret the world entirely through immediate, tangible experiences 79.

Because money is inherently an abstract representation of value, it is notoriously difficult for a preoperational mind to grasp. This challenge has been severely exacerbated by the rapid transition to a cashless society. To a preschooler, modern commerce appears to be invisible magic. They watch a parent tap a piece of plastic or a smartphone against a terminal, and groceries, toys, or experiences magically appear 101112. They do not witness a corresponding decrease in resources; they do not see a wallet becoming thinner or feel the weight of coins being exchanged. Without the tactile feedback that historically taught financial basics automatically, children can easily develop the misconception that digital money is an unlimited resource 1013.

At this developmental stage, the goal is not to teach structured budgeting, but to build executive function, basic numerical recognition, and the understanding that resources are finite 11210. Parents must actively work to make the invisible tangible again.

The primary pedagogical tool for this age group is the clear jar method. While traditional ceramic piggy banks have nostalgic value, they hide the money from view, rendering the act of saving invisible. A transparent container allows a child to see the physical accumulation of coins and bills, helping them understand that saving is an active, growing process 111213. When a child deposits a coin, they receive immediate visual feedback. Over weeks, they can witness the volume of their savings increase, connecting their patience with a tangible result.

Furthermore, everyday errands must be transformed into teachable moments through a process of "thinking out loud." Because children in the preoperational stage learn heavily through observation and modeling, parents should vocalize their internal financial monologues 10. When navigating a grocery store, a parent might explain, "We are buying this bread because we need it to make sandwiches for lunch, but we are leaving this expensive cereal on the shelf because it is a want, not a need, and it costs too much today" 111314. This ongoing narration helps the child build mental categories for necessities versus luxuries.

To teach the concept of opportunity cost and scarcity, parents can utilize two-item choice exercises. Giving a preschooler a small amount of physical cash - such as two dollars - and allowing them to choose between two different snacks forces them to evaluate trade-offs 1210. They learn quickly that selecting one item means sacrificing the other. When the physical money is handed over to the cashier, it is permanently gone, reinforcing the reality that resources are limited and choices have permanent consequences.

| Financial Concept | Traditional Approach | Modern Tangible Approach for Preoperational Minds |

|---|---|---|

| Saving | Ceramic piggy bank (hidden progress). | Transparent jars where volume accumulation is visible daily. |

| Spending | Parent hands over an invisible credit card. | Child hands over physical coins to a cashier for a small item. |

| Scarcity | Saying "We cannot afford that." | Offering a strict two-item choice with a fixed physical budget. |

| Value | Explaining prices conceptually. | Sorting physical coins by size, color, and eventual numerical worth. |

Middle Childhood (Ages 6 to 12): Norms, Habits, and the Allowance Debate

Between the ages of seven and eleven, children transition into Piaget's concrete operational stage. Their cognitive abilities undergo a profound shift. They become significantly more logical, they begin to understand the concept of conservation (the idea that a quantity remains the same despite changes in its physical appearance), and they develop the ability to mentally reverse actions 78. They also become less egocentric, developing a heightened concern for justice, fairness, and rules-based systems 15.

This is the optimal developmental window to introduce structural financial habits, future orientation, and positive attitudes toward frugality 14. At this stage, children are capable of planning ahead and delaying gratification for larger rewards. They can place events in a time sequence, allowing them to comprehend the concept of saving for a goal that is weeks or even months away 1516.

To bridge the gap between effort and reward, many families introduce an allowance during middle childhood. However, the academic and psychological literature reveals significant debate regarding how an allowance should be structured. The methodology a parent chooses directly dictates the underlying financial lesson the child internalizes. If structured poorly, an allowance can foster financial dependence rather than financial capability 17.

| Allowance Structure | Implementation Method | Primary Behavioral Lesson | Identified Vulnerabilities |

|---|---|---|---|

| Strictly Chore-Based | Funds are paid solely upon the completion of specific, itemized tasks (e.g., a piece-rate system). | Reinforces the direct, causal link between labor, effort, and income generation. | Children may refuse to participate in basic household duties if they decide they do not currently "need" money. |

| Unconditional Fixed | A set amount is provided weekly or monthly, independent of household contributions. | Money serves primarily as a pedagogical tool to practice budgeting, saving, and managing a reliable cash flow. | Fails to teach the reality of earning an income through labor; may breed entitlement or reliance on external support. |

| The Hybrid Model | A small baseline amount is provided for learning, while significant funds require the completion of extra, non-routine labor. | Balances the need for guaranteed practice capital with the vital lesson that extra effort yields extra reward. | Requires meticulous tracking, consistency, and ongoing negotiation from parents, increasing household cognitive load. |

Regardless of the chosen allowance model, financial researchers highly recommend pairing the income with a structured allocation system. The most prominent of these is the "Three-Jar System," which requires the child to divide all incoming funds into distinct categories: Spend, Save, and Share (or Grow) 11121318.

This physical and mental separation forces the child to allocate funds intentionally rather than impulsively. The "Spend" jar provides autonomy and the freedom to make minor mistakes with immediate consequences. The "Save" jar introduces the discipline of delayed gratification, often tracked via a visual chart on the refrigerator to maintain motivation 1223. The "Share" jar connects financial resources to empathy and community support, aligning with the concrete operational child's developing sense of social justice 1115. By establishing this triage process early, parents hardwire a budgeting heuristic into the child's brain, making the division of resources an automatic habit long before they encounter adult tax brackets or retirement contributions.

Navigating Fictional Economics in the Digital Age

As children transition into late elementary and middle school, they face a financial environment entirely alien to previous generations. They are no longer simply managing physical coins in jars; they are navigating sophisticated, highly optimized digital economies. This phenomenon, often referred to as "fictional economics," encompasses the complex systems of exchange within digital worlds, mobile applications, and video games 24.

The gaming industry, in particular, has engineered digital environments that systematically abstract the value of real-world money, creating psychological friction that encourages continuous spending 192620. A 2025 study commissioned by the UK regulator Ofcom revealed that 32% of children regret the money they spent playing games online, highlighting a pattern of design strategies that deliberately exploit the developing cognitive vulnerabilities of youth 19.

Understanding the architecture of these digital economies is essential for modern financial socialization.

Developers utilize several interlocking persuasive design tactics:

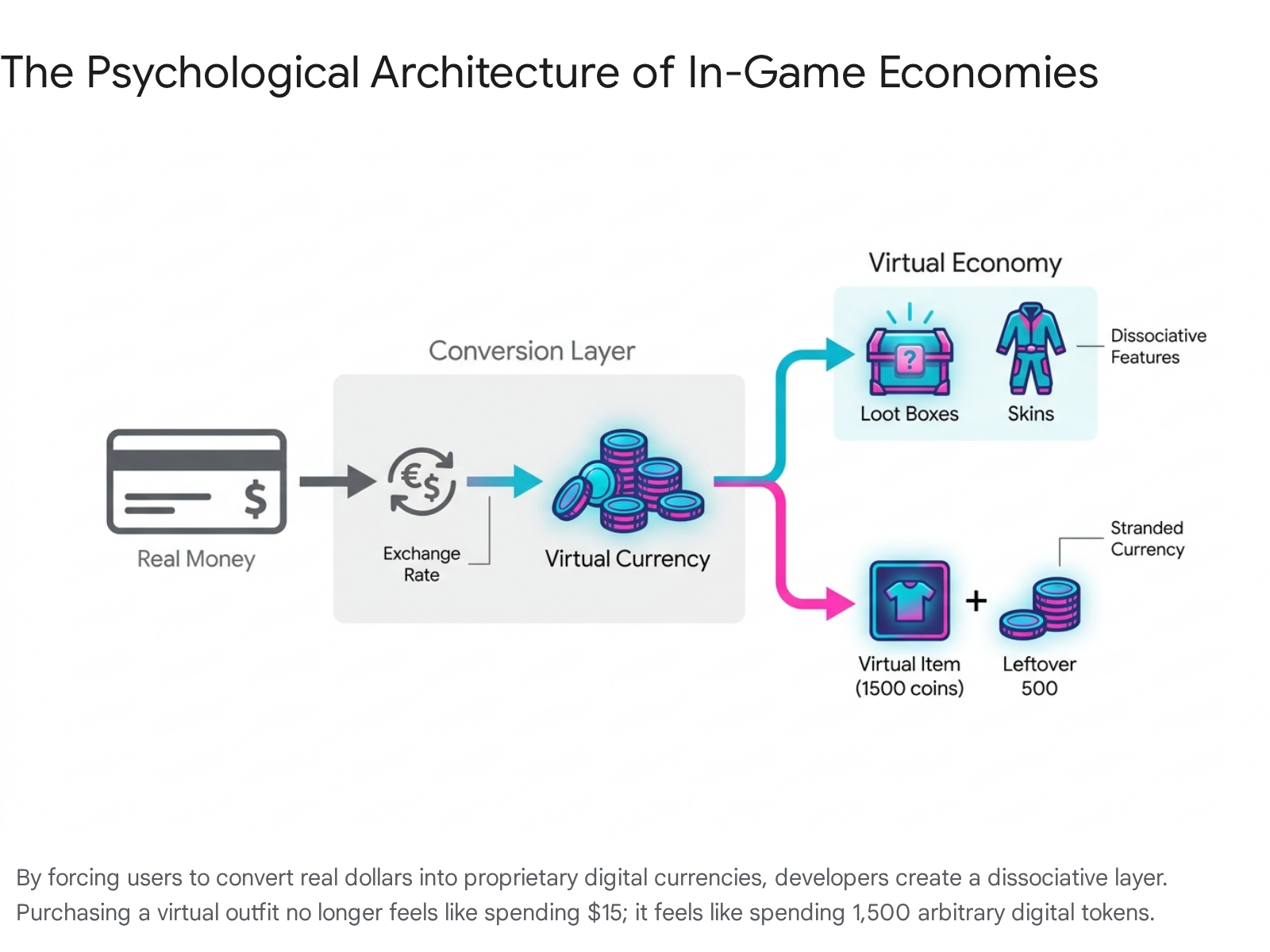

The most foundational tactic is the implementation of dissociative features. Games rarely allow players to purchase items directly with fiat currency (e.g., US Dollars or Euros). Instead, players must use real money to purchase "Hard Currency" - proprietary digital tokens such as V-Bucks, Robux, or FC Coins 2426. This creates a powerful psychological disconnect. When a child contemplates buying a digital cosmetic item (a "skin"), they are not evaluating a $15 purchase; they are evaluating a 1,500-token purchase. Because the digital tokens have no real-world equivalent, the brain's natural loss aversion is circumvented 192621.

Furthermore, developers masterfully employ stranded currency through psychological pricing. A highly desired in-game item might cost 1,200 digital tokens, but the developer will only sell tokens in fixed bundles of 1,000 or 2,800 24. If the child wishes to acquire the item, they are forced to purchase the 2,800-token bundle. After the transaction, they are left with a remainder of 1,600 stranded tokens. This remainder makes the child feel artificially wealthy, yet they still lack enough tokens to purchase the next premium item, which inevitably costs 2,000 tokens. This deliberate mathematical mismatch creates a perpetual, frustrating cycle that necessitates continuous real-world spending to "clear out" the balance 24.

The most controversial of these mechanics is the loot box, a virtual container that can be purchased with real or in-game money. Upon opening a loot box, the player receives a randomized assortment of virtual items 2022. Because the outcome is unknown until after the purchase is finalized, loot boxes rely on a variable-ratio reinforcement schedule - the exact psychological mechanism utilized by slot machines. Both parents and regulatory bodies have likened loot boxes to unregulated gambling, as they prey on impulsive features and risk-based tactics to exploit children's developing cognition 192022. Research indicates that these mechanics make it incredibly difficult for young players to track their actual spending, often leading to severe financial regret 1922.

To counter these sophisticated psychological traps, parents must actively reconstruct the friction that fictional economies seek to eliminate. This requires shifting from a "Magic Money Phase," where children view the digital purchase button as an infinite resource, to a highly regulated "Digital Allowance" phase 24.

Parents should consider utilizing digital banking applications designed specifically for families, such as BusyKid or Greenlight, which allow children to interface with digital money in a controlled environment while tracking their balances visually 132130. When dealing specifically with in-game purchases, parents must enforce the "Real Bucks Conversion" 24. If a teenager desires a $20 digital enhancement, the parent should mandate an explicit calculation: how many hours of household chores, babysitting, or neighborhood labor are required to generate that exact dollar amount? By anchoring the abstract digital token to the physical reality of human labor, children regain the capacity to accurately evaluate the true cost of their virtual consumption 2426.

Adolescence (Ages 13 to 18): Abstract Reasoning and Complex Systems

As children mature into teenagers, they enter Piaget's formal operational stage. At this juncture, the brain develops the capacity to think abstractly, reason systematically, and solve hypothetical problems 78. Teenagers can conceptualize the future with greater clarity, making it the critical window to introduce complex financial instruments, the time value of money, and the severe consequences of debt 46.

At this stage, financial socialization must pivot from basic saving habits to comprehensive wealth management and risk assessment. Two concepts are paramount during these years: compound interest and credit utilization.

Demystifying Compound Interest

To a teenager focused on impending social events and academic pressures, the concept of saving for retirement decades in the future feels entirely abstract and largely irrelevant. To capture their attention, financial educators and parents must rely on the mathematical marvel of compound interest.

Compound interest is the process of earning interest on both the principal amount of an investment and the accumulated interest from previous periods 233233. It acts as a financial snowball rolling downhill - starting small but gathering mass at an exponential rate 32.

Because the adolescent brain often struggles with long-term future orientation, abstract explanations are insufficient. Parents must provide concrete, mathematical scenarios demonstrating the "Ten-Year Head Start." For instance, a common pedagogical analogy asks the teenager to imagine investing $100 annually at an 8% return. In the first year, the investment yields a modest $8. However, if the funds remain untouched, the compounding effect accelerates. Because compounding rewards the duration of time exponentially more than the initial principal, a teenager who begins saving small amounts at age 16 will almost always mathematically outperform an individual who begins saving vastly larger amounts at age 35 233234.

Teaching this principle early neutralizes the common misconception that substantial wealth requires a massive initial deposit. It proves to the teenager that consistency and time are their most valuable financial assets.

Consumer Debt and the Credit Card Transition

Conversely, teenagers must be thoroughly educated on how compound interest operates against them in the form of consumer debt. Aggressive marketing by credit card companies often portrays credit access as an extension of income. Without direct intervention, teenagers frequently assume a credit card functions similarly to a debit card, failing to grasp the compounding penalties associated with revolving balances 2425.

Financial socialization must explicitly clarify the mechanics of borrowing. A credit card is not free money; it represents an immediate, high-interest loan from a financial institution 253738. Teenagers must be shown the brutal mathematics of revolving debt. For example, if an individual carries a $5,000 credit card balance at a 16% interest rate and pays only the 2% minimum monthly requirement, the interest accrued will actively outpace the principal reduction. The borrower will remain in debt for years, ultimately paying thousands of dollars in interest charges for a relatively minor initial purchase 33.

Furthermore, adolescents must learn to distinguish between the nature of different liabilities.

| Debt Category | Characteristics | Examples | Financial Implication |

|---|---|---|---|

| "Good" (Investment) Debt | Funds used to acquire assets that have the potential to appreciate in value or significantly increase future earning capacity. | Reasonable student loans, a residential mortgage, business capitalization loans. | Can be a strategic tool for building long-term wealth if interest rates are favorable and risk is managed 243739. |

| "Bad" (Consumer) Debt | High-interest funds utilized to purchase consumable, rapidly depreciating goods or to fund a lifestyle beyond current income levels. | Credit card balances carried month-to-month, payday loans, high-interest auto loans. | Actively destroys wealth through compounding interest; restricts future cash flow and damages credit scores 243739. |

To safely introduce teenagers to credit, parents can employ supervised practice. Adding a teenager as an authorized user on a well-managed parental credit card, or opening a low-limit secured credit card requiring a cash deposit, allows the adolescent to practice building a credit history 2526. By requiring the teenager to pay off small, predictable expenses (such as a streaming subscription or gasoline) in full every month, they internalize the rhythm of responsible credit utilization before they are exposed to the risks of independent adult borrowing 3826.

Cross-Cultural Variances in Financial Socialization

While discussions of compound interest and credit scores dominate Western financial literature, it is crucial to recognize that financial socialization is not a universal, context-free monolith. The values, mechanisms, and goals of financial education vary drastically across global cultures, socioeconomic strata, and historical contexts 2728.

The predominant Western model of financial education is heavily anchored in individualism. It emphasizes personal autonomy, the accumulation of individual wealth, the management of personal credit scores, and the financial independence of the nuclear family. However, non-Western cultures frequently approach financial socialization through a fundamentally different lens - one of interdependence, collective security, and distinct systemic trajectories 28.

A profound example is found in the divergent human capital accumulation strategies of China and India over the 20th century. Historical analysis reveals that colonial India's education system prioritized the humanities to fulfill administrative needs, and post-colonial India largely neglected mass compulsory primary education in favor of elite tertiary education 29. This systemic choice left a massive portion of the Indian population reliant on the informal, rural economy, deeply influencing how financial survival skills were transmitted across generations 2930. In stark contrast, China adopted a bottom-up approach, prioritizing mass primary education early on, and later pivoting to expansive vocational training. Nearly 25% of Chinese students at the secondary level are enrolled in vocational education, compared to roughly 2% in India, aligning the population's socialization directly with the state's goals of rapid manufacturing growth 29.

On a familial level, cultural norms dictate vastly different approaches to resource allocation. In many Asian, African, and Latin American contexts - particularly where robust state-sponsored social safety nets or widespread institutional retirement accounts may be weak or non-existent - parents are essentially required to educate their children to save and plan for communal, intergenerational financial security rather than sheer individual accumulation 2731.

A recent qualitative study examining families in Indonesia illuminated how financial socialization is deeply intertwined with religious and cultural norms 4748. Rather than focusing strictly on personal enrichment, these families emphasized the concept of sharing and charitable giving as core pillars of a healthy budget. The financial lessons passed from parent to child were designed to foster collective family well-being and community resilience 47.

Even the basic concept of the "allowance" is subjected to intense cultural scrutiny. While Western pedagogy often champions the fixed weekly allowance to teach budgeting, researchers studying diverse socioeconomic groups argue that automatic allowances can inadvertently breed financial dependence 1732. In many global households, providing children with "money on request" - where funds are distributed only after rigorous negotiation, justification, and discussion between parent and child - is preferred. The rationale is that the friction of the dialogue itself is the primary socializing agent, forcing the child to articulate their needs, defend their choices, and engage actively with the family's broader economic reality 174733.

Similarly, research utilizing the Family Financial Socialization Theory highlights structural differences in how young adults perceive parental support. A comparative study of Asian American and international Asian college students found that while both groups rely heavily on parental financial socialization, international students often operate under a paradigm where full parental financial support for education is a pre-established norm, altering how they navigate debt and budgeting compared to their American-raised peers who face high student loan pressures 3435.

Ultimately, effective financial education cannot be imported wholesale without considering the cultural and socioeconomic realities of the household. An effective curriculum must be adaptable, acknowledging that the definition of financial success varies from maximizing an individual investment portfolio to ensuring the economic stability of a multi-generational family unit 2747.

Evaluating Efficacy: School Curriculums Versus the Home Environment

For the past two decades, policymakers, economists, and educators have championed mandatory personal finance courses in high schools as the panacea for societal debt and poor saving habits. Millions of dollars have been allocated to integrate financial literacy into standard curriculums. But as this movement matures, a critical question remains: does formal financial education actually work?

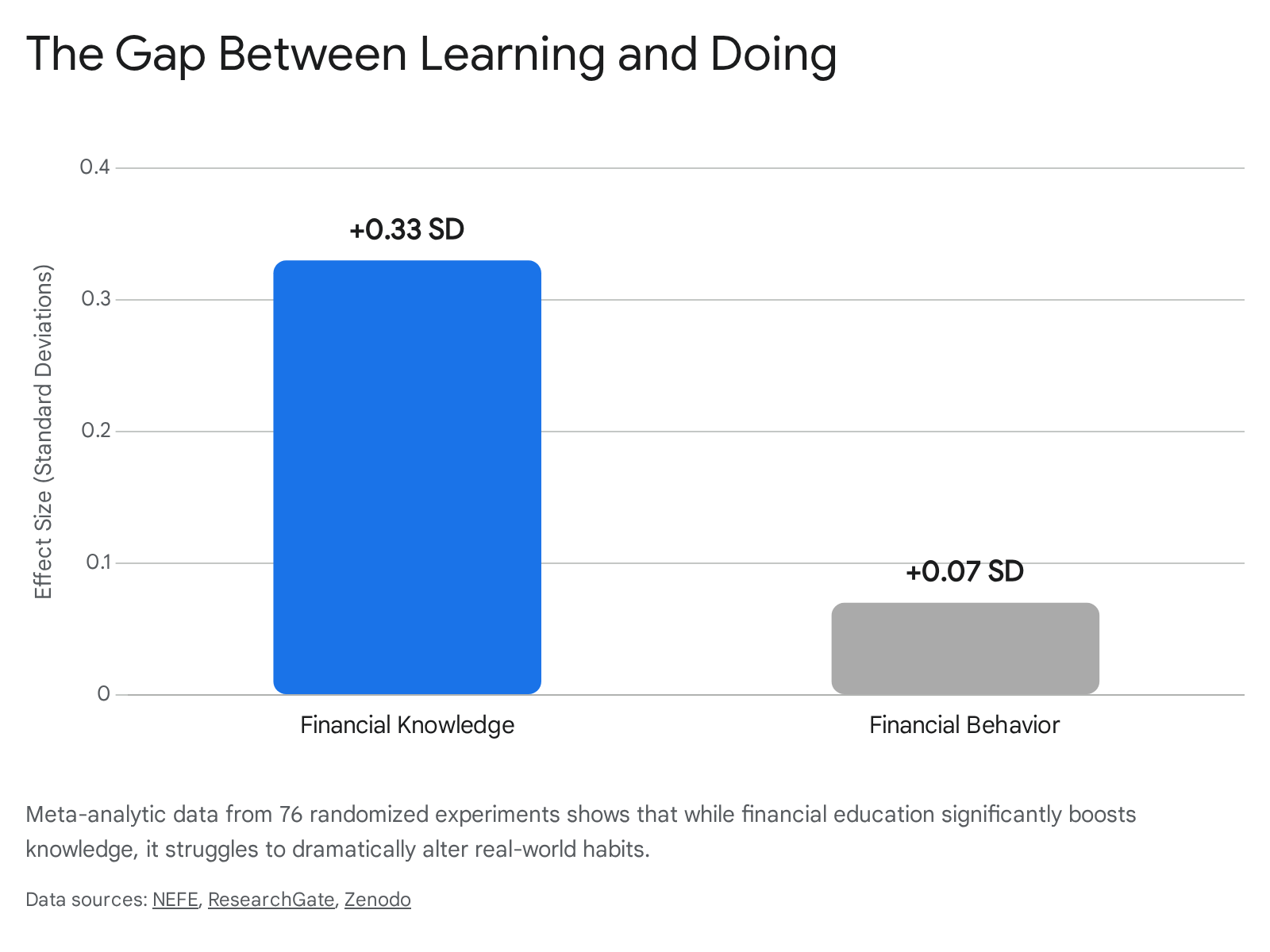

To answer this, researchers conducted a massive, comprehensive meta-analysis in 2024, examining 76 randomized experimental studies spanning 33 countries and covering over 160,000 individuals 365437. The aggregated data revealed a chronic, fascinating paradox in the field of financial education.

The data unequivocally proves that school-based financial literacy programs consistently and effectively improve financial knowledge. The meta-analytic evidence demonstrates large, statistically significant gains in student understanding, reflecting an effect size of +0.33 standard deviations. To put this in perspective, an impact of this magnitude is entirely comparable to the effect sizes seen in highly successful, traditional mathematics and reading interventions 365438. When tested on vocabulary, inflation mechanics, and compound interest calculations, students who undergo financial education perform vastly better than those who do not.

However, the paradox emerges when researchers attempt to measure how that classroom knowledge translates into actual behavioral change. The impact of financial education on real-world financial behavior - such as increasing monthly savings rates, delaying gratification, or avoiding high-interest debt - is drastically smaller, registering a meager effect size of just +0.07 standard deviations 543839.

This stark discrepancy highlights the fundamental flaw in treating financial capability as an academic subject rather than a behavioral discipline. Knowing how a budget works mathematically on a whiteboard does not endow a teenager with the neurological impulse control required to resist intense social pressure to purchase a luxury item. Factual knowledge is easily overridden by emotion, peer influence, and the persuasive design of modern retail environments 5440.

The Experiential Learning Imperative

To bridge this massive gap between theoretical knowledge and practical execution, financial learning must move beyond the textbook and become highly experiential 414243.

The most successful institutional interventions are those that simulate reality. Programs such as Junior Achievement's BizTown or "My Classroom Economy" (MCE) immerse students in simulated, risk-free micro-economies 414344. In these environments, students apply for jobs, receive mock salaries, pay taxes, rent their physical classroom desks, and manage digital bank accounts over an extended period. These experiential simulations consistently yield positive, lasting changes in student attitudes, self-efficacy, and behavioral retention because they force children to experience the actual emotional friction of parting with resources 414344. Interestingly, researchers note that programs like MCE not only boost financial literacy but also demonstrate positive spillover effects into standard math and social studies comprehension 41.

Yet, despite the innovations in school-based simulations, the most potent experiential learning environment remains the home.

The Family Financial Socialization Theory posits that the family unit is the ultimate crucible for financial behavior 3334. Parents shape their children's financial futures through both purposive socialization (direct instruction, assigning chores, reviewing bank statements) and unintentional socialization (the child observing the parent arguing about bills, impulse shopping, or utilizing credit cards) 273345.

Studies confirm that teenagers who engage in open communication with their parents about money, and who generate their own earned income during high school, exhibit significantly higher financial confidence and make healthier financial decisions in emerging adulthood 323345. Ultimately, parents who intentionally construct scenarios where children earn money, track expenses, and, most importantly, face the natural consequences of poor financial choices within a safe environment are the true architects of their children's financial capability.

Bottom line

The foundation of a child's financial capability is built long before they receive their first paycheck; it begins in early childhood through the development of executive function, patience, and impulse control. While school-based programs are highly effective at teaching the mathematical facts of personal finance, extensive meta-analytic data shows they struggle to instill lasting behavioral changes without hands-on, experiential practice. Parents remain the ultimate financial educators, and their most critical task today is to make the "invisible money" of our digital, gamified economy tangible again through open conversation, structured resource allocation, and practical experience.