Fintech disruption of incumbent banks from the low end

Executive Summary

- Financial technology (fintech) firms initially captured market share through low-end disruption, targeting unbanked or underbanked consumers with low-cost digital offerings that legacy institutions deemed unprofitable.

- The macroeconomic shift from the Zero Interest Rate Policy (ZIRP) era to the high-interest-rate environment of 2023 - 2024 has fundamentally altered fintech incentives, replacing a "growth at all costs" mandate with a strict requirement for sustainable profitability.

- In contrast to Western markets, Asian economies demonstrate extensive technological leapfrogging, where state-sponsored public infrastructure and private super-app ecosystems have entirely bypassed legacy banking networks.

- A pervasive misconception assumes digital financial interfaces operate as autonomous banks; in reality, most rely heavily on legacy sponsor banks, a dependency that has triggered severe regulatory crackdowns in 2023 and 2024.

- Fintechs currently face mounting structural headwinds, primarily driven by surging customer acquisition costs (CAC) due to digital channel saturation, alongside increasingly burdensome anti-money laundering (AML) and consumer protection compliance requirements.

The landscape of financial services is undergoing a structural transformation driven by digitalization, shifting macroeconomic policies, and evolving regulatory frameworks. While early narratives positioned financial technology startups as existential threats to incumbent banks, the reality is far more complex, characterized by symbiotic partnerships, geographic divergence, and stringent economic realities. This report examines the mechanics of disruptive innovation within financial services. It explores the foundational theories of low-end market entry, the varying regional trajectories of technological leapfrogging, the fragile operational realities of Banking-as-a-Service (BaaS) models, and the compounding headwinds of customer acquisition and regulatory compliance in a post-ZIRP economy.

Theoretical Foundations of Disruption

Low-End and New-Market Disruption

The conceptual framework for analyzing how new entrants challenge incumbent financial institutions is anchored in Clayton Christensen's theory of disruptive innovation. Christensen articulated that disruption is not merely an improvement in technology, but a specific process by which a product or service initially takes root in simple applications at the bottom of a market 112. Disruptive innovations expand markets by offering cheaper, more accessible, and often technologically simpler alternatives to over-served or unserved populations 24.

In the context of financial services, low-end disruption occurs when a fintech company introduces a streamlined product - such as a fee-free digital checking account or basic peer-to-peer (P2P) payment wallet - that meets the needs of lower-income or younger demographics. Incumbent banks, trapped in the "Innovator's Dilemma," logically choose not to defend this low-margin territory 43. Because traditional banks are burdened by the high fixed costs of physical branch networks and legacy core systems, they must focus on their highest-margin customers to satisfy shareholder demands for return on equity 44. Consequently, established banks voluntarily cede the low end of the market to fintechs, assuming the new entrants pose no threat to their core profit pools of corporate lending and wealth management.

Alternative Frameworks and Sustaining Innovation

While the disruption narrative dominates industry discourse, a comprehensive theoretical lens reveals that fintech often acts as a sustaining innovation or an enabler for traditional financial institutions, rather than a purely destructive force. Sustaining innovations improve the performance of existing products along the dimensions that mainstream customers historically value 24.

Many fintechs operate through embedded finance, open banking, and white-label Banking-as-a-Service (BaaS) platforms, which integrate financial services directly into non-financial digital ecosystems 756. These technologies function as enabling infrastructure. For example, Application Programming Interface (API) gateways and data normalization layers allow traditional institutions to outsource the expensive and rapid development of modern user interfaces 610. By absorbing fintech capabilities for backend efficiency - such as automated credit scoring and digital onboarding - legacy banks engage in "defensive digitization," maintaining their pricing power and leveraging their exclusive deposit-taking licenses to cement their dominance 47. In this framework, fintechs are not replacing banks; they are serving as outsourced research and development arms that ultimately sustain the incumbent system.

The Neobank Upmarket Trajectory

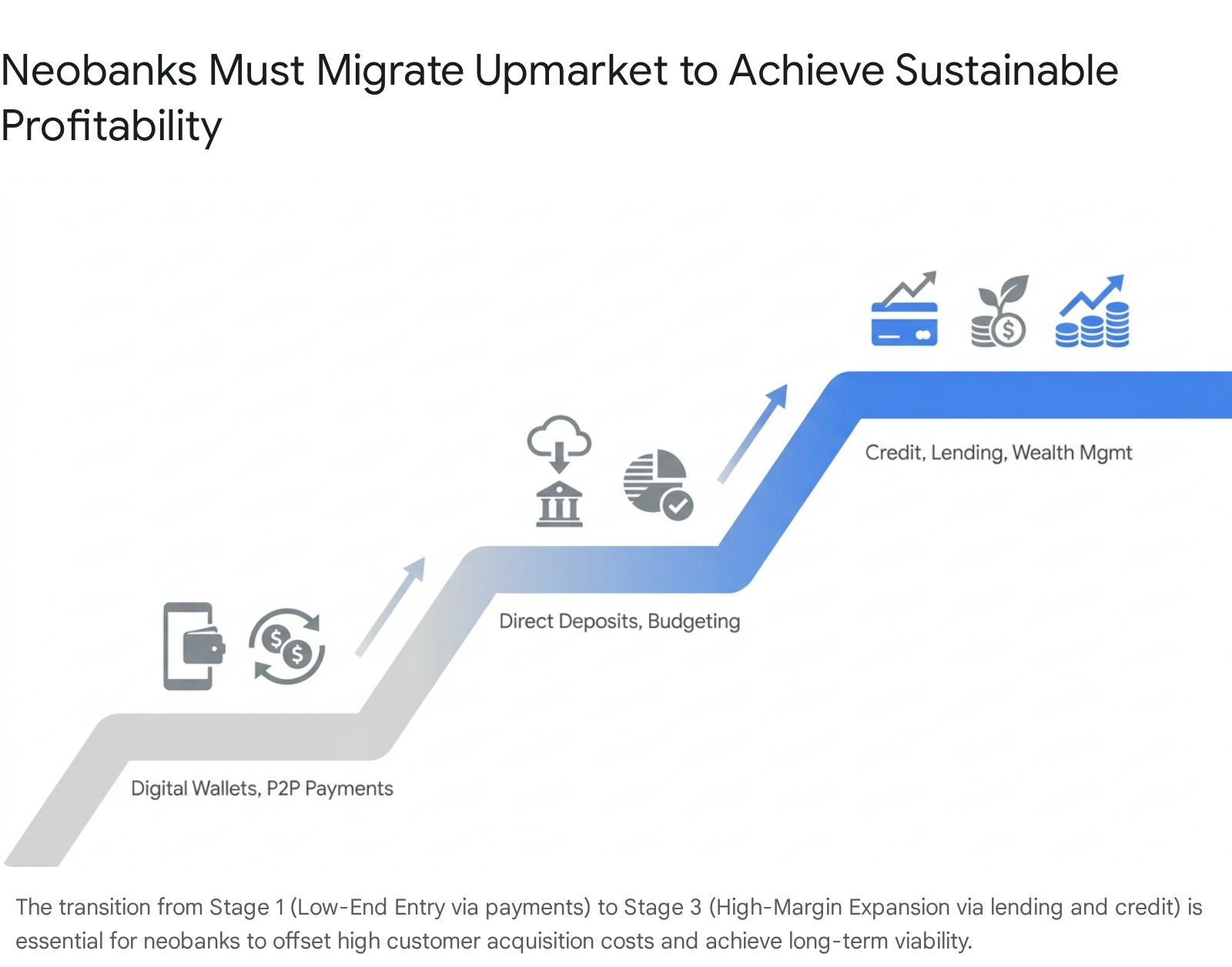

To achieve long-term viability, digital challengers that enter the market through low-end disruption must execute a strategic migration upmarket. This migration is necessary because the foundational products used to acquire customers - such as zero-fee debit cards or basic money transfers - generate insufficient revenue to sustain a standalone business.

The operational strategy of a typical neobank can be mapped across distinct phases of maturity, tracking the evolution from low-margin acquisition tools to high-margin financial products:

- Stage 1: Low-End Entry: The primary product offerings consist of digital wallets, P2P payments, and prepaid debit cards. Revenue is generated via interchange fees (swipe fees) and minor withdrawal fees. The strategic objective is rapid user acquisition, establishing brand trust, and driving daily app engagement among unbanked populations, students, subprime consumers, and early adopters.

- Stage 2: Core Banking: As the firm matures, it introduces direct deposit accounts, basic budgeting tools, and minor overdraft coverage. The revenue mechanism shifts to net interest income on aggregated deposits and premium subscription tiers. The primary goal is achieving primary account status, reducing churn, and stabilizing funding from lower-middle to middle-income earners and gig workers.

- Stage 3: High-Margin Expansion: In the final phase, the neobank offers unsecured personal loans, credit cards, Buy Now Pay Later (BNPL) facilities, and wealth management. The revenue model relies on interest spreads, origination fees, and assets under management (AUM) fees. The ultimate strategic objective is sustainable profitability and maximizing Customer Lifetime Value (LTV) among prime borrowers, small-to-medium businesses (SMBs), and the mass affluent.

The success of this trajectory depends heavily on network effects and economies of scale. In the initial stage, neobanks leverage slick user interfaces and high deposit yields to rapidly aggregate an unprofitable but vast user base. As they transition to Stage 2, they encourage users to deposit their payroll directly, turning transient transaction volume into a stable deposit base. Finally, in Stage 3, the neobank leverages the proprietary transactional data gathered during the earlier stages to underwrite credit risk more accurately than legacy banks 1213. This data advantage allows them to issue high-margin loans and credit products, completing the journey from a niche payment tool to a comprehensive financial institution capable of challenging incumbent profitability 1214.

Geographic Diversity and Technological Leapfrogging

The mechanics of financial disruption vary profoundly across geographic regions. While Western fintech evolution has largely been characterized by the unbundling of traditional banking services, emerging economies - particularly in Asia - demonstrate a phenomenon known as technological leapfrogging. In these markets, populations have entirely bypassed the intermediate stages of financial infrastructure, such as checkbooks, physical bank branches, and traditional credit card networks, transitioning directly from cash-based economies to mobile-first digital ecosystems 489.

State-Sponsored Public Infrastructure

In several major developing economies, disruption has been initiated and subsidized by the state rather than private venture capital. India's Unified Payments Interface (UPI), launched by the central bank-backed National Payments Corporation of India (NPCI) in 2016, represents the pinnacle of this model 17. UPI is a real-time, account-to-account (A2A) public interoperability layer that allows third-party applications to facilitate immediate transfers.

The scale of this state-sponsored disruption is unprecedented. In 2023, UPI processed 117.6 billion transactions exceeding Rs 182 lakh crore in value 10. This rapid growth trajectory carried into the first half of 2024, which alone recorded 78.97 billion transactions valued at Rs 116.63 trillion, effectively accounting for the vast majority of India's digital payment volume 11. By mandating a zero-merchant discount rate (MDR) for transactions below a certain threshold, the Indian government effectively eliminated the core revenue stream that traditional Western payment networks rely upon 1720. This infrastructure forced private fintechs like PhonePe and Paytm to innovate beyond payments, expanding rapidly into insurance, mutual funds, and merchant services to achieve profitability 128.

Similar state-guided leapfrogging is evident in Brazil with the Pix payment system, which rapidly captured a massive share of the nation's electronic payments by circumventing legacy card rails 20. In 2023, Pix processed over 42 billion transactions worth more than BR $17 trillion, representing a 72% year-over-year growth 2112. Operating as a direct challenger to traditional banking limits, Pix reached 149 million consumers and 15 million businesses by the end of 2023, firmly establishing real-time payments as the national default 21.

Super-App Ecosystems

In contrast to the interoperable public infrastructure of India, China and Southeast Asia have been disrupted by closed-loop, private "super-app" ecosystems. Super-apps are all-in-one mobile platforms that integrate messaging, e-commerce, ride-hailing, food delivery, and full-stack financial services within a single user interface 8.

In China, Ant Group's Alipay and Tencent's WeChat Pay dominate the digital landscape, collectively commanding over 90% of the mobile payment market 2013. These platforms leverage immense network effects and proprietary consumer behavioral data to underwrite credit and distribute wealth management products instantly 813. Similarly, in Southeast Asia, ride-hailing giants like Grab and GoTo (Gojek and Tokopedia) have utilized their frequent user interactions to launch dominant digital wallets (GrabPay and GoPay), expanding into micro-lending and insurance 814.

By 2024, Grab reached 41.3 million monthly active users and generated $2.8 billion in revenue 26. During the same period, GoTo's FinTech segment reached 20.2 million monthly transacting users, with its standalone app accelerating customer acquisition 15. Combined, these two platforms command an estimated 85% gross merchandise value (GMV) share of the regional ride-hailing and embedded delivery market 16. This dynamic creates a "Double Squeeze" on traditional Asian incumbents. The super-apps systematically unbundle the most profitable financial services (credit and investment) while leaving legacy banks burdened with the high fixed costs of maintaining physical infrastructure and regulatory compliance 4. Unlike European consumers, who slowly transitioned to web portals, hundreds of millions of Asian consumers formed their primary financial relationships with a super-app before ever stepping foot in a bank branch 4.

The Sponsor Bank Model and Regulatory Scrutiny

A pervasive misconception in the financial sector is that sleek consumer-facing digital applications operate as fully autonomous, chartered banks. In reality, the vast majority of digital front-ends lack a banking charter. Instead, they rely heavily on traditional, legacy "sponsor banks" through a framework known as Banking-as-a-Service (BaaS) 729.

BaaS decouples the regulatory banking license and core ledger infrastructure from the customer-facing user experience 717. Fintechs manage customer acquisition and frontend design, while regional and community sponsor banks provide the regulatory compliance, deposit holding, and access to payment rails (such as the Automated Clearing House, or ACH, and wire transfers) 731.

The 2023 - 2024 Regulatory Crackdown

While the BaaS model democratized entry into the financial sector, it introduced severe systemic vulnerabilities, leading to a massive regulatory crackdown. Federal agencies - specifically the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation (FDIC), and the Federal Reserve - escalated their oversight of BaaS partnerships throughout 2023 and 2024 2918.

The primary regulatory concern is third-party risk management. Regulators maintain that a chartered bank cannot outsource its compliance obligations to a technology startup. A recent analysis indicated that banks providing BaaS to fintechs accounted for a disproportionately large percentage of severe enforcement actions in 2023 19. The severity of this regulatory shift is evidenced by specific institutional penalties targeting systemic breakdowns in Bank Secrecy Act (BSA) compliance, Anti-Money Laundering (AML) controls, and consumer protection frameworks:

- Blue Ridge Bank: In January 2024, the OCC issued a Cease and Desist order against the institution citing systemic BSA/AML breakdowns and weak independent testing. The bank was forced to undergo a massive overhaul, only achieving the termination of the order 22 months later after hiring a completely new executive risk management team 2021.

- Piermont Bank: In February 2024, the FDIC subjected Piermont Bank to a strict consent order over unsafe banking practices and a lack of proper internal controls over its third-party partnerships, requiring the bank to retroactively review all transactions dating back to September 2022 to identify unreported suspicious activity 2223.

- Evolve Bank & Trust: Serving as a primary partner in the sector, Evolve received a formal enforcement action from the Federal Reserve in 2024 - independent of the catastrophic bankruptcy of its middleware partner Synapse - mandating immediate revisions to its fintech compliance protocols and risk management procedures 24.

The regulatory urgency was further compounded by the 2024 bankruptcy of Synapse, a prominent BaaS middleware provider, which left thousands of consumers unable to access their funds and highlighted the profound fragility of multi-layered fintech-bank dependencies 2918.

Regulatory Burden Comparison

The regulatory expectations placed upon financial entities differ drastically depending on their structural foundation. To understand why fintechs avoid charters, and why regulators are penalizing sponsor banks, it is necessary to compare their respective burdens.

| Entity Type | Structural Definition | Primary Regulatory Burden | Capital Requirements | Compliance Focus |

|---|---|---|---|---|

| Pure Digital Front-End (Fintech) | Unchartered technology platform acting as a user interface for financial products. | Indirect regulation via contractual obligations to their partner bank. Subject to state money transmitter laws. | Minimal. Venture capital funded. No federally mandated capital adequacy ratios. | User Experience (UX), data privacy, and maintaining basic KYC to satisfy the sponsor bank's audit requirements. |

| Fully Chartered Neobank | Digital-native institution that has obtained its own national or state banking charter. | Direct, comprehensive federal oversight (OCC, FDIC, Fed). Subject to frequent, rigorous safety and soundness examinations. | High. Must maintain Basel-aligned capital ratios and retain a massive liquidity buffer to protect consumer deposits. | End-to-end management of BSA/AML, fair lending laws, and strict third-party vendor management. |

| Legacy Incumbent (Sponsor Bank) | Traditional chartered bank providing core infrastructure to digital front-ends. | Direct federal oversight. Held strictly liable for the actions of their unchartered fintech partners under third-party risk guidelines. | High. Must hold capital against the aggregate risk of their own operations plus the risk introduced by fintech partners. | Aggressive oversight of fintech partners, transaction monitoring, and ensuring the fintech does not engage in deceptive marketing. |

(Note: The above matrix synthesizes the structural disparities outlined by regulatory enforcement actions and institutional frameworks 291825.)

The severity of recent consent orders has forced sponsor banks to significantly increase the compliance requirements they impose on fintech partners, slowing innovation cycles and pushing some banks to exit the BaaS market entirely 2925.

Macroeconomic Shifts and Profitability Mandates

The trajectory of fintech disruption has been abruptly altered by profound macroeconomic shifts. From the aftermath of the 2008 financial crisis until late 2021, the global economy was defined by a Zero Interest Rate Policy (ZIRP) 26. In 2022, facing historic inflation, central banks initiated an aggressive tightening cycle; the U.S. Federal Reserve raised rates rapidly, transitioning the economy into a sustained high-interest-rate environment through 2023 and 2024 4127. (Note: Precise real-time macroeconomic impacts remain dynamic; the following analysis relies strictly on validated institutional data up to late 2024).

The End of the "Growth at All Costs" Era

During the ZIRP era, capital was abundant and cheap. Venture capital firms aggressively funded fintech startups, demanding rapid user acquisition and top-line revenue growth while completely ignoring unit economics and net losses 4144. Fintechs could afford to subsidize unviable business models - offering unsustainably high yield on deposits or zero-fee stock trading - knowing that sequential funding rounds were easily accessible.

The transition to high interest rates exposed the fragility of these models. The cost of capital surged, venture funding contracted sharply, and the market consensus abruptly shifted from "growth at all costs" to a mandate for sustainable, near-term profitability 4528. A significant number of fintech business models that relied on cheap debt to fund subprime lending or "Buy Now, Pay Later" (BNPL) structures found themselves squeezed between skyrocketing funding costs and rising consumer delinquency rates 47.

Transitioning to Sustainable Unit Economics

Consequently, the industry is undergoing a severe rationalization. While high interest rates have theoretically boosted the net interest margins (NIM) of fully chartered institutions holding consumer deposits, unchartered fintechs that rely primarily on fixed interchange swipe fees do not capture the benefit of high rates 4447.

To survive the current macroeconomic reality, fintechs are pivoting their strategies. Consumer-focused startups are actively abandoning subprime markets to target prime borrowers who exhibit lower default risks, despite these segments being highly saturated 47. Furthermore, there is a pronounced industry pivot toward Business-to-Business (B2B) fintech models - such as corporate expense management and financial workflow software - which offer higher Average Contract Values (ACV), lower churn rates, and more stable revenue streams than volatile consumer segments 45.

Emerging Headwinds in Customer Acquisition and Compliance

As macroeconomic conditions tighten, digital challengers must also navigate severe operational headwinds that threaten their core business models, specifically the escalating costs of acquiring users and the crushing burden of financial crime compliance.

Rising Customer Acquisition Costs

The financial technology market has reached a state of intense channel saturation, driving Customer Acquisition Costs (CAC) to prohibitive levels. Historically, fintechs leveraged cheap digital advertising on social media to acquire users for a fraction of what traditional banks spent - specifically, traditional banks routinely expend $150 to $350 to acquire a new customer through physical branches and legacy marketing, whereas early neobanks originally drove CAC down to an incredibly efficient range of $5 to $15 4849. However, as the digital marketplace crowded with hundreds of competing neobanks, digital wallets, and lending apps, the cost of digital ad real estate surged 1350.

Recent data indicates that the average CAC for digital banking overall has escalated to approximately $189, with some estimates suggesting acquisition costs for specific B2B or specialized consumer segments have pushed past $1,400 per customer 495152. This spike in CAC fundamentally breaks the unit economics of many consumer fintechs. To maintain a sustainable business model, industry benchmarks dictate that a digital bank must preserve a Lifetime Value (LTV) to CAC ratio above 3:1 (with highly successful neobanks benchmarking at 3.5) 53. If the LTV of a retail customer - who may only use the app for occasional peer-to-peer transfers - does not exceed the cost to acquire them by a healthy margin, the business is structurally destined to fail 54.

Anti-Money Laundering and Consumer Protection Burdens

Simultaneously, the cost of maintaining regulatory compliance has transformed from a back-office administrative expense into an existential threat to fintech operating margins. Financial services is one of the most heavily regulated industries globally, and regulators are systematically closing the loopholes that allowed early fintechs to operate with light compliance 55.

The burden of Anti-Money Laundering (AML) and Know Your Customer (KYC) compliance is staggering. Traditional legacy banks invest heavily to manage this scale; for example, JPMorgan Chase dedicates $2 billion annually specifically to AI infrastructure (within a broader $19.8 billion technology budget), utilizing an OmniAI platform to monitor over $10 trillion in daily transactions, successfully cutting AML false positives by 95% 56. Similarly, Citi deploys sprawling Global Screening Operations units to manage KYC and sanctions compliance across a massive worldwide footprint of over 230,000 employees 5758.

Fintechs, attempting to operate lean technology teams, have historically struggled with the operational intensity of alert triage and manual identity verification 31. As state and federal regulators intensify their scrutiny of BaaS partnerships, sponsor banks are forcing their fintech partners to adopt institutional-grade AML systems 2529. This creates a paradox for digital challengers: they are expected to offer a seamless, frictionless, single-click onboarding experience to consumers while simultaneously executing rigorous, multi-layered identity verifications to satisfy their sponsor bank's compliance mandates 3145. The financial and human capital required to maintain sophisticated, AI-driven fraud detection networks and compliance teams fundamentally alters the cost structure of a fintech startup, erecting massive barriers to entry for new disruptors and forcing market consolidation 1345.

Practical Market Entry in the Post-ZIRP Era

Given the restrictive regulatory environment surrounding traditional Banking-as-a-Service partnerships and the prohibitive costs of obtaining a full banking charter, contemporary fintechs are adopting alternative market entry strategies to survive. Rather than launching standalone, direct-to-consumer (B2C) neobanks, many new entrants are aggressively pivoting toward Business-to-Business (B2B) embedded finance and enterprise software models 30.

In this "BaaS 2.0" paradigm, fintechs focus on integrating financial tools directly into existing non-financial platforms - such as vertical SaaS networks, healthcare portals, or gig-economy applications - leveraging the established distribution channels of partner brands to bypass exorbitant digital customer acquisition costs 6162. Furthermore, by acting strictly as technology vendors or non-custodial software providers, these startups purposefully distance themselves from the direct compliance liabilities of holding consumer funds. They rely instead on deeply integrated, co-managed risk frameworks with tier-one sponsor banks to satisfy regulatory scrutiny without bearing the full weight of a banking charter 61.

Ultimately, the era of frictionless, highly subsidized disruption in financial services has concluded. The modern fintech landscape is defined by the rigorous realities of high-interest-rate economics, the necessity of deep structural partnerships with incumbent banks, and the relentless pressure of regulatory compliance, signaling a maturation of the sector from radical disruption to institutional integration.