Evidence-Based Steps to Improve Your Credit Score

The architecture of the United States consumer credit system is undergoing its most profound transformation in decades. Driven by regulatory interventions, macroeconomic shifts, and the modernization of algorithmic risk assessment by the Federal Housing Finance Agency (FHFA), the paradigms governing creditworthiness are rapidly evolving. For the American consumer, a credit score is not merely a metric of financial health; it is the ultimate determinant of capital access, housing opportunities, and lifetime borrowing costs. This report is explicitly framed around the U.S. credit ecosystem - specifically the algorithmic models of FICO and VantageScore - providing a comprehensive analysis of modern credit optimization, recent structural developments, and evidence-based recovery strategies.

The Macroeconomic Context and the Real-World Cost of Credit

To contextualize the gravity of credit optimization, one must quantify its impact on everyday financial transactions. In the U.S. mortgage market, lenders utilize credit score tiers to price risk, typically operating in 20-point increments 1. As of early 2026, the national average FICO score has settled at 714, reflecting a slight decline driven by the resumption of student loan repayments and rising mortgage delinquencies 23. Macroeconomic analysts describe this as a "K-shaped" recovery in credit, where top-tier borrowers continue to consolidate wealth and expand their credit access, while lower-income brackets face thinning margins and increased subprime stress 2.

The financial penalty of operating in the lower tiers of this K-shaped economy is severe. Consider a consumer seeking a standard $300,000, 30-year fixed-rate mortgage. A borrower presenting a 620 FICO score - often the threshold for conventional loan approval - faces an average Annual Percentage Rate (APR) of 7.341% 1. This results in a monthly payment of $2,065 and a staggering $443,429 in total interest paid over the life of the loan 1. Conversely, a borrower who strategically improves their profile by 140 points to reach the elite 760+ tier unlocks an APR of 6.566% 1. This optimized score reduces the monthly payment to $1,909 and the total interest to $387,326 1. In this everyday scenario, an optimized credit profile translates to $156 in monthly cash flow savings and precisely $56,103 in exact dollar savings over the mortgage's duration 1. A mere 50-point drop, taking a consumer from "good" to "fair" credit, can strip away tens of thousands of dollars in purchasing power 3.

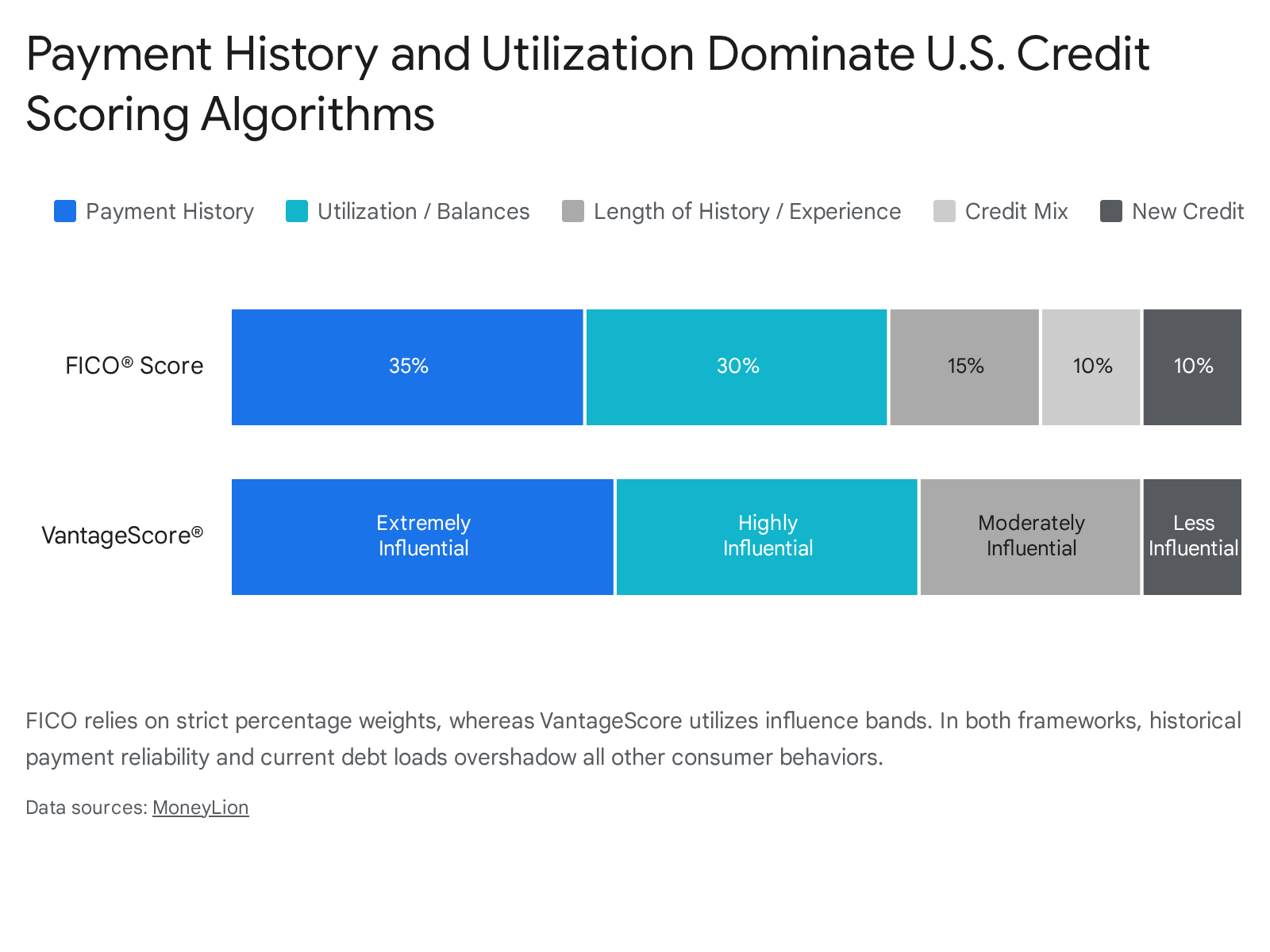

The Anatomy of a U.S. Credit Score: FICO vs. VantageScore

The U.S. credit reporting landscape is dominated by two primary algorithmic frameworks: FICO (Fair Isaac Corporation) and VantageScore, a joint venture created by the three major credit bureaus (Equifax, Experian, and TransUnion) 34. While both models ingest the identical underlying consumer data furnished to the bureaus and scale from 300 to 850, they weight specific behaviors differently and serve varying underwriting purposes. FICO scores currently power over 90% of major lending decisions - enjoying an near-monopoly in traditional mortgage underwriting - while VantageScore is heavily utilized by free consumer credit monitoring platforms and a growing coalition of credit card issuers 46.

The following table delineates the exact structural methodologies employed by both models. FICO relies on rigid percentage allocations, whereas VantageScore evaluates consumer data through descriptive influence levels, though the foundational hierarchy of risk assessment remains largely parallel 4.

| Scoring Factor | FICO Percentage Weight | VantageScore Influence Level | Strategic Implication |

|---|---|---|---|

| Payment History | 35% | Extremely Influential | The paramount factor governing creditworthiness. A single 30-day late payment inflicts catastrophic damage across both models 47. |

| Credit Utilization / Amounts Owed | 30% | Highly Influential | The ratio of revolving balances to total credit limits. Algorithmic optimization requires keeping this metric aggressively low 45. |

| Length of Credit History | 15% | Moderately Influential | Rewards mature credit files. Calculated by the age of the oldest account and the average age of all accounts 45. |

| Credit Mix | 10% | Moderately Influential | A diversified portfolio of revolving debt (credit cards) and installment debt (auto loans, mortgages) demonstrates comprehensive risk management 49. |

| New Credit / Inquiries | 10% | Less Influential | Opening multiple accounts rapidly signals financial distress. Hard inquiries depress scores temporarily 49. |

The Transition to Trended Data: FICO 10T and VantageScore 4.0

For decades, consumer credit scoring operated on a "snapshot" methodology. Legacy models evaluated a consumer's financial standing based solely on the exact balances reported on the specific day the credit file was pulled 1011. This allowed savvy consumers to aggressively manipulate their utilization ratios immediately prior to applying for a loan, creating an artificially pristine profile that masked long-term debt behaviors.

In response, the industry is undergoing a seismic shift toward "trended data" models, most notably FICO 10T and VantageScore 4.0. Rather than assessing a single point in time, these advanced algorithms construct a 24-month historical trajectory of a consumer's financial habits 121314. This continuous view allows lenders to explicitly differentiate between "transactors" - consumers who utilize credit for convenience and pay their balances in full each month - and "revolvers," who carry persistent debt burdens and accrue interest 11. If a consumer slowly accumulates revolving debt over 18 months, even without missing a single payment, trended data models will identify this compounding risk and adjust the score downward 13.

This algorithmic evolution is actively reshaping the U.S. mortgage market. The Federal Housing Finance Agency (FHFA) has mandated that Fannie Mae and Freddie Mac transition from the classic tri-merge FICO system to a framework utilizing both FICO 10T and VantageScore 4.0 146. FICO's proprietary white papers claim that FICO 10T materially outperforms VantageScore 4.0, alleging it identifies 18% more defaulters in the critical lower-score deciles compared to a mere 3.4% improvement by VantageScore, though VantageScore fiercely contests these metrics, accusing FICO of relying on truncated, unrepresentative data 78910. Regardless of the corporate friction, the implementation timeline stretches through 2026 and 2027, meaning borrowers preparing for future real estate transactions must adopt long-term transactor behaviors today, as short-term fixes will no longer deceive the underwriting algorithms 146.

FAQ: Does Carrying a Balance Actually Help? (And Other Common Misconceptions)

The realm of consumer finance is clouded by pervasive, deeply entrenched myths that actively sabotage credit optimization efforts. Dispelling these misconceptions is the foundation of any effective credit recovery strategy.

Debunking the Balance-Carrying Myth

Perhaps the most damaging fallacy in personal finance is the belief that carrying a small revolving balance past the due date - and thereby paying interest to the issuer - somehow improves a credit score. This is categorically false. Carrying a balance does absolutely nothing to elevate a credit profile; it solely enriches the lending institution 112021.

This misconception represents a severe misunderstanding of a legitimate optimization technique known among credit experts as the AZEO (All Zero Except One) method 20. Scoring algorithms require empirical proof of active, responsible credit management. If every credit card on a consumer's file reports a strict $0 balance, the algorithm registers a lack of recent credit usage, which can temporarily depress or stall score growth 20. The FICO algorithm rewards a utilization "sweet spot" of between 1% and 9% 1120.

However, the critical distinction lies in the timeline of reporting. Banks report balances to the credit bureaus on the statement closing date, which is typically several weeks before the actual payment due date 1011. The AZEO strategy dictates that a consumer pays all credit cards down to exactly zero prior to their respective statement closing dates, leaving only a single card to report a nominal balance (e.g., $10) to the bureaus 2021. Once that tiny balance is reported, the consumer still pays that final card in full by the due date, entirely avoiding interest charges 1022. AZEO demonstrates active, meticulous financial control without ever carrying debt month-to-month, but it is an intensive tactic best reserved for the 30 to 45 days immediately preceding a major mortgage or auto loan application 2122.

Debunking the Inquiry Myth: Does Checking Your Own Credit Lower It?

A highly common deterrent to proactive credit monitoring is the fear that checking one's own report will lower the score. This anxiety stems from a misunderstanding of inquiry classifications. Accessing your own credit profile through platforms like AnnualCreditReport.com constitutes a "soft inquiry," which is entirely invisible to scoring algorithms and has zero impact on the mathematical calculation of a score 11.

In contrast, a "hard inquiry" occurs when a consumer actively applies for new credit, authorizing a lender to review their file for underwriting purposes 34. Each hard inquiry signals a pursuit of fresh capital and typically penalizes the score by 5 to 10 points for up to 12 months, remaining visible on the report for two years 324. Fortunately, modern algorithms contain deduplication logic; if a consumer applies for multiple mortgages or auto loans within a focused 14- to 45-day window, the system groups them as a single rate-shopping event, applying only one penalty 25. Consumers should routinely monitor their own files for inaccuracies without any fear of algorithmic reprisal.

Debunking the Account Closure Myth: Does Closing Unused Cards Improve Your Profile?

Consumers seeking to simplify their financial lives often erroneously close old, unused credit card accounts, assuming it demonstrates fiscal responsibility. In reality, closing an established account is a universally damaging action that simultaneously triggers two negative algorithmic responses 3524.

First, closing an account immediately eradicates that specific credit limit from the consumer's total available credit pool. If the consumer maintains revolving balances on other active cards, the sudden contraction of the overall limit mathematically inflates their aggregate credit utilization ratio, causing an immediate, sharp drop in the score 35. Second, the closure truncates the active lifespan of the credit file. The "Length of Credit History" accounts for 15% of a FICO score 45. To maintain optimal credit age and maximum available capacity, consumers are universally advised to keep old, no-annual-fee credit cards open, utilizing them for nominal, auto-paid subscriptions to prevent the issuer from closing them due to inactivity 525.

Recent Developments (2023+): Medical Debt and BNPL Integration

The U.S. credit reporting apparatus has experienced intense regulatory and structural turbulence in recent years, fundamentally altering how distinct categories of debt are processed by scoring algorithms.

The Medical Debt Legal Battle: From Total Bans to Court Vacations

For decades, medical debt functioned as an involuntary burden that severely damaged credit scores, despite vast empirical evidence suggesting it is a uniquely poor predictor of a consumer's likelihood to default on conventional loans 2627. Recognizing this disparity, the three major credit bureaus initiated a sweeping, voluntary policy shift in 2023. They unilaterally ceased reporting all paid medical collections, eradicated unpaid medical debts under $500 from consumer files, and implemented a 365-day grace period preventing new medical debts from appearing on reports while patients navigated insurance disputes 262930. This voluntary action successfully purged an estimated 70% of medical tradelines from the American credit ecosystem 30.

Attempting to formalize and expand these protections, the Consumer Financial Protection Bureau (CFPB) finalized a landmark federal rule in January 2025. This regulation sought to outright ban the inclusion of all medical debt on consumer credit reports, regardless of the dollar amount or payment status, and prohibited lenders from utilizing medical debt data in underwriting decisions 6272930. The CFPB projected this rule would lift the credit scores of 15 million Americans by an average of 20 points, effectively dissolving $49 billion in reported medical debt 2712.

However, this victory for consumer advocates was abruptly dismantled. In July 2025, a federal judge in the U.S. District Court for the Eastern District of Texas vacated the CFPB's rule entirely 291333. The court found that the CFPB had vastly exceeded its statutory authority under the Fair Credit Reporting Act (FCRA), ruling that the agency could not unilaterally prohibit the reporting of specific debt categories based on their origin 272933. The decision was celebrated by the Consumer Data Industry Association (CDIA) and collection agencies, who argued that suppressing accurate debt data threatens the integrity of the risk assessment system 3334.

The reality for the American consumer in 2026 is highly fragmented. Because the federal CFPB rule is legally dead, unpaid medical collections exceeding $500 continue to actively damage credit profiles across the nation 272930. The primary shields remaining for consumers are the bureaus' 2023 voluntary threshold rules (which survived the court ruling) and the growing patchwork of state-level legislation, as over 15 states have now independently banned medical debt reporting within their jurisdictions 293033. Furthermore, the evolution of scoring models provides uneven relief; while VantageScore 4.0 entirely disregards medical collections, and FICO 10T weights them less severely, the reality is that the mortgage industry's continued reliance on legacy models (FICO 2, 4, and 5) means medical debt remains a lethal obstacle to homeownership 6262735.

The Integration of Buy Now, Pay Later (BNPL) Services

Parallel to the medical debt controversy, the explosive proliferation of Buy Now, Pay Later (BNPL) financing created a massive blind spot in the consumer credit market. By late 2023, roughly 53.6 million U.S. adults were utilizing BNPL plans, generating billions in "phantom debt" that remained entirely invisible to traditional lenders and scoring algorithms 14. Regulators grew concerned that borrowers were stacking multiple hidden loans, dangerously overextending their true debt-to-income ratios 14.

To rectify this, FICO engineered and deployed FICO Score 10 BNPL and FICO Score 10T BNPL 1415. These models actively ingest and analyze BNPL repayment data furnished by major providers like Affirm 1416. The algorithmic impact on the end consumer is highly dependent on behavioral patterns. Initial joint studies indicate that the integration is relatively benign for the majority; 85% of BNPL users experience a score shift of fewer than 10 points 141718.

However, BNPL reporting introduces severe, competing forces into the algorithm. While consistent, on-time installment payments inject positive data into the consumer's "payment history" and enhance their "credit mix" (which together account for 45% of a traditional FICO score), the mechanics of BNPL actively penalize frequent users 417. Because each BNPL transaction technically opens a discrete, short-term installment loan, a consumer utilizing BNPL for everyday purchases will flood their credit report with new accounts. This drastically reduces the "average age of accounts" and spikes the velocity of "new credit" metrics, subsequently dragging the score downward 17. Consequently, while responsible BNPL use can assist thin-file consumers in establishing a footprint, chronic "loan stacking" presents a new, highly visible risk factor under modern algorithmic scrutiny 161742.

FAQ-Worthy Sub-Questions: Navigating Modern Credit Hurdles

Are Services Like Experian Boost Worth It?

In the pursuit of rapid score inflation, millions of consumers have turned to self-reporting mechanisms like Experian Boost, which allows individuals to link their bank accounts and funnel utility, telecom, and streaming service payment data directly into their credit files 101944. While the marketing promises instant improvement, the architectural utility of these services in 2026 is highly conditional.

Empirical testing reveals that Experian Boost yields a modest average increase of roughly 8 points 44. The service is most efficacious for "thin file" consumers - those with fewer than five established credit accounts - who can realize gains of up to 17 points 44. Conversely, borrowers with mature, thick credit files often see negligible movement, with many experiencing zero point changes 44.

The critical, often misunderstood limitation of Experian Boost is its rigid platform exclusivity and model constraints. The injected data only manipulates the Experian FICO 8 score 44. It has absolutely zero effect on Equifax or TransUnion files 44. More importantly, because the mortgage lending industry currently relies heavily on legacy models (FICO 2, 4, and 5) that do not possess the programming logic to process self-reported utility data, Experian Boost is practically useless for consumers attempting to secure a home loan 44. It remains a viable, albeit limited, tool for young adults seeking entry-level unsecured credit cards, but it provides no leverage in high-tier underwriting.

Do Authorized Users Build Credit?

"Piggybacking" as an authorized user involves a primary account holder adding a secondary individual to a mature, pristine credit card. The primary account's entire chronological payment history and credit limit are subsequently mirrored onto the authorized user's credit report 2021. This strategy remains one of the most potent, entirely legal mechanisms for rapidly fabricating creditworthiness from scratch.

A comprehensive longitudinal study conducted by researchers at Rice University and the University of Wisconsin-Madison scrutinized 16 years of credit data to analyze this phenomenon, coining the term "nepo credit" 22. The academic findings confirm that young adults leveraging family members' accounts receive a massive, instantaneous credit score boost ranging from 22 to 42 points 22. This artificial elevation allows authorized users to cross prime borrowing thresholds, making them 2.7 percentage points more likely to secure an auto loan and 2.9 percentage points more likely to be approved for a mortgage compared to their peers lacking familial credit support 22.

However, the study uncovered a striking paradox regarding true risk profiles. Borrowers operating on inflated "nepo credit" were statistically 0.5 to 0.8 percentage points more likely to eventually fall seriously delinquent (90+ days late) on their own subsequent debt obligations 22. The imported history artificially inflates the credit score relative to the borrower's true, untested credit quality 22. Despite this increased empirical risk of default, the algorithms continue to blindly reward the data injection, making authorized user status an incredibly efficient shortcut to capital access.

How Fast Can I Raise My Credit Score?

The velocity of credit repair is governed by the structural cadence of institutional reporting cycles and the strict statutory deadlines dictated by the Fair Credit Reporting Act (FCRA). Credit scores do not update in real-time; they are recalculated instantly only when new data is furnished to the bureaus 31023.

When a consumer executes a strategic action - such as paying down a maxed-out credit card to optimize utilization - the timeline is contingent upon the creditor. Banks typically dispatch data to Equifax, Experian, and TransUnion once a month, shortly after the statement closing date 10. Consequently, organic score improvements driven by debt reduction generally materialize within 30 to 45 days, or 1 to 2 billing cycles 51949.

Conversely, when a consumer attacks inaccurate derogatory marks through formal disputes, federal law dictates the timeline. Upon receiving a dispute, the FCRA mandates that credit bureaus conduct a "reasonable reinvestigation" within exactly 30 days 1124. If the consumer submits supplemental evidence during this window, the investigation period is legally extended by 15 days, capping the process at 45 days 1124. During this high-volume process, offshore dispute agents often allocate a mere 5 to 10 minutes to review the evidence 51. If the data furnisher fails to verify the debt or respond within the mandated window, the bureau is legally compelled to delete the negative tradeline 25. This deletion frequently triggers an instantaneous score surge the moment the investigation concludes 4951. For consumers actively engaged in mortgage underwriting who cannot wait 45 days, loan officers possess the capability to order a "rapid rescore" - a premium service that forces the bureaus to manually update the file and generate a new score within 3 to 7 days 49.

The Anatomy of Negative Marks: Point Drops and Recovery Timelines

Understanding the mathematical severity of derogatory marks is critical for diagnosing credit collapses and executing triage. A fundamental, counterintuitive characteristic of the FICO algorithm is that borrowers possessing exceptionally high scores suffer the most catastrophic point drops when a negative event occurs, as the algorithm calculates they have more pristine history to lose compared to a subprime borrower 24.

The following table estimates the algorithmic impact of common derogatory marks and outlines the timeline for recovery, which is heavily governed by the reporting limitations established by the FCRA.

| Negative Event | Estimated FICO Point Drop | FCRA Reporting Limit / Recovery Timeline | Strategic Context |

|---|---|---|---|

| 30-Day Late Payment | 17 - 37 pts (Fair Credit) 63 - 83 pts (Excellent Credit) |

Remains visible for 7 years. Score impact lessens after 12 - 24 months 24. | Late payments dominate 35% of the score. Setting up automated minimum payments is an essential safeguard 3724. |

| Collection Account | 50 - 100+ pts | 7 years + 180 days from the original Date of First Delinquency (DOFD) 5354. | Modern scoring models ignore paid collections; however, legacy mortgage models do not. Paying can yield a 20 - 60 point boost under FICO 9/10 354955. |

| Tax Liens / Civil Judgments | Indirect Impact Only | No longer reported on consumer credit files as of 2018 5657. | While purged from credit reports, they remain public records accessible to lenders via alternative databases (e.g., LexisNexis), frequently triggering loan denials 56575859. |

| Short Sale | 85 - 160 pts | 7 years 6061. | While the initial point drop mirrors a foreclosure, a short sale avoids the stigma of a completed legal repossession, allowing for a much faster mortgage recovery trajectory 6126. |

| Foreclosure | 85 - 160 pts | 7 years from the date of the first missed payment leading to foreclosure 60. | Foreclosures are invariably bundled with a cascading sequence of 90-to-180-day late payments prior to the event, creating compounding score damage 6061. |

| Bankruptcy (Chapter 7 & 13) | 130 - 200 pts | 10 years for Chapter 7. 7 years for Chapter 13 95560. |

Recovery requires immediate, aggressive rebuilding with secured cards. Fair to good scores (640 - 700+) are mathematically achievable within 2 to 5 years post-discharge 95527. |

The Illegal Tactic of "Re-Aging" Debt

When navigating recovery from severe delinquency, consumers must remain vigilant against the aggressive tactics of third-party debt buyers. A foundational component of the FCRA is the Date of First Delinquency (DOFD) - the exact, immutable date a consumer missed the payment that precipitated an account charge-off 535464. Federal law dictates that collection accounts must vanish from a credit report exactly 7 years and 180 days after this initial DOFD 5354.

To circumvent this limitation, unscrupulous collection agencies frequently engage in "re-aging," a starkly illegal practice where the agency reports a falsified, newer date to the bureaus (often the date the agency purchased the debt portfolio) 536566. This malicious action resets the 7-year statutory clock, essentially creating "zombie debt" that haunts the consumer's credit profile indefinitely 5465. The Federal Trade Commission (FTC) and the CFPB strictly prohibit this behavior 5465. Consumers who identify a re-aged account must aggressively challenge it by mailing certified disputes citing 15 U.S.C. § 1681c, forcing the furnishers to supply the true DOFD within 90 days or face regulatory enforcement 54.

Practical Takeaways and Timelines: Quick Wins vs. Long-Term Habits

The mechanics of credit optimization require bifurcating strategies into tactical, immediate interventions and sustained behavioral shifts.

Quick Wins (0 to 60 Days)

The most rapid method to manufacture a higher credit score is the aggressive manipulation of revolving utilization via the AZEO method 2022. Consumers preparing for imminent loan applications must pay all credit card balances to exactly zero before their individual statement closing dates, allowing only one card to report a micro-balance of 1% to 9% of its limit 20. Because utilization possesses no algorithmic memory in legacy FICO models, this action forces the system to calculate risk based on pristine debt levels, reflecting massive score improvements within 30 to 45 days as the new data cycles into the bureaus 1021.

Simultaneously, consumers must execute aggressive auditing of their reporting data. By procuring comprehensive files from AnnualCreditReport.com, borrowers can identify false late payments, re-aged collection DOFDs, and fraudulent inquiries 5154. Formal, certified mail disputes invoke the 30-day FCRA reinvestigation window 1124. Because data furnishers often fail to provide adequate verification within the strict statutory deadlines, bureaus are forced to delete the derogatory marks, resulting in immediate, highly lucrative score surges the moment the investigation concludes 25. Lastly, for individuals with thin or barren credit files, establishing an authorized user relationship on a financially secure relative's mature account acts as an algorithmic steroid, importing years of pristine payment history within a single 30-day billing cycle 2028.

Long-Term Habits (6 Months to Years)

While tactical manipulation is effective in the short term, the macroeconomic pivot toward trended data algorithms demands a fundamental restructuring of consumer behavior. The deployment of FICO 10T and VantageScore 4.0 throughout the mortgage industry necessitates that consumers cultivate enduring "transactor" habits 11121314. Because lenders will soon assess a continuous 24-month trajectory of debt management, consumers must consistently pay balances in full every month to avoid the severe penalties levied against compounding "revolvers" 1113.

Furthermore, consumers must fiercely protect the chronological integrity of their credit portfolios. The temptation to close older, unused credit cards must be resisted, as doing so permanently erases available credit capacity and truncates the average age of accounts 3524. By placing nominal, automated subscriptions on these legacy cards, consumers ensure continuous activity, cementing the 15% of the FICO score dependent on historical depth 525. Finally, when actively seeking financing, borrowers must strictly consolidate their rate-shopping activities 25. By clustering all mortgage or auto loan applications within a focused 14- to 45-day window, consumers trigger the algorithms' deduplication logic, consolidating multiple hard inquiries into a single, manageable penalty, thereby insulating the wider credit profile from systemic damage 25.

Bottom Line

The U.S. credit scoring system is a mathematically rigid, highly reactive framework where proactive optimization directly dictates consumer purchasing power and capital access. The transition toward trended data algorithms like FICO 10T, the fraught legal landscape surrounding the reporting of medical collections, and the integration of Buy Now, Pay Later financing have collectively dissolved the effectiveness of short-term algorithmic manipulation. Moving forward, sustained credit excellence requires a dual approach: consumers must meticulously enforce the accuracy of their reporting data through aggressive FCRA disputes, while simultaneously maintaining deep, seasoned accounts and executing flawless, monthly transactor behaviors to satisfy the evolving demands of modern underwriting algorithms.