Effects of Emotion, Sleep, and Stress on Trading Performance

The execution of financial trading requires decision-making under conditions of extreme uncertainty, rapid information processing, and constant risk assessment. Traditional economic models and the Efficient Market Hypothesis posit that market participants act as perfectly rational utility maximizers, pricing assets based purely on available fundamental information. However, empirical data from behavioral finance, neuroendocrinology, and cognitive psychology reveals a profound disconnect between theoretical models and actual market behavior. Financial performance, commonly quantified as Profit and Loss (P&L), is inextricably linked to the physiological and psychological states of the trader. Biological variables - ranging from endocrine system fluctuations and circadian rhythm disruptions to acute cognitive fatigue and cultural background - fundamentally alter risk preferences, pattern recognition, and trade execution.

Endocrine Responses and Financial Risk Tolerance

The human endocrine system serves as a biological substrate for financial risk-taking. Specifically, the interplay between steroid hormones modulates an individual's appetite for risk, influencing both individual P&L and broader market stability. These physiological mechanisms act as a risk-detection and confidence-calibration system adapted for physical competitive environments, but they frequently misalign with the abstract risks of modern financial markets 1.

Testosterone and the Amplification of Risk Appetite

Testosterone functions as a biological driver of competitive dominance, risk-taking, and confidence. Observational field studies conducted on professional trading floors in the City of London discovered a predictive relationship between a trader's morning testosterone levels and their afternoon profitability 21. On days when a trader's 11:00 a.m. testosterone registered above their personal median, their afternoon P&L was significantly higher - in some experienced cohorts, nearly a full standard deviation above the mean 12.

This correlation is underpinned by the "winner effect," a neurobiological feedback loop well-documented in animal behavior. In this loop, competitive success elevates testosterone, which subsequently increases dopamine transmission, confidence, and risk tolerance, thereby theoretically increasing the probability of continued success 123. In experimental asset market simulations, the administration of transdermal testosterone (three doses of 10 g 1% testosterone gel over 48 hours) shifted participant investments heavily toward riskier assets 4. The data indicates that testosterone operates primarily by inducing heightened optimism regarding future price changes 4.

However, when left unchecked, chronically elevated testosterone weakens cognitive and emotional control. This leads to impulsive decision-making, excessive trading volume, and the overvaluation of assets, creating a self-reinforcing cycle that actively contributes to the formation of market bubbles 35.

Cortisol and the Physiology of Market Volatility

While testosterone acts as an accelerator for financial risk, cortisol - a primary glucocorticoid released in response to physical or psychological stress - acts as a biological brake. Crucially, neuroeconomic research indicates that cortisol levels in professional traders do not correlate directly with the absolute rate of financial loss. Instead, cortisol tracks the variance, or standard deviation, of a trader's P&L and the implied volatility of the broader market 21. In studies analyzing derivative markets, daily group average cortisol levels correlated strongly with the implied volatility of German Bunds (r2 = 0.86), demonstrating that the hormone functions as a forward-looking risk-detection mechanism responding to uncertainty rather than realized negative outcomes 12.

In highly volatile environments, the hypothalamus-pituitary-adrenal (HPA) axis is continuously stimulated. During periods of extreme market uncertainty, traders experience unusually volatile cortisol levels, with some subjects exhibiting intraday spikes as high as 500% from morning to afternoon 1. Clinical administration of hydrocortisone - simulating the 69% physiological spike observed in live traders during volatile periods - demonstrates that sustained, high levels of cortisol drastically suppress risk appetite 86. In these experimental conditions, the "risk premium" (the amount of extra risk an individual is willing to tolerate for a higher potential return) plunged by 44% 8.

This physiological shift creates a systemic vulnerability. During market crashes, when the financial system most requires liquidity and the buying of distressed assets, the endogenous stress response of market makers and traders physically inhibits their capacity to assume risk 26. This cortisol-mediated risk aversion has the potential to transform localized market shocks into widespread liquidity crises.

Biological Feedback Loops in Financial Decision-Making

Data indicates that the human endocrine system initiates two opposing feedback loops during market participation. The interaction between market stimuli and hormonal secretion directly shapes macroeconomic phenomena.

| Biological Pathway | Market Stimulus | Primary Hormone | Neurobehavioral Shift | Macro-Market Impact |

|---|---|---|---|---|

| Dominance / Reward Loop | Competitive success, realized gains | Testosterone | Increased optimism, elevated risk appetite, weakened cognitive control | Overvaluation of assets, excess trading volume, formation of market bubbles 34 |

| Stress / Variance Loop | High market volatility, P&L variance | Cortisol | Heightened stress, acute risk aversion, suppressed risk premium | Failure to provide liquidity, irrational pessimism, exacerbation of market crashes 286 |

Sleep Deprivation and Cognitive Processing

Financial market participation is increasingly a 24-hour endeavor, fostering a culture where sleep is frequently sacrificed for extended market monitoring. However, physiological alertness is a fundamental prerequisite for rational capital allocation. Sleep deprivation causes measurable neurocognitive deficits that directly impair the specific analytical frameworks required for trading, carrying severe implications for workplace productivity and financial outcomes 1078.

Neuroanatomical Impairments from Sleep Loss

Sleep loss compromises the neural function of the prefrontal cortex, the brain region responsible for executive function, impulse control, and logical decision-making 10. Reduced activation in the prefrontal cortex directly correlates with irrational financial behaviors, including the disposition effect - the tendency for investors to prematurely close winning positions to secure a gain while holding onto losing positions to avoid realizing a loss 10. Furthermore, sleep loss physically degrades neural architecture; research indicates that chronic sleep deprivation can lead to astrocytes consuming portions of synapses 10.

In addition to prefrontal cortex degradation, sleep deprivation alters dopaminergic transmission in the striatum and thalamus, creating an artificial optimism bias as a byproduct of the brain's attempt to maintain wakefulness 1013. Consequently, sleep-deprived individuals exhibit an asymmetric risk preference: they become acutely focused on maximizing the size of potential gains while simultaneously distorting the probability and magnitude of potential losses 109.

Compounding these structural errors is the suppression of the anterior insula following sleep loss. The anterior insula is critical for processing the emotional experiences of loss and regret. When a well-rested trader executes a poor trade, the resulting negative emotional feedback facilitates learning and future risk mitigation. In sleep-deprived traders, decreased insula activation dulls the disappointment of financial loss, severely degrading the trader's ability to learn from disadvantageous decisions and correct destructive behaviors. Behavioral economists note that sleep-deprived traders making choices in the Iowa Gambling Task demonstrate patterns resembling those of patients with medial frontal brain damage 1013.

Quantitative Effects on Portfolio Profitability

The economic penalty of sleep deprivation can be quantified at the household and institutional levels. Large-scale analyses of household-level stock trading panel data have isolated the effects of sleep disruption using exogenous instrumental variables, such as local sunset time. Because human circadian rhythms entrain to the sun, populations residing on the late-sunset side of a time zone border experience an average reduction in sleep duration of approximately 19 minutes per day compared to those on the early-sunset side 10.

Panel regression analyses demonstrate that when sunset occurs one hour later - disrupting the sleep window - traders experience a 2.1 basis point decline in average daily abnormal returns over the subsequent 21 trading days 910. This performance drag is equivalent to a 0.44 percentage point reduction in monthly abnormal return, a deficit roughly comparable in magnitude to the underperformance penalty associated with extreme behavioral overconfidence (0.31 percentage points) 10. Merely living in a geography that promotes mild sleep deprivation reduces the likelihood of trading optimally in response to corporate earnings announcements, highlighting a severe deficit in attention and information processing 910.

Circadian Mismatch in Global Markets

Circadian mismatch extends to global institutional markets. When traders operate across disparate geographic time zones, market heterogeneity increases. Experimental asset market sessions reveal that markets populated by a high percentage of circadian-mismatched (and therefore cognitively fatigued) participants exhibit longer-lasting asset bubbles and higher overall share turnover volume 11.

Sleep quality directly dictates the optimal behavior of distinct investor profiles. Data covering 405 individual investors utilizing logistic regression and principal component analysis indicates that increased sleep duration causes passive investors to properly hold fewer stocks during bull markets and increase holdings during market declines 1213. Conversely, active investors with high sleep quality demonstrate improved timing, holding greater numbers of stocks during bull markets and decreasing exposure during bear markets. Proper sleep architecture, including midday naps, correlates strongly with improved total investment returns 1213.

Cognitive Overload in High-Frequency Environments

High-Frequency Trading (HFT) and modern algorithmic monitoring subject human supervisors to an intense, unnatural velocity of data. While the execution of trades occurs in milliseconds, the human mandate to monitor, intervene, and manage risk parameters induces profound psychological friction and cognitive fatigue 1914.

The Mechanics of Decision Fatigue

The human brain possesses a finite capacity for intrinsic, extraneous, and germane cognitive load. In complex data environments overflowing with conflicting financial signals, traders experience rapid depletion of cognitive reserves. Sustained vigilance tasks in visual trading environments lead to measurable decrements in alertness and accuracy within 20 to 30 minutes 21. As the load exceeds capacity, the brain shifts away from in-depth analytical processing and defaults to automated thinking and heuristic intuition 19. Traders frequently experience "choice paralysis," opting to take no action rather than risk an incorrect intervention in a highly volatile market 21.

When cognitive fatigue sets in, the autonomic nervous system physically reacts. Electrocardiogram (ECG) and biometric tracking reveal a decline in high-frequency (HF) heart rate variability (HRV) power during episodes of mental exhaustion, signaling a dampening of the parasympathetic nervous system 15. Simultaneously, low-frequency (LF) power increases, indicating a transition toward sympathetic dominance, which correlates with heightened physiological stress and arousal 15. The result is a dangerous feedback loop: heavy cognitive load accelerates decision fatigue, producing poorly timed market entries. These errors generate emotional frustration, adding extraneous emotional load, which further erodes processing capacity and cascades into exponential error rates 21.

Neurobiological Interventions for Cognitive Fatigue

Experimental interventions suggest that physiological fatigue in these environments requires neurological resetting rather than simple passive rest. Interventions such as high-frequency repetitive transcranial magnetic stimulation (rTMS) applied to the left dorsolateral prefrontal cortex (DLPFC) between sustained attention tasks have been shown to promote the reorganization of large-scale brain networks. Specifically, rTMS modulates long-range fronto-temporal connectivity, shifting the brain toward a more efficient topological state characterized by increased local efficiency and clustering coefficients. This non-passive intervention successfully mitigates mental fatigue and preserves reaction times in high-stress cognitive environments 16.

Institutional Versus Retail Behavioral Dynamics Under Stress

The physiological drivers of trading behavior scale from the individual operator to aggregate market cohorts. A distinct bifurcation exists between retail participants and institutional entities in their behavioral response to extreme market stress and volatility.

Performance Disparities and Capital Outflows

Retail investors historically suffer disproportionate capital losses during periods of high volatility, underperforming institutional benchmarks. Quantitative studies spanning 20-year periods indicate the average retail investor underperforms the S&P 500 by approximately 6.1% annually, with the gap widening to 5.5% in bull market years like 2023 17. This deficit is largely attributed to emotionally driven capitulation - selling assets at the nadir of a market downturn and missing the subsequent mathematical rebound 17. The psychological toll is severe, with tracking data showing that 80% of retail day traders quit the profession entirely within their first two years 17.

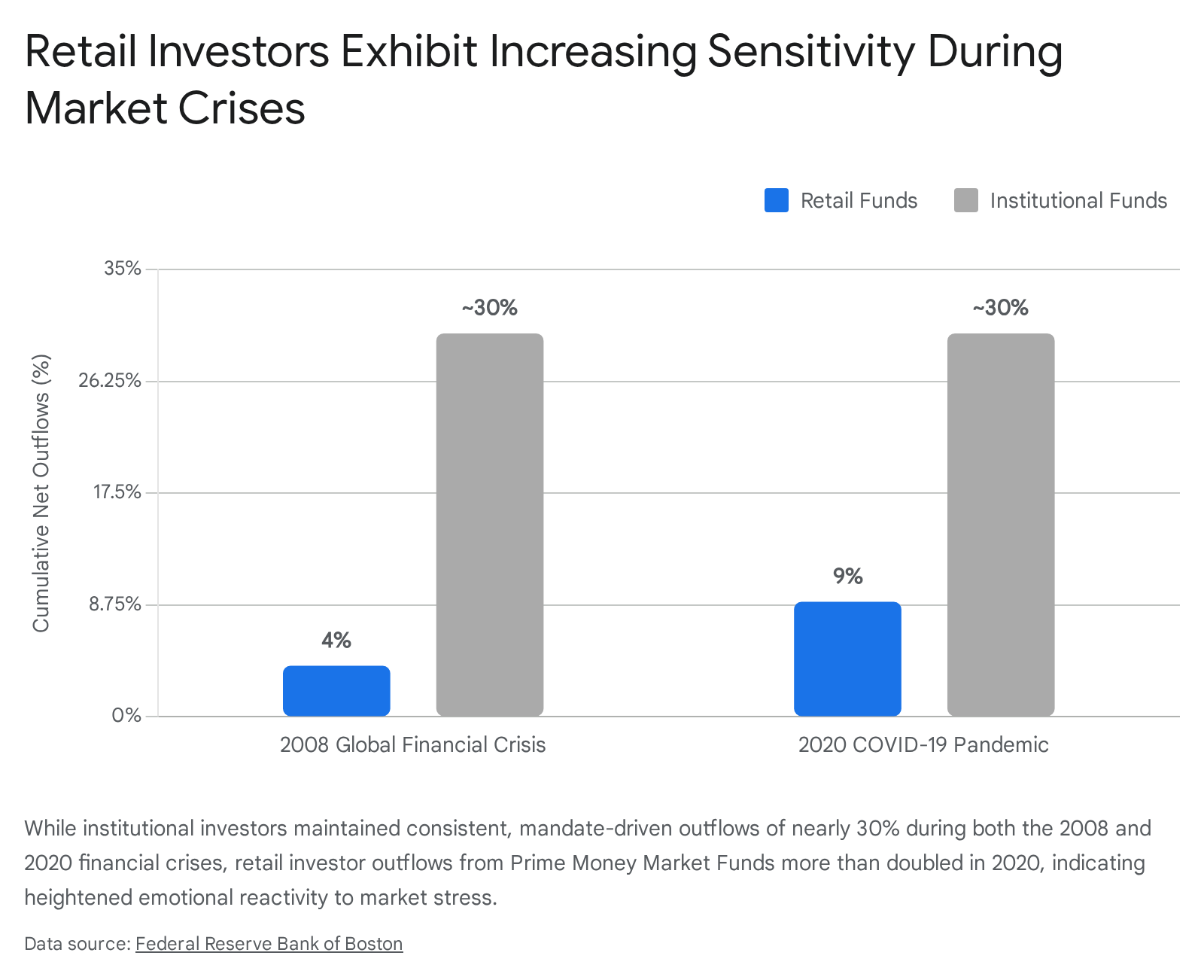

Analyses of Prime Money Market Funds (MMFs) highlight an increasing retail sensitivity to systemic stress compared to their institutional counterparts. During the 2008 Global Financial Crisis, retail prime funds experienced cumulative outflows representing roughly 4% of their assets 18. In contrast, during the liquidity crisis of the COVID-19 pandemic in March 2020, retail outflows from identical vehicles more than doubled to 9% 18.

While institutional MMFs experienced massive, highly rational outflows of nearly 30% in both crises due to strict cash-management mandates and corporate treasury requirements, the evolving retail data suggests that everyday investors are becoming increasingly reactive and prone to panic-induced liquidity runs 18.

Retail Amplification of Systemic Volatility

The influx of retail trading directly amplifies market variance. During the severe equity market selloff from late February through April 2020, institutional investor sentiment dipped significantly below levels seen in previous years, driving cautious outflows. Conversely, retail sentiment remained irrationally bullish, aggressively buying the dip despite macro-uncertainty 19. Statistical analysis of 4,024 unique stocks during the pandemic period demonstrates that the causal effect of retail trading on range-based market volatility was approximately 30% greater during the pandemic than in pre-pandemic environments 20. Driven by behavioral biases such as loss aversion, overconfidence, normalcy bias, and the fear of missing out (FOMO), emotionally uncalibrated retail cohorts exacerbate price swings and disassociate market dynamics from economic realities 21222324.

Algorithmic Mitigation and Algorithmic Herding

In contrast to retail emotionality, the institutional landscape is increasingly dominated by algorithmic execution. As of 2024, algorithmic systems account for roughly 65% to 90% of U.S. equity trading volume 32. Algorithms provide a structural advantage by strictly adhering to embedded risk parameters, circumventing the psychological friction that plagues human discretionary traders 32. Data indicates that professional human traders deviate from their own predefined risk rules approximately 23% of the time, typically due to fear after a loss or overconfidence following a gain, whereas automated systems adhere to parameters 100% of the time 32.

However, algorithms introduce a different systemic risk: "algorithmic herding." During crisis events, the collective, automated withdrawal of liquidity by momentum-based or volatility-triggered algorithms creates a feedback loop. While detached from human emotion, these cascading sells mimic human panic, resulting in precipitous correlation breakdowns and exacerbating endogenous financial instability 22.

Cross-Cultural Variances in Risk Perception

The physiological and psychological drivers of trading behavior are further modulated by the cultural framework of the market participant. Traditional financial models assume that risk aversion is a universal constant; however, cross-cultural studies utilizing the Conjoint Expected Risk (CER) model reveal significant variances in how risk is perceived and tolerated across different geographic cohorts 2534.

The Cushion Hypothesis and Risk Assessment

Empirical comparisons between investors in the United States and the People's Republic of China demonstrate that Chinese cohorts consistently display higher levels of financial risk tolerance 263627. In standardized risk tolerance assessments and pricing experiments for risky financial options, Chinese respondents were significantly less risk-averse, demonstrating a higher willingness to pay for lotteries and speculative gambles compared to Americans and Western Europeans 3627.

This variance is primarily explained by the "cushion theory." The theory posits that in collectivist cultures, dense social and familial networks provide an implicit financial safety net. If an individual suffers a severe financial loss, the extended social network acts as a cushion, allowing the individual to take greater financial risks. Conversely, in highly individualistic societies like the United States, the absence of this collectivist cushion makes the consequences of financial ruin more severe, naturally enforcing higher risk aversion 36.

Interestingly, these cross-cultural differences are localized to financial decisions. In medical or academic decision-making domains where social networks offer no direct mitigation of the consequences, Chinese cohorts do not display higher risk tolerance than their Western counterparts 36. Furthermore, content analysis of proverbs reveals that Chinese cultural texts actively provide more risk-seeking advice regarding financial matters than German or American proverbs 36.

| Assessment Dimension | Western Cohorts (e.g., U.S., Germany) | Collectivist Cohorts (e.g., China, Taiwan) |

|---|---|---|

| Financial Risk Tolerance | Lower relative tolerance; highly sensitive to the magnitude of potential losses. 3427 | Higher relative tolerance; willing to engage in speculative options. 3627 |

| Perception of Risk vs. Attitude | High apparent risk aversion driven by perception of options as inherently riskier. 27 | High risk-seeking behavior driven by differing perceptions of the actual risk, not just a preference for danger. 3427 |

| Social vs. Financial Risk | Symmetrical risk aversion across both social and financial domains. 36 | Asymmetrical; highly risk-seeking in finance, but risk-averse in personal/social domains. 36 |

| Theoretical Mechanism | Individualistic structures require personal absorption of total financial loss. 36 | "Cushion Theory": robust social networks socialize the downside of financial ruin. 36 |

Real-Time Biometric Tracking and Emotion Engineering

The advancement of neurofinance relies heavily on the ability to quantify ambiguous physiological states in real time. Historically, researchers have faced a critical tradeoff between controlled internal validity (the laboratory) and external validity (the chaotic live market environment) 2829. Modern behavioral tracking increasingly leverages multi-modal wearable biometrics to capture unfiltered physiological data without interfering with a trader's workflow.

Wearable Sensing Technologies

Advanced smart eyewear utilizes a non-invasive sensing method called Optomyography (OMG) to capture high-resolution facial muscle movements. Operating at 50 Hz, infrared-based optical sensors track 3D movement (X, Y, Z axes) of the skin 30. By monitoring the frontalis (eyebrow raises indicating surprise or stress), the corrugator (center brow frowns indicating concern), and the zygomaticus major (cheek movement indicating smiles and reward), algorithms can map real-time emotional valence without the intrusive constraints and hygiene issues of traditional electromyography (EMG) sticky electrodes 30.

When these facial metrics are fused with physiological inputs like electrodermal activity (EDA, measuring skin conductance as a proxy for arousal) and electrocardiograms (ECG, measuring heart rate variability), modern machine-learning models achieve remarkable accuracy. Studies indicate that ECG features alone can achieve 94.19% accuracy in basic emotion detection, while EDA signals perfectly register emotional triggers with a root mean squared error of just 0.9871 3142. These systems allow quantitative firms to build automated "circuit breakers" that monitor a trader's emotional arousal and enforce mandatory risk reductions when biological metrics indicate extreme cognitive fatigue or heightened stress.

The Laboratory-to-Live Replication Gap

Despite technological advances, interpreting behavioral finance data requires rigorous methodological skepticism. Human behavior inside an artificial, controlled laboratory environment - such as a 2-hour mock trading exercise with simulated lottery games - rarely maps perfectly to a 6-day live field study where real capital is at risk 2829. The lack of actual financial devastation or career risk in lab settings inherently depresses the cortisol responses that drive true market panics 29.

Furthermore, the behavioral and social sciences suffer from documented replication challenges. In systematic replication projects analyzing experimental economics studies published in high-impact journals, only about 61.1% of studies successfully replicated with significant effects in the original direction, and replicated effect sizes were on average only 66% of the original 32. To combat this "false positive" crisis, researchers advocate for "replication marketplaces" and registered reports, ensuring that neuroeconomic findings regarding trader psychology reflect structural truths rather than statistical anomalies before they are codified into market architecture 3334.

Synthesis of Physiological and Behavioral Market Drivers

The intersection of psychology and financial P&L is governed by immutable biological realities. Rationality in financial markets is not a default human state; it is a fragile cognitive condition that must be actively managed and protected. Endocrine shifts dictate an individual's appetite for risk, with testosterone fueling overconfidence during bull markets and cortisol triggering paralytic risk aversion during volatility. Acute sleep deprivation and cognitive load compound these errors, degrading the prefrontal cortex and anterior insula to a point where probabilistic thinking and loss-mitigation become neurologically compromised.

Cultural frameworks further dictate the baseline acceptance of risk, while the rapid influx of retail capital has demonstrated how untrained, emotionally reactive cohorts can exponentially amplify systemic market variance. For institutional and retail participants alike, acknowledging these physiological and psychological constraints is the first step toward robust risk management. As biometric tracking technologies mature and algorithmic execution democratizes, the future of trading performance will increasingly rely not just on superior financial data, but on the real-time quantification and regulation of human biology.