How to Keep a Trading Journal That Improves Your Results

A trading journal is an essential, structured feedback loop that transforms random market speculation into a measurable, data-driven business operation by logging quantitative metrics, qualitative psychology, and macroeconomic market context. Modern journaling methodologies replace simplistic accounting ledgers with advanced analytics to track R-multiples, enforce rule adherence, and facilitate systematic daily, weekly, and monthly reviews. Utilizing these structured platforms prevents emotional gambling, optimizes statistical edge across global asset classes, and is widely mandated by elite proprietary trading firms to ensure continuous metacognitive improvement.

The Paradigm Shift: From Casino Speculator to Systematic Business Owner

The financial markets offer an environment of absolute freedom, lacking the external structures, managerial oversight, or rigid operational guidelines that characterize traditional professional environments. This boundless, unstructured environment presents a profound psychological trap: without self-imposed structure, market participants naturally default to treating the market like a casino 12. The defining characteristic of this casino mindset is an obsession with prediction and immediate outcomes - chasing disparate strategies, reacting to impulsive emotions like the fear of missing out (FOMO), and viewing the market as an adversarial entity to be "beaten" or outsmarted 23.

Pioneering trading psychologists Mark Douglas and Brett Steenbarger extensively documented the absolute necessity of abandoning this chaotic mindset in favor of treating trading as a formalized, highly regulated business 24. Douglas emphasized that long-term trading success relies on executing probabilities over predictions; the market owes the trader nothing, and the primary obstacle to profitability is the psychological need to be right on every single execution 25. Steenbarger advanced this philosophy by likening an effective trading journal to a daily business plan 4. A business plan outlines anticipated operational setups, acknowledges systemic weaknesses, and establishes protocols for exploiting market opportunities. If trading is a business, the trading journal is its foundational operational ledger, quality assurance mechanism, and research and development department combined.

The transition from retail speculation to professional trading requires replacing emotional reactions with structured, metacognitive review processes. This evolution forces the trader out of a chaotic environment governed by hope and fear, and into a highly organized business environment characterized by data dashboards, structured review routines, and objective performance metrics. The vocabulary of the casino trader - using words like "hope," "revenge," "YOLO," and "lucky" - acts as a cognitive virus that shuts down the brain's prefrontal cortex, blocking objective risk management 35. Conversely, treating trading as a business requires adopting an "Alchemist Protocol," a linguistic and structural framework that turns every market loss into tuition paid for valuable data, refining the underlying system 5.

The Accounting Ledger Myth

A pervasive and damaging misconception among retail market participants is that a trading journal is merely an accounting ledger - a sterile log of ticker symbols, entry prices, exit prices, and net profit or loss (P&L) 61. While tracking capital fluctuations is necessary for calculating account equity and tax liabilities, an accounting ledger is inherently silent on the most critical variable of performance: why the outcome occurred 68.

If a trader only records financial outcomes, they remain completely blind to the behavioral and strategic context driving those numbers. An accounting ledger cannot distinguish between a highly disciplined, perfectly executed trade that resulted in a statistical loss and a reckless, rule-breaking impulse trade that resulted in a lucky profit 69. Consequently, an accounting ledger actively reinforces bad habits by rewarding luck, whereas a true trading journal breaks negative behavioral loops by exposing the underlying decision-making process, the emotional state of the operator, and the systemic adherence to the predefined edge 69.

The Professional Sports "Game Tape" Analogy

To understand the functional utility of a comprehensive trading journal, behavioral finance experts and elite prop firm managers frequently draw direct parallels to professional sports and competitive games 12111213. Professional athletes do not simply compete on game day relying on raw instinct; they spend thousands of hours off the field reviewing game tape to identify blind spots, analyze opponent tendencies, and correct mechanical flaws in their own execution 1211.

Skipping the journaling process is equivalent to an athlete refusing to watch replay footage after a devastating loss 211. When a basketball player reviews tape, they see the lazy defense or poor shot selection that they could not objectively perceive in the heat of the moment 2. Similarly, a chess grandmaster reviews past matches to understand exactly where their strategic foresight failed 14. A trading journal strips away the emotional distortion of real-time market execution, replacing post-trade rationalization with cold, irrefutable data 2. It forces the trader to confront the reality of their execution: did they hesitate when the setup perfectly aligned? Did they increase risk sizing following a loss in a desperate attempt to exact revenge on the market? 21115. The journal acts as the ultimate psychological mirror, transforming random market losses into structured, tuition-paid lessons that prevent the repetition of errors 152.

FAQ: What Exactly Should Go in a Trading Journal?

The components of an effective trading journal must capture the totality of a market event, seamlessly blending mechanical execution data with psychological state tracking and environmental factors. To prevent the journal from devolving into a useless emotional diary or a sterile accounting ledger, the data must be highly structured.

A professional journal categorizes data into three distinct, interdependent pillars: Quantitative Metrics, Qualitative Metrics, and Market Context 1617183.

Quantitative metrics measure the what and the how much. These are the hard, numerical data points that define the financial parameters of the trade, fitting neatly into databases for statistical analysis 16. They are essential for calculating mathematical expectancy, maximum drawdown, and the statistical validity of the edge 173. However, relying solely on quantitative data can be misleading if separated from human behavior. Qualitative metrics explore the why and the how. These metrics capture the subjective, non-numerical nuances of human behavior, emotional regulation, and psychological biases 1618. Behavioral finance research indicates that qualitative data is critical for understanding the root causes of execution errors, exposing the cognitive processes that drive the numbers 1617. Finally, Market Context records the external environment. Because trading strategies are highly regime-dependent, tracking the broader macroeconomic and structural market conditions prevents a trader from discarding a mathematically valid strategy during an temporarily incompatible market phase 421.

| Metric Category | Specific Data Field | Description & Primary Purpose |

|---|---|---|

| Quantitative | Instrument & Direction | The ticker symbol (e.g., EUR/USD, AAPL, BTC/USDT) and trade direction (Long/Short), identifying asset-specific proficiencies 422. |

| Quantitative | Entry & Exit Prices | The exact mechanical fill prices, utilized to calculate slippage and deviation from planned execution levels 4. |

| Quantitative | Position Size & Risk | The absolute capital or percentage of account equity allocated, critical for preventing catastrophic drawdowns 1323. |

| Quantitative | Commissions & Slippage | Tracks gross P&L versus net P&L; essential for identifying "commission drag" eroding high-frequency strategies 215. |

| Quantitative | Holding Period | The exact time elapsed between entry and exit, identifying whether winning trades are cut too early or losers are held too long 425. |

| Qualitative | Strategy / Setup Tag | A predefined label (e.g., "Breakout," "Mean Reversion") allowing performance filtering by specific edge to determine what works 2126. |

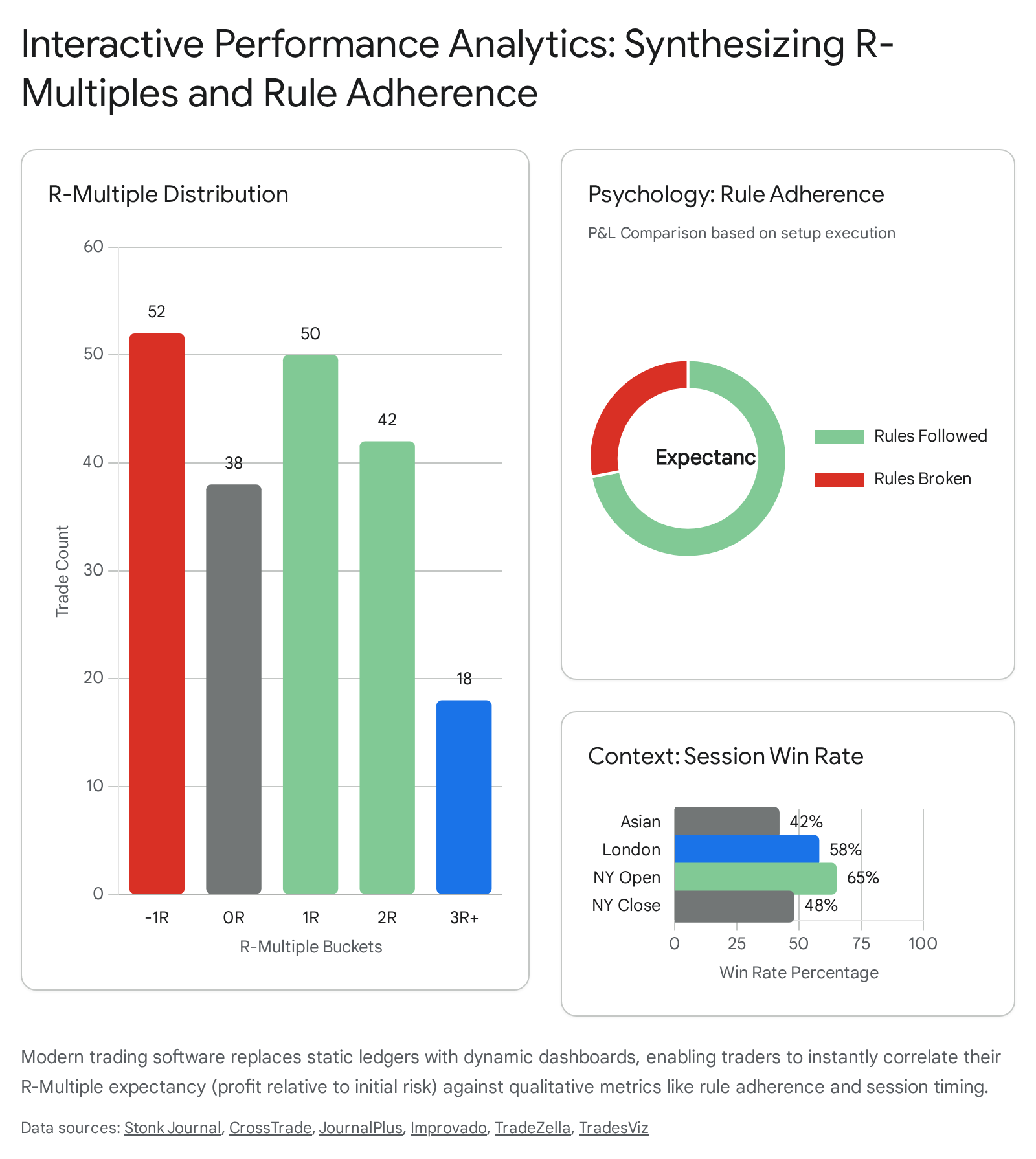

| Qualitative | Rule Adherence | A binary (Yes/No) field confirming if the trade strictly followed the pre-defined business plan; the single most important qualitative metric 927. |

| Qualitative | Emotional State | Categorical tags (e.g., FOMO, Revenge, Confident, Anxious) documenting the psychological triggers present during execution 272829. |

| Qualitative | Execution Grading | A subjective assessment (A/B/C) of setup quality, allowing expectancy analysis based on the perfection of the trade plan 825. |

| Market Context | Time of Day / Session | Identifies performance dependencies across specific liquidity windows (e.g., London Open, NY Close, Asian Session) 2122. |

| Market Context | Market Regime | Classifies the broader market environment (e.g., Trending, Range-Bound, High-Volatility, Low-Liquidity) 21. |

| Market Context | Macroeconomic Catalyst | Notes structural drivers such as CPI reports, earnings releases, or central bank decisions directly impacting the asset's volatility 4. |

FAQ: What is an R-Multiple?

Developed and popularized by trading psychologist Dr. Van K. Tharp in his seminal work on position sizing, the R-Multiple is universally considered the most critical quantitative metric a professional trader can track 3031. The "R" stands for the initial risk taken on a trade 3233. An R-Multiple expresses the final profit or loss of a trade strictly as a multiple of that initial defined risk, rather than in absolute currency amounts 303133.

To calculate the initial risk (1R), a trader determines the financial difference between their entry price and their predefined protective stop-loss level, multiplied by the total position size 303334. For example, if an equities trader buys a stock at $50 and places a hard stop-loss at $48, the risk per share is $2. If they purchase 250 shares, the total initial risk (1R) for that specific execution is $500 3031.

The outcome of the trade is then divided by this 1R value to generate the R-Multiple: * If the trade hits the stop-loss and the trader loses exactly their planned $500 risk, the outcome is recorded in the journal as -1R 3033. * If the trade moves favorably and is closed at $56, generating $1,500 in total profit, the outcome is +3R (since $1,500 is three times the initial $500 risk) 3031. * If the trader panics, violates their plan, and exits early for a $250 loss, the outcome is recorded as -0.5R 3233.

The mathematical power of the R-Multiple lies in its ability to standardize performance 3133. Absolute dollar amounts are highly deceptive; a $5,000 profit is meaningless without context. Earning $5,000 while risking $50,000 (+0.1R) represents exceptionally poor reward-to-risk mechanics and a highly vulnerable portfolio, whereas earning $5,000 while risking $500 (+10R) is an indicator of profound market edge 2131. By tracking R-Multiples, traders can seamlessly compare the efficacy of strategies across wildly different asset classes, account sizes, and market volatilities; a +2R outcome on a single micro-futures contract holds the exact same statistical weight as a +2R outcome on a ten-million-dollar institutional bond position 3032.

Furthermore, calculating the Average R-Multiple across hundreds of trades yields the system's "Expectancy" - the mathematical average of what a trader can expect to earn or lose per unit of risk expended over time 3033. Expectancy dictates long-term survival; a strategy with an average outcome of +0.3R to +0.5R across hundreds of trades is mathematically guaranteed to generate substantial wealth, completely independent of the underlying asset's nominal price fluctuations 30.

FAQ: How Often Should I Review My Logged Trades?

The mere act of logging data is insufficient; sustained improvement requires the aggressive, continuous synthesis of that data through structured review 828. Behavioral finance research highlights the necessity of "metacognitive regulation" - the psychological capability to actively monitor, evaluate, and control one's own cognitive processes and decision-making heuristics 67. Traders with high metacognitive awareness consistently outperform those who operate on autopilot, as they can accurately detect when their mental models are drifting from objective reality 8. Regular journal reviews serve as the primary structural mechanism for enforcing this metacognitive feedback loop.

To optimize this loop and prevent data overload, expert guidance and proprietary trading firm methodologies suggest a highly stratified review schedule, divided into daily, weekly, and monthly horizons.

The Daily Review: The Emotional Reset

The daily review should be brief, taking no longer than 5 to 10 minutes, and must occur immediately after the trading session closes 825. The objective of this phase is not deep statistical analysis, as the daily sample size of executions is far too small to yield statistically significant data 38. Instead, the daily review focuses entirely on execution fidelity and emotional awareness.

Traders must quickly tag each trade to identify deviations from the business plan, record the presence of impulsivity, fatigue, or "tilt," and assess strict rule adherence 839. Did the trader execute the setup exactly as planned? Were stops moved out of fear? This rapid feedback loop forces the trader to externalize their internal state, preventing emotional baggage and cognitive distortions from carrying over into the following session 2940.

The Weekly Review: Pattern Recognition

The weekly review is the cornerstone of the journaling process, requiring 30 to 60 minutes of dedicated analysis, typically conducted over the weekend 840. During this time, the trader aggregates the week's data to detect emerging behavioral and strategic patterns before they inflict catastrophic damage on the portfolio 2140.

A highly effective weekly review is interrogative, designed to answer specific, actionable questions: Did the win rate or profit factor drastically shift during specific times of day? Did subjective "A-grade" setups perform as mathematically expected? Were financial losses heavily correlated with a specific emotional tag, such as overconfidence following a winning streak, or boredom during low-volatility sessions? 82528. The trader then distills these insights to formulate one highly specific, actionable focus area for the upcoming week, ensuring continuous, incremental improvement 89.

The Monthly/Quarterly Review: Strategic Optimization

Statistical edge requires a significant sample size - typically a minimum of 20 to 50 executions of identical setups - before a trader can make objective, mathematically sound alterations to their core strategy 38. The monthly or quarterly review is designed for macroscopic analysis, evaluating aggregated R-Multiple distributions, overall market regime shifts, and total portfolio drawdown against predefined risk limits 3940. At this level, traders use the journal to fundamentally adjust risk parameters, expand operations to new asset classes, refine algorithmic constraints, or mercilessly discard broken setups that no longer possess a verifiable edge 21.

Nuances Across Global Markets: Crypto, Forex, and International Equities

A comprehensive trading journal must be uniquely adapted to the structural realities and idiosyncratic mechanics of the specific asset class being traded. The assumption that a standard, domestic stock-trading template functions universally is a primary cause of statistical distortion for multi-asset speculators.

Cryptocurrency: Extreme Volatility and Continuous Market Hours

Cryptocurrency markets operate 24 hours a day, 7 days a week, 365 days a year, fundamentally altering the traditional concepts of "overnight risk," market gaps, and session boundaries 2326. A crypto trading journal must account for factors entirely non-existent in traditional equities, such as the impact of funding rates on perpetual futures contracts, complex on-chain volatility metrics, and aggressive altcoin sector rotations 26.

The most critical journaling adjustment required for crypto is the method of position sizing and stop-loss tracking. Because the baseline volatility of crypto assets is often 5 to 10 times higher than major fiat currencies or blue-chip stocks, utilizing raw price distance or fixed percentages for stop-losses is mathematically flawed 23. A 0.25% stop-loss might survive for hours on a stable forex pair like EUR/USD, but will be hunted and triggered in seconds on an asset like Bitcoin or Solana 23. Consequently, a crypto journal must track stop-loss distances in direct relation to the asset's Average True Range (ATR) - a standardized measure of historical volatility 2332. By logging risk in ATR multiples rather than raw points or pips, traders ensure their exposure adjusts dynamically to extreme market conditions 2332. Additionally, the journal must track effective volatility exposure rather than raw leverage; a 5x leveraged position on Bitcoin carries roughly the same daily P/L swing potential as a 50x leveraged position on a major forex pair 23.

Foreign Exchange (Forex): Session Volatility and Pip Calculations

The foreign exchange market is characterized by distinct global trading sessions (Asian, London, New York) and heavily relies on real-time macroeconomic data releases 42223. A forex-specific journal must categorically track the time-of-day session, as a strategy that demonstrates a profound statistical edge during the overlapping liquidity of the London-New York window may face devastating drawdown in the low-volume, mean-reverting Asian session 2223.

Furthermore, because the monetary value of a "pip" fluctuates wildly depending on the base currency, quote currency, and lot size (e.g., the pip value of EUR/USD differs vastly from exotic pairs like USD/TRY or EUR/GBP), the journal must accurately track exact lot sizes and pair specifications to calculate true dollar risk and expectancy 22. For traders utilizing proprietary (prop) firm capital - such as those trading FTMO or FundedNext challenges - the journal must also overlay rigid institutional parameters, specifically tracking daily and maximum absolute drawdown limits in real-time to avoid breaching strict evaluation rules that standard stock journals entirely ignore 22.

International Equities: Currency Risk, Stamp Duties, and Transaction Taxes

Trading international equities introduces profound layers of macroeconomic risk, foreign exchange exposure, and heavy sovereign taxation that must be explicitly accounted for in a journal's quantitative metrics to reveal true net performance and cost of capital 91011.

Currency Risk (FX Exposure) When a domestic investor purchases foreign stocks in their local currency, they are effectively placing two simultaneous, independent trades: one on the fundamental performance of the underlying company, and one on the performance of the foreign currency relative to their domestic currency 910. For example, U.S. investors holding European equities will see their aggregate returns eroded if the US Dollar strengthens against the Euro, as those foreign corporate profits convert back into fewer domestic dollars 91012. A sophisticated international equity journal must meticulously track unhedged versus hedged performance to determine if the alpha generated by superior stock selection is being nullified by adverse, macroeconomic currency fluctuations 101213.

Taxation and Regulatory Levies: The United Kingdom and India Failing to meticulously log geographic-specific transaction costs can rapidly turn a gross-profitable strategy into a net loser, a phenomenon known as "commission drag" 21. * The United Kingdom: Traders purchasing UK-listed shares are subject to the Stamp Duty Reserve Tax (SDRT), an immediate 0.5% levy applied to electronic share purchases through the CREST system (excluding AIM-listed shares) 46141516. Combined with standard platform fees, a short-term UK equity trader can immediately lose 1-2% of their total trade value to structural costs upon entry 4616. An accurate UK trading journal must auto-calculate this 0.5% SDRT drag to locate the true, mathematically viable breakeven point. Furthermore, the journal must legally segregate assets subject to Capital Gains Tax (CGT) - which operates under strict Section 104 pooling rules - from entirely tax-free vehicles like Spread Betting 461516. * India: The Indian stock market presents extreme regulatory nuances that fundamentally alter retail trading behavior. In 2024, the Indian government enacted sharp increases to the Securities Transaction Tax (STT) on derivatives, raising the levy by a massive 150% on futures (to 0.05% of notional turnover) and 50% on options (to 0.15% of premium turnover) 1718. Because the STT on futures is levied on the total notional contract value rather than just the premium exchanged, the mathematical cost of executing futures strategies increased exponentially, devastating the edge of high-frequency traders 1718. A journal focused on the National Stock Exchange (NSE) or Bombay Stock Exchange (BSE) must auto-calculate these aggressive STT levies, alongside GST and SEBI turnover fees 52. Behavioral data indicates these tax hikes force active retail traders to migrate toward synthetic futures constructed via complex options to escape the notional tax burden 17; consequently, a premier Indian market journal must be capable of tracking multi-leg options strategies to evaluate the efficacy of these structural adaptations 185253.

The Minimum Viable Journaling Routine

The primary reason novice traders rapidly abandon their journals is complexity overload. Attempting to track thirty distinct variables per trade - from moon phases to macroeconomic indicators - leads to analytical paralysis and burnout within weeks 854. The solution is implementing a "Minimum Viable Routine" - a frictionless, highly focused process designed solely to build the habit of metacognitive review before layering in advanced analytics 4054.

Step-by-Step Implementation for Beginners

- Automate Mechanical Data Capture: Manual data entry (price, size, time, fees) guarantees inconsistency and human error 4055. Traders must utilize a tool that imports basic fill data automatically via broker API or CSV upload 4054. If entering manually, only the absolute minimum fields should be tracked.

- Limit Custom Fields to the Core Four: Initially, track only the absolute necessities beyond price and size: Strategy Name, Setup Quality (A/B/C Grade), Rule Adherence (Yes/No), and a brief, one-sentence post-trade note capturing the emotional state at execution 8254054.

- The 30-Day "No Optimization" Window: For the first 30 days (or 20 - 30 trades), the singular goal is habit formation, not profitability 3854. The trader must execute their plan, risk an exceptionally small amount of capital (e.g., $25 or 0.5% per trade), and log every single outcome without exception 956. During this phase, the trader must actively resist the urge to tweak the strategy or alter rules based on a statistically insignificant sample size 3854.

- Execute the Review Cadence: Spend a maximum of 5 minutes daily ensuring all trades are tagged 8. Spend 30 minutes every weekend reviewing the aggregate data, focusing primarily on the "Rule Adherence" metric over absolute P&L 89.

- Expand Gradually: Only after 30 days of flawless logging and reviewing should a trader introduce more complex fields, such as detailed market regime tagging, specific emotional trigger mapping (e.g., separating FOMO from revenge trading), or complex R-Multiple distribution studies 938.

Limitations and Pitfalls: Logging Without Actionable Review

Even a well-maintained, highly detailed journal becomes useless if corrupted by poor data practices, cognitive biases, or an absence of scheduled reflection. The behavioral finance literature points to several critical limitations that actively destroy journal efficacy.

The Write-Only Diary Syndrome The most fatal journaling mistake is logging data meticulously but failing to aggregate and analyze it 828. A journal that is never systematically reviewed is merely a diary; it may offer temporary emotional catharsis or a false sense of productivity after a difficult trading session, but it generates zero statistical improvement 828. Without the metacognitive feedback loop of a scheduled review, the data sits dormant, and the trader inevitably repeats the exact same neurological errors 2838.

Selective Logging and the Omission Bias Human psychology is inherently defensive; facing the mathematical reality of poor decisions and lack of discipline is painful 411. Consequently, struggling traders often commit the cardinal sin of selective logging - diligently recording their winning trades while conveniently "forgetting" to log humiliating, rule-breaking losses, or waiting until the end of the month to batch-enter data from a distorted memory 42139. Selective logging instantly invalidates the journal's mathematics. A win-rate metric missing 20% of its losing data points provides a false sense of security, leading to dangerous over-leveraging and eventual account destruction 21.

Overanalyzing Insufficient Sample Sizes Conversely, the psychological phenomenon known as the "law of small numbers" causes traders to overreact to statistically insignificant data 38. Altering a strategy, firing a setup, or changing risk parameters after analyzing only five trades introduces extreme strategy drift and guarantees inconsistency 38. True behavioral and strategic patterns require a minimum sample size of 20 to 50 identical setups before the data becomes statistically reliable enough to warrant a change in the underlying business plan 38.

Automated Software vs. Manual Spreadsheets (Post-2023 Analysis)

Historically, traders constructed elaborate Microsoft Excel or Google Sheets workbooks to track performance 555758. While spreadsheets offer infinite customization and zero upfront software cost, their utility sharply degrades at scale 5758. Once a trader surpasses roughly 20 to 50 executions per month, the manual entry of entry prices, exit prices, times, and commissions becomes an unsustainable bottleneck, consuming hours of administrative work 55575960. Furthermore, complex spreadsheets are plagued by "formula drift" - a single broken cell reference or improperly dragged column can silently corrupt months of P&L and expectancy data without the trader realizing it 575859.

Post-2023, the trading journal software industry experienced rapid acceleration, integrating direct broker API synchronization, big data analytics, and artificial intelligence 5860. Platforms such as TradesViz, TraderSync, TradeZella, and TraderLens have fundamentally shifted the standard for performance tracking across the retail and proprietary trading industries 27286162.

These dedicated applications completely remove the friction of data entry by automatically importing thousands of trades in seconds, instantly calculating highly complex metrics like Maximum Favorable Excursion (MFE) and Maximum Adverse Excursion (MAE) 2752575860. Modern platforms also feature deep integration with AI engines (such as ReflectIQ and TraderSage) that automatically analyze historical datasets to detect hidden psychological pitfalls, highlight periods of emotional tilt, group complex options strategies automatically, and generate personalized coaching insights based on the trader's actual execution history 53616364.

| Feature / Capability | Manual Spreadsheet (Excel, Google Sheets) | Dedicated Journal Software (Post-2023 AI platforms) |

|---|---|---|

| Data Entry Process | 100% manual. High risk of human error, missed trades, and fat-finger typos 555758. | Fully automated via Broker API or CSV direct import. Zero manual entry for trade mechanics 555758. |

| Time Investment | 15 - 30 minutes daily (8-10 hours monthly) for active traders just for data input 5760. | Under 5 minutes daily for review. Saves 50 - 80% of administrative time, focusing effort on analysis 5760. |

| Customization | Infinite. Traders can build bespoke formulas for highly unique, niche metrics 555759. | High, but inherently constrained by the software's UI and predefined metric structures 55. |

| Scalability & Integrity | Poor. Workbooks become sluggish and extremely prone to "silent" formula breakages past 1,000 rows 575859. | Excellent. Cloud databases easily and instantly manage tens of thousands of trades without performance loss 5760. |

| Visual Analytics | Basic. Requires advanced developer-level skills to build dynamic dashboards or option payout charts 5558. | Native. Instantly generates interactive equity curves, MFE/MAE scatter plots, and time-of-day heatmaps 2752575861. |

| AI Integration & Coaching | Non-existent 27. | Advanced. AI assistants detect strategy leaks, flag emotional patterns, and offer specific rule enforcement 2753586364. |

| Operational Cost | Free (excluding the significant opportunity cost of time) 575860. | Monthly subscription ($10 - $50+), requiring a positive ROI justification based on saved time and improved performance 5558. |

Proprietary Trading Firm Practices and Academic Research

The absolute necessity of strict journaling and structured performance review is heavily corroborated by academic literature in behavioral economics, personality psychology, and the rigorous internal training protocols of elite proprietary (prop) trading firms.

Academic Evidence: Metacognition, Big Five Traits, and Self-Monitoring

Peer-reviewed literature consistently demonstrates that human beings are fundamentally ill-equipped for the probabilistic, unstructured environment of the financial markets due to deeply ingrained evolutionary cognitive biases 1966. Retail investors frequently exhibit highly destructive "feedback trading" patterns, driven by herd mentality, profound overconfidence, and a biological aversion to realizing losses (loss aversion) 196667.

Psychological studies utilizing experimental financial markets indicate that a participant's ability to engage in "metacognition" - the psychological capability to monitor, evaluate, and correct one's own thought processes and emotional responses - is directly correlated with superior, long-term financial performance 67820. Research by Biais et al. (2005) specifically demonstrated that participants exhibiting high "self-monitoring" traits - individuals who are hyper-aware of external feedback and rapidly adjust their behavior to align with objective reality - significantly outperformed those plagued by ego-driven overconfidence and miscalibration 212223. Furthermore, studies utilizing the OCEAN (Big Five) personality model reveal that traits like emotional regulation can be cultivated to override compulsive trading dynamics 20.

A trading journal acts as the mechanical apparatus for inducing this essential metacognition 720. By meticulously writing down their pre-trade thesis, tracking their emotional states in real-time, and objectively observing their own metrics, the trader distances their fragile ego from the financial outcome, shifting from a reactive, emotional participant to an objective, scientific observer of their own behavioral anomalies 2920.

Institutional Standards: The SMB Capital Approach

SMB Capital, a highly respected, deeply established proprietary trading firm based in New York, treats the review of trading performance with the exact same rigor as the trading execution itself 247374. According to co-founder Mike Bellafiore, the failure rate in proprietary trading is exceptionally high largely because aspiring professionals refuse to engage in the necessary "deliberate practice" 25.

At SMB Capital, developing traders are strictly required to utilize advanced journaling software to monitor their daily execution against rigid institutional parameters 76. The firm fosters a culture of radical accountability; trading is viewed entirely as a performance-based business where simply "punching the clock" or operating on gut feeling results in immediate failure and termination 25. Through rigorous daily journaling, the use of joint accounts to foster peer-to-peer accountability, and intensive "after the close" tape review, traders meticulously dissect the nuances of their setups, isolating highly specific variables that average retail traders completely ignore 7425. If an SMB trainee is diligently logging their work, following their business plan, and proving continuous metacognitive improvement through the journal, the firm absorbs their capital losses as the cost of education; conversely, a trader who is temporarily profitable but refuses to engage in the structured review process is viewed as a systemic liability operating on borrowed time 25.

Bottom Line

The transition from an amateur, emotion-driven speculator to a consistently profitable professional trader occurs entirely within the metacognitive feedback loop of a structured trading journal. By abandoning the destructive casino mentality and the pervasive myth of the accounting ledger, traders can utilize deep quantitative, qualitative, and market context metrics - particularly the mathematical power of the R-Multiple - to objectively identify and iteratively refine their statistical edge. While manual spreadsheets suffice for low-volume beginners establishing a minimum viable routine, active professionals operating across diverse global markets require the automation, precise tax tracking, and AI-driven insights of modern journaling software to mitigate cognitive biases, accurately account for structural costs, and enforce the rigorous discipline demanded by elite financial institutions.