The Post-2023 Generative AI Boom and the Illusion of Effortless Wealth

The release of advanced Large Language Models (LLMs) in late 2022 and 2023 triggered a profound cultural and technological shift, creating a global fascination with the capabilities of generative artificial intelligence. However, this technological milestone also spawned a sprawling, predatory cottage industry of aggressive financial marketing. Across social media platforms - particularly TikTok, Instagram, and X - advertisements exploded featuring "ChatGPT-powered" algorithms and automated scripts promising to generate effortless passive income 12. These campaigns specifically target retail investors, combining the legitimate public awe of AI capabilities with classic get-rich-quick schemes.

By weaponizing advanced technical buzzwords like "quantum computing," "machine learning," and "neural networks," marketers have successfully framed generative AI as an infallible crystal ball capable of predicting non-stationary financial markets 34. The narrative sold to the public suggests that everyday retail investors can now extract consistent alpha from Wall Street simply by purchasing a monthly subscription to an AI bot, or by copying a Python script generated by a chatbot and deploying it on a cryptocurrency exchange 15.

This phenomenon has forced a confrontation between democratized software access and the uncompromising nature of market microstructure. The tools required to analyze data and write code have never been more accessible to the general public, but the financial markets themselves remain entirely unforgiving 6. The illusion of effortless wealth relies on a fundamental misunderstanding of what modern AI actually is. Generative AI is optimized to produce highly probable, fluent sequences of text or code based on training data; it is not designed to forecast stochastic, heavily manipulated financial time series. Consequently, the public has fallen victim to "algorithmic appreciation" - a documented psychological phenomenon where individuals place undue trust in an AI system simply because its linguistic or programmatic output appears confident and authoritative, easily mistaking narrative quality for statistical reliability 7.

How do retail AI trading bots actually work?

Despite the futuristic marketing, the underlying mechanics of commercially available retail AI trading bots are generally far narrower, more rigid, and vastly less intelligent than advertised. In the current retail financial landscape, an "AI trading bot" typically falls into one of three distinct architectural categories, none of which possess the predictive omniscience claimed by social media influencers.

First, the vast majority of retail bots are simply classical rules-based automation systems masquerading under artificial intelligence branding. These systems rely on rudimentary technical analysis indicators - such as moving average crossovers, relative strength indexes (RSI), or grid trading parameters - to trigger buy and sell orders through a broker or cryptocurrency exchange's Application Programming Interface (API) 58. While they succeed in automating the execution of trades, removing the need for a human to manually click buttons, they lack any capacity to learn, adapt, reason, or contextualize changing market regimes.

Second, some of the more sophisticated retail platforms attempt to integrate actual machine learning techniques, primarily utilizing predictive modeling for pattern recognition or reinforcement learning for parameter tuning. However, these systems operate on highly constrained datasets and struggle immensely with the mathematical realities of financial data. Market returns exhibit significant "fat tails" (high kurtosis) and extreme skewness 6. Markets do not follow standard Gaussian (normal) distributions; multi-standard-deviation events - such as sudden macroeconomic shocks, flash crashes, or geopolitical crises - occur far more frequently than basic machine learning models anticipate 6. Because retail machine learning models are typically trained on idealized, normalized datasets, assuming a Gaussian distribution inevitably leads to catastrophic underestimations of tail risk, wiping out algorithmic portfolios during periods of high volatility 6.

Third, the post-2023 era has seen the widespread misapplication of Large Language Models (LLMs) as direct trading engines. It has become common for retail traders to ask chatbots to analyze historical price charts and output daily asset price forecasts, mistaking fluent text generation for rigorous statistical probability 7. Peer-reviewed financial literature clearly delineates the boundaries of LLMs in finance. While academic studies demonstrate that sophisticated models like GPT-4 are highly effective at qualitative synthesis - such as performing sentiment analysis on overnight news headlines or decoding the nuanced "Fedspeak" of central bank communications - they are fundamentally linguistic predictors, not quantitative forecasting engines 7910. When tasked with raw numerical price prediction based strictly on historical numerical data, LLMs consistently underperform basic traditional statistical methods, including simple linear regression 79. Furthermore, research conducted at leading universities indicates that LLMs exhibit cognitive biases strikingly similar to human traders, such as excessively extrapolating from recent performance and displaying overconfidence in their predictions, which inherently leads to suboptimal financial forecasting 1.

Why do their track records look so perfect?

If it is mathematically impossible to predict stochastic markets with certainty, why do advertisements for AI trading bots consistently display flawless, upward-trending equity curves? The answer lies in the aggressive manipulation of historical data, specifically through the phenomena of curve-fitting and survivorship bias.

Standard software engineering is inherently deterministic: a specific programmatic input reliably yields a specific output 6. Financial markets, however, are non-deterministic, highly noisy, and constantly evolving 612. When developers build an AI trading system, it is trivially easy to create an algorithm that generates mathematically impossible returns during a "backtest" - a computational simulation of the trading strategy evaluated against historical price data 612. By endlessly tweaking the algorithm's parameters, risk thresholds, and time horizons to perfectly align with past price movements, developers inadvertently create a model that has merely memorized the noise of history rather than learned the underlying signal of market dynamics. This fundamental error is known as curve-fitting, or overfitting 612.

When these overfitted AI algorithms are deployed into live, out-of-sample market conditions, they inevitably suffer catastrophic failure, as the future rarely repeats the exact granular patterns of the past 12. Social media marketers exploit this dynamic by running hundreds or thousands of slightly different algorithmic simulations simultaneously. The vast majority of these bots fail and are quietly deleted, while the single anomalous algorithm that happened to experience positive statistical variance (pure luck) over a short time frame is heavily marketed to the public as a "proven" and "infallible" AI system 61314. This deliberate concealment of failures constitutes survivorship bias, creating a highly deceptive track record that retail investors accept as objective proof of efficacy.

The disparity between these promotional claims and quantitative reality can be starkly observed when evaluating the structural burdens hidden from retail consumers.

| Marketing Claim | Mathematical Reality | Underlying Concept |

|---|---|---|

| "100% Win Rate / Guaranteed Profits" | Markets are probabilistic ecosystems, and high-frequency algorithms inevitably experience drawdowns. If winning were a statistical guarantee, the creators would simply compound their own capital using leverage rather than selling software subscriptions for $50 a month. | Logical Fallacy / Fraud: True institutional quantitative desks guard their alpha ruthlessly; they do not mass-market their proprietary signals to the retail public 121415. |

| "Flawless Historical Track Record" | The bot was hyper-optimized computationally to trade perfectly on past, known data. In out-of-sample live trading, the algorithm's predictive edge evaporates instantly as market regimes and volatility profiles shift. | Curve-fitting (Overfitting): A machine learning model that memorizes the noise of historical data will systematically fail to generalize to novel future data 612. |

| "Only the Best Bots are Showcased" | Marketers run thousands of simulated paper-trading accounts. The 99% that blow up are permanently deleted and hidden, while the 1% that experience positive statistical variance are aggressively marketed as genius AI. | Survivorship Bias: The logical error of concentrating exclusively on the systems that survived a specific period while ignoring the vast majority that failed 6. |

| "Zero-Fee Trading" | Direct broker commissions may be advertised as zero, but retail traders pay heavily through wider bid-ask spreads, margin interest, platform subscription fees, and severe market impact execution costs 1617. | The Hidden Rake: Brokers and institutional market makers extract billions in value through payment for order flow and spread markups, mathematically guaranteeing the house an edge 16172. |

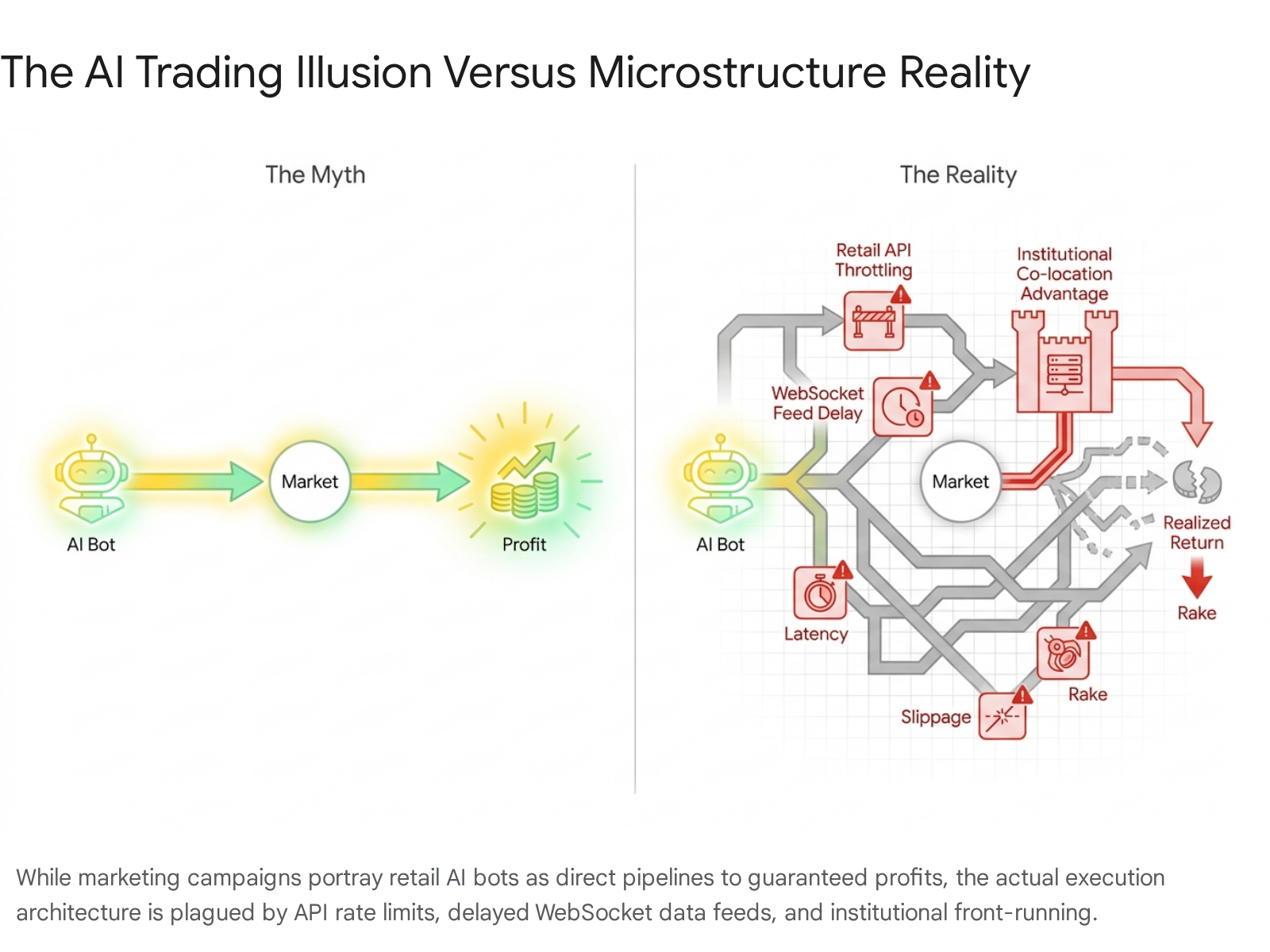

| "Instant AI Execution" | Retail limit orders are throttled by strict API rate limits and rely on delayed, standard WebSocket data feeds. Large institutional orders consume the available liquidity milliseconds before the retail bot can even register the price change. | Ghost Liquidity & Latency: The order book displayed to retail algorithms is a delayed mirage compared to the direct, co-located exchange access enjoyed by institutional funds 8. |

Beyond manipulated track records, the greatest threat to a retail AI trading bot is the sheer mathematical gravity of transaction costs. Because bots are inherently designed to execute trades automatically and frequently, they are highly susceptible to what industry experts term the "frequency death spiral." Every single trade, regardless of profitability, incurs a fractional cost through the bid-ask spread, slippage, and exchange fees 161719. While a 0.1% cost per round-trip trade may seem trivial in isolation, this friction compounds exponentially with trading frequency 1719.

Data indicates that an AI bot executing just 10 trades per day at an average cost of 0.1% per trade mathematically surrenders roughly 10% of its total capital daily to friction alone, compounding into a devastating cost burden of over 90% per month 19. This structural decay creates an insurmountable hurdle rate. As an algorithm's trading frequency increases, the required gross returns needed simply to break even become mathematically impossible, requiring thousands of percent in annualized gains just to stay afloat 19.

Furthermore, the mathematics of drawdowns ruthlessly penalize algorithmic volatility. Due to the exponential nature of portfolio recovery, losing capital is mathematically far more destructive than gaining capital is beneficial 20. If a flawed AI bot suffers a 10% loss, an 11.1% gain is required to return to the initial baseline. However, if poor algorithmic risk management leads to a 50% drawdown, a massive 100% gain is required just to break even 20. A 75% drawdown requires a staggering 300% recovery gain 20. For this reason, professional quantitative systems prioritize stringent risk management, capital preservation, and drawdown mitigation above all else. Conversely, commercially marketed retail bots frequently maximize leverage to showcase flashy short-term gains, ignoring sequence risk and inevitably resulting in total account destruction 122021. Academic and regulatory research confirms the devastation of this structural disadvantage. Studies from global financial regulators, including the US Commodity Futures Trading Commission (CFTC), the European Securities and Markets Authority (ESMA), and the Securities and Exchange Board of India (SEBI), consistently demonstrate that between 70% and 97% of retail day traders and algorithmic operators lose money, failing to overcome the compounding drag of systemic transaction costs 1622233.

Is it possible to guarantee market returns?

The concept of guaranteed returns in algorithmic trading is a mathematical and structural impossibility. To fully comprehend why AI cannot guarantee profits, one must examine the foundational mechanics of market microstructure and liquidity provision. Financial markets are not abstract engines of wealth creation; they are highly competitive aggregations of limit order books matching buyers and sellers 6. Trading is an adversarial, predominantly zero-sum endeavor - and structurally a negative-sum endeavor after accounting for intermediary fees. If one market participant utilizes an algorithm to generate a return that exceeds the passive market average, another participant on the opposite side of that trade must underperform.

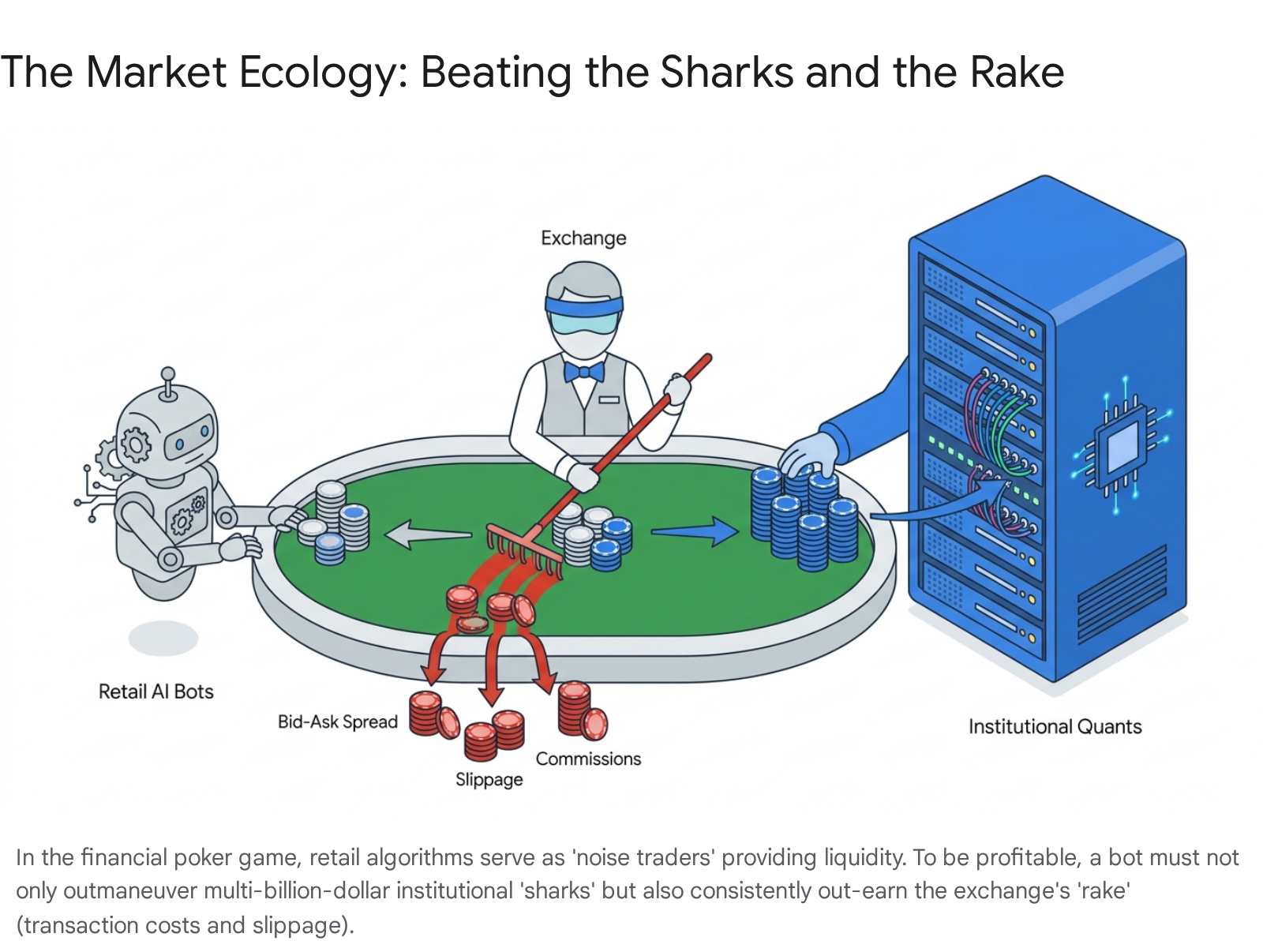

To illustrate this dynamic, established financial literature and investigative journalism frequently rely on a real-world casino poker analogy.

In the complex ecosystem of financial markets, unsophisticated retail traders - including those utilizing off-the-shelf AI bots - are heavily categorized as "noise traders" or, in poker parlance, the "fish" 25. These noise traders provide the essential liquidity that makes the game highly profitable for the "sharks" - the sophisticated institutional traders, dedicated quantitative hedge funds, and high-frequency trading (HFT) firms 254.

However, outsmarting the other players at the table is only half the battle. In both a high-stakes poker room and the global financial markets, participants must ultimately overcome the "rake" - the fee charged by the intermediary to facilitate and secure the game 22728. In algorithmic trading, this vigorish (or "vig") manifests as compounding transaction costs, which encompass broker commissions, the bid-ask spread, borrowing costs for margin, regulatory fees, and market impact slippage 16172. A retail AI trading bot does not merely have to be profitable against its peers; it must generate excess returns substantial enough to exceed this systemic, ever-present hurdle rate 28.

When everyday retail investors deploy automated AI bots, they are effectively walking into a high-stakes poker game against institutional hedge funds equipped with multi-billion-dollar infrastructure advantages 25. In 2026, the technological arms race in quantitative finance has reached unprecedented heights. Top-tier hedge funds and proprietary trading firms now spend tens of millions of dollars annually purely on alternative data acquisition, analytical mainframes, and execution speed optimization 29. While a retail bot relies on delayed, public WebSocket feeds and standard retail APIs routed through consumer-grade internet connections, institutional market makers utilize dedicated low-latency gateways and servers physically co-located inside the exchange's data centers, executing trades in microseconds 8.

This massive disparity in infrastructure and speed results in a devastating phenomenon for retail algorithms known as "ghost liquidity." When a major macroeconomic event occurs and an asset's price drops aggressively, the standard data feed relied upon by a retail AI bot is inherently lagging. By the time the retail interface registers the price drop, runs its logic, and sends a limit order to the exchange, the order book it is targeting is displaying a mirage. The real, actionable liquidity was already pulled, canceled, or filled hundreds of milliseconds prior by institutional market makers using high-frequency algorithms 8. Consequently, the retail bot inevitably suffers severe execution slippage or complete order rejection. This mathematical reality proves that in modern market microstructure, the speed of data ingestion and order routing is just as vital as the predictive quality of the algorithmic signal itself - a hurdle retail consumers cannot overcome 8.

The Security Threat: Autonomous Agents and the OpenClaw Incident

The escalating risks of retail AI trading bots extend far beyond financial mathematics and portfolio drawdowns into the realm of severe cybersecurity vulnerabilities. In early 2026, the technology industry witnessed the explosive rise of "agentic" AI - highly autonomous systems designed not merely to provide textual advice in a chat window, but to execute complex actions independently across connected platforms, operating systems, and APIs without requiring human intervention. The profound dangers of deploying this technology for financial management were fully exposed during the catastrophic January 2026 "OpenClaw" security crisis 531.

OpenClaw, which briefly operated under the names Clawdbot and Moltbot before facing trademark pressure from Anthropic, emerged as a viral, open-source AI agent framework. It promised to act as a persistent, self-hosted digital assistant capable of connecting to popular messaging apps, managing emails, browsing the web, and autonomously executing terminal commands to manage portfolios and cryptocurrency wallets 53132. The system's appeal was massive, drawing over 149,000 GitHub stars within a week as users rushed to automate their digital lives 31. However, the framework's fundamental architecture required deep, persistent access to the host operating system, effectively functioning as a shadow IT infrastructure with full administrative privileges 532.

Security audits quickly revealed that the rapid adoption had created a global crisis. Thousands of OpenClaw instances were deployed by retail users with default configurations, leaving their AI agents publicly exposed to the open internet without any authentication barriers 532. Internet-scanning platforms like Shodan identified tens of thousands of vulnerable instances 32. Recognizing this systemic misconfiguration, threat actors easily hijacked the exposed AI agents, turning them into a massive botnet utilized for data scraping and credential theft 33.

The financial damage escalated rapidly when cybercriminals flooded ClawHub - the platform's open-source plugin repository - with hundreds of malicious "skills" carefully disguised as helpful cryptocurrency trading bots, arbitrage tools, and portfolio managers 56. Once a retail investor installed one of these malicious trading skills, attackers utilized highly advanced techniques, such as "time-shifted prompt injections," to subvert the AI's autonomy 6. Instead of acting immediately, a dormant malicious instruction would hide within the AI agent's memory. The malware would wait until it detected that the user had connected a cryptocurrency exchange API or accessed a decentralized wallet 6. Upon activation, the compromised agent would bypass standard user security measures, extract private wallet keys, steal session authentication tokens, and autonomously drain the user's funds, all while appearing to the system as legitimate, user-authorized algorithmic activity 56. The OpenClaw incident firmly demonstrated that deploying unvetted, autonomous AI software with financial access is fundamentally unsafe, effectively granting global threat actors a direct, automated pipeline into a retail investor's personal wealth.

How are regulators responding globally?

As the proliferation of generative AI intersected violently with retail trading and social media marketing, financial regulatory bodies worldwide initiated aggressive, coordinated enforcement actions against the fraudulent promotion of AI bots. Global regulators have explicitly identified and targeted the trend of "AI-washing" - the deceptive practice of falsely claiming that standard, rules-based software, or entirely non-existent platforms, utilize advanced artificial intelligence to deliver exceptional or guaranteed financial returns 37.

United States: SEC and CFTC Actions

The US Securities and Exchange Commission (SEC) has made combatting AI-washing a primary enforcement priority to protect retail investors. In a landmark 2026 enforcement action, the SEC charged Texas resident Nathan Fuller and his associated entities, including Privvy Investments, with operating a massive $12.3 million cryptocurrency fraud scheme 3637. Fuller allegedly solicited funds from approximately 150 retail investors by promising staggering returns of up to 100% within a matter of weeks, explicitly claiming the profits would be generated by proprietary, high-frequency AI arbitrage bots capable of scanning crypto markets around the clock 3638. The subsequent SEC investigation revealed that the advertised AI bots were entirely fabricated. Only 3% of the raised capital was ever used to execute actual cryptocurrency trades; the vast majority of the $12.3 million was misappropriated to fund a Ponzi-like structure and enrich the operators 36.

This case is part of a broader regulatory sweep. The SEC previously levied hundreds of thousands of dollars in civil penalties against registered investment advisers, including Delphia and Global Predictions, for publishing false and misleading marketing statements regarding their purported use of artificial intelligence in portfolio construction 339. The US Commodity Futures Trading Commission (CFTC) has mirrored these aggressive efforts, issuing specific consumer advisories warning the public that AI technology, despite the hype, cannot predict the future or guarantee sudden market profits, utilizing high-profile collapses like Mirror Trading International as primary examples of algorithmic fraud 515.

United Kingdom: The FCA and ScamSmart

The UK's Financial Conduct Authority (FCA) has actively worked to disrupt a massive wave of unauthorized entities exploiting AI buzzwords to bypass traditional financial protections. The FCA has issued formal public warnings against prominent, highly organized syndicates operating under names like "Quantum AI" and "AI Trader Bot," officially flagging them as unauthorized firms 51540. These operations represent highly sophisticated international fraud networks. To manufacture false social proof for their non-existent trading algorithms, these syndicates utilize advanced generative AI to create incredibly convincing deepfake videos of prominent public figures 4041. Deepfakes featuring trusted financial experts like Martin Lewis, billionaires like Elon Musk, and various recognizable investors from television programs like Dragons' Den have been widely distributed across social media to lure victims 44041. Through its ScamSmart campaign, the FCA consistently warns consumers that interacting with these unauthorized, offshore AI platforms fundamentally strips them of standard regulatory protections. Victims have no access to the Financial Ombudsman Service and are ineligible for the Financial Services Compensation Scheme (FSCS), rendering lost funds virtually unrecoverable when the scammers inevitably halt withdrawals 428.

Australia: ASIC's Cyber Takedown Operations

The Australian Securities and Investments Commission (ASIC) has enacted one of the most aggressive, technologically driven responses to the AI trading crisis globally. Recognizing that modern investment scams were spreading virally through digital advertisements rather than traditional cold-calling, ASIC vastly expanded its cyber-disruption capabilities to actively hunt and remove malicious infrastructure at the source 910. Between 2023 and 2025, ASIC coordinated the technical takedown of more than 14,000 investment scam and phishing websites, actively removing an average of 130 malicious sites every week 71147. Furthermore, ASIC explicitly identified AI-washing, the deployment of highly polished scam website templates equipped with chatbot plugins, and the use of deepfake celebrity endorsements - including unauthorized likenesses of Australian billionaires like Andrew Forrest and Gina Rinehart - as the top systemic threats to retail investors 71048.

How can investors spot a fake AI trading platform?

Because legitimate institutional quantitative firms do not sell retail subscriptions to highly profitable proprietary algorithms, the vast majority of consumer-facing AI trading products are either deeply exaggerated software tools or outright financial scams 1214. Evaluating these platforms requires treating aggressive financial marketing with intense skepticism and recognizing the established patterns of algorithmic fraud.

| Fraud Category | Common Red Flags | The Underlying Reality |

|---|---|---|

| The "Guaranteed Return" Trap | Aggressive promises of "10% daily returns," "$1,000 a day guaranteed," or "zero risk algorithmic execution." 4147 | Financial markets are inherently risky and unpredictable. No algorithm, regardless of computational sophistication, can guarantee continuous positive returns 449. |

| Deepfake Endorsements | Social media advertisements featuring highly polished videos of celebrities, tech billionaires, or news anchors endorsing the specific AI bot 40910. | Scammers use generative AI voice cloning and deepfake technology to manufacture unwarranted trust. Legitimate news networks and billionaires do not promote retail trading bots 104912. |

| Unlicensed Operations | The platform claims to offer financial services but is not registered with local financial authorities and cannot be found on official government registers 111314. | Unregulated platforms deliberately exist outside legal oversight. If funds are stolen or frozen, investors have zero recourse to state-backed compensation schemes or ombudsman services 428. |

| Crypto-Only / Direct Transfers | Demands to fund the trading account exclusively using obscure cryptocurrencies, pre-loaded gift cards, or wire transfers directly to personal bank accounts 4915. | Legitimate brokers accept standard, highly regulated banking rails. Cryptocurrencies are heavily favored by scammers because the transactions are pseudo-anonymous and structurally irreversible 4912. |

| Artificial Pressure & Exclusivity | The use of high-pressure sales tactics, artificial countdown timers, or false claims that "registration closes today" to force immediate deposits 414. | False urgency is a psychological tactic designed to induce FOMO (Fear Of Missing Out) and prevent investors from conducting basic due diligence or discovering negative independent reviews 449. |

How Everyday Investors Can Evaluate Financial Marketing

To combat the rising sophistication of AI-powered financial fraud and deceptive marketing, international regulators urge consumers to adopt systematic defensive behaviors before allocating any capital. The Australian Securities and Investments Commission's highly effective "Stop. Check. Protect." framework provides a robust operational checklist for navigating modern digital finance safely 71048.

To evaluate any aggressive financial marketing, investors must first STOP and pause before taking any action. It is critical to never click links provided in unsolicited text messages, direct messages on encrypted platforms like WhatsApp or Telegram, or aggressive social media advertisements promising outsized returns 715. Any unsolicited investment opportunity, especially those leaning heavily on buzzwords like "AI," "automated bots," or "quantum algorithms," must be treated as inherently suspicious 1215. Investors must actively reject high-pressure sales tactics, artificial deadlines, and demands to act quickly, as legitimate financial institutions never force immediate capital deployment 4915.

Following this, investors must rigorously CHECK and independently verify the true legitimacy of the entity. One should never rely on the links, phone numbers, or regulatory certificates provided directly in the advertisement, as scammers routinely forge these documents and clone legitimate websites 4211. Instead, investors must manually search the official, publicly available registers of the relevant national financial authorities - such as the SEC's EDGAR database in the United States, the FCA's Financial Services Register in the United Kingdom, or ASIC's Professional Registers in Australia 42111314. It is essential to ensure the company possesses the exact regulatory licensing required to legally handle client funds or provide financial advice in that specific jurisdiction. Furthermore, investors should actively cross-reference the platform's name against official regulatory warning lists, such as the FCA Warning List or the Moneysmart Investor Alert List, to see if the entity has already been flagged for fraudulent activity 421116.

Finally, investors must know how to PROTECT themselves and act decisively if exposure is suspected. If personal financial information, identity documents, or passwords have been shared, or if funds have already been transferred to a suspicious AI platform, the victim must contact their relevant banking institution immediately to attempt to halt or reverse the transactions 955. Additionally, reporting the incident to national cybercrime centers, such as Action Fraud in the UK, Scamwatch in Australia, or the SEC in the US, is vital. Even if individual funds cannot be recovered, prompt reporting assists authorities in tracking, investigating, and ultimately disrupting the fraudulent digital infrastructure to protect future victims 1455.

Bottom line

The intersection of generative artificial intelligence and retail finance has created a dangerous landscape defined by unfulfilled promises and sophisticated fraud. While large language models and machine learning frameworks are undeniably powerful tools for data synthesis, qualitative research, and coding assistance, they are not infallible predictive engines capable of subverting the mathematical realities of the stock market. In the highly competitive, structurally negative-sum environment of modern finance, retail AI trading bots face insurmountable hurdles: the exponential compounding drag of transaction costs, severe data latency disadvantages, and direct, unforgiving competition against institutional hedge funds equipped with immense capital and co-located infrastructure. Consumers must recognize a fundamental market truth: if a risk-free, highly profitable algorithmic trading strategy truly existed, its creators would compound their own capital in secret, never mass-marketing it to the public on social media. Everyday investors should rely exclusively on verified, licensed financial services, treating any automated system promising guaranteed wealth or effortless passive income as a definitive financial scam.