Rational management decisions and corporate decline

The fundamental mechanism of corporate failure in the face of technological change is rarely gross incompetence, technological ignorance, or strategic apathy. Instead, empirical evidence across multiple industries demonstrates a profound paradox: the very management practices that allow a company to become an industry leader are precisely the practices that precipitate its decline when confronted with disruptive innovation. This phenomenon, formalized as the innovator's dilemma, describes a structural vulnerability wherein rational, profit-maximizing managerial decisions systematically prevent incumbent firms from investing in the technologies or business models that will ultimately unseat them.

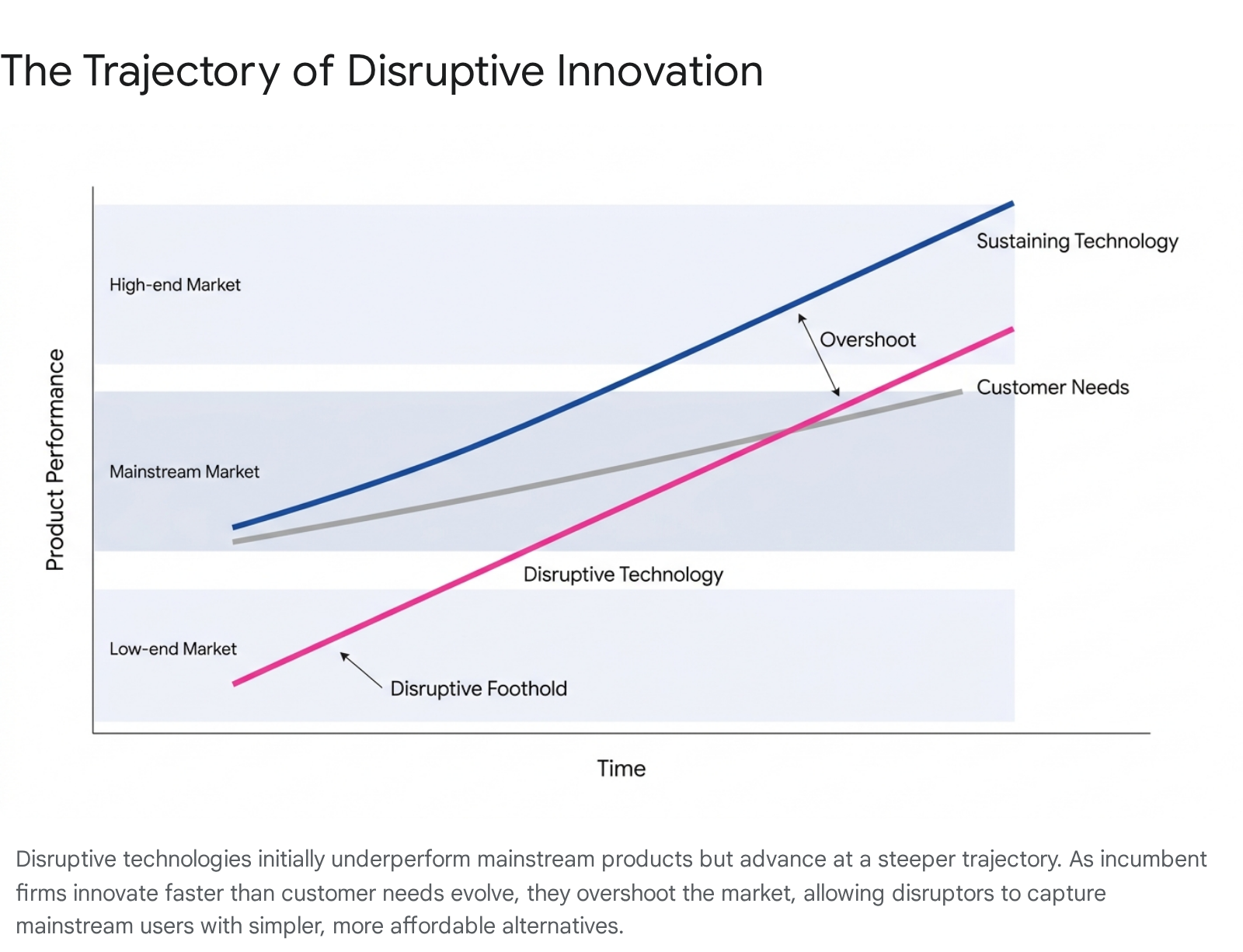

Incumbent organizations are optimized to listen to their most profitable customers, improve their highest-margin products, and allocate capital to projects that clear established internal hurdle rates. When a disruptive technology emerges, it typically presents as an inferior product with low profit margins, appealing only to small, peripheral market segments. For a multi-billion-dollar enterprise, investing substantial resources into a low-margin, small-market product is financially irrational. Consequently, incumbents cede the lower tiers of the market to new entrants. However, because disruptive technologies improve at a rate faster than customers can absorb performance improvements, the entrant eventually moves upmarket, challenging the incumbent in the mainstream and high-end segments with a mature product that retains a structural cost advantage.

Theoretical Foundations of Innovation Strategies

To analyze the mechanics of corporate decline, it is necessary to differentiate between the two primary trajectories of technological progression: sustaining innovation and disruptive innovation. These two forces require distinct organizational capabilities, business models, and strategic responses.

Sustaining Innovation and Incumbent Dominance

Sustaining innovations are improvements made to existing products, services, or processes that are designed to meet the demands of an organization's current, most profitable customers 112. The core objective of sustaining innovation is to solidify a firm's market position by delivering enhanced performance along traditional, well-understood metrics. This approach can involve incremental refinements or radical technological breakthroughs, provided the innovation reinforces the established value proposition.

Established companies consistently win the battles of sustaining innovation because their organizational processes, resource allocation mechanisms, and sales channels are highly tuned to execute these improvements. The financial rationale is straightforward: improving a product for a high-end customer allows the firm to charge premium prices, thereby expanding gross margins 13. By focusing on sustaining innovation, firms minimize risk, guarantee immediate cash flow, and satisfy the rigorous demands of their most lucrative market segments 45.

Disruptive Innovation and Market Entry

Disruptive innovation, conversely, originates in low-end or new-market footholds and initially offers worse performance than existing mainstream solutions, as measured by historical industry standards 16. However, these innovations introduce a new package of attributes - typically involving simplicity, convenience, accessibility, or affordability - that appeals to overserved customers or non-consumers 3.

Because disruptive innovations initially generate low profit margins and serve small, unproven markets, they are structurally unattractive to incumbent firms. The incumbent's resource allocation processes inherently filter out disruptive proposals in favor of sustaining projects that promise higher, immediate returns.

To systematically compare the attributes of these distinct innovation models, the following table summarizes their core characteristics across key strategic dimensions.

| Strategic Dimension | Sustaining Innovation | Disruptive Innovation |

|---|---|---|

| Primary Objective | Enhance existing products for the most demanding, highest-paying customers. | Create accessible, simpler, or more affordable solutions for overserved or new customers. |

| Initial Performance | Superior to previous generations; pushes the technological frontier. | Inferior to established products along traditional performance metrics. |

| Target Audience | Mainstream and high-end tier of the existing market base. | Low-end market segments, niche groups, or entirely new non-consumers. |

| Financial Motivation | Higher profit margins and revenue preservation. | Low-margin, high-volume models, or entirely novel revenue architectures. |

| Impact on Incumbents | Solidifies the market leadership of established industry giants. | Undermines incumbents by rendering their cost structures and value networks obsolete. |

| Technological Trajectory | Often exceeds the capacity of users to absorb the performance improvements. | Rapidly improves to eventually meet the performance requirements of mainstream users. |

The Paradox of Rational Management

The mechanism that transforms successful companies into victims of disruption is not managerial failure, but rather the flawless execution of traditional corporate management principles. Standard financial and strategic frameworks dictate that capital should be allocated to initiatives with the highest risk-adjusted returns, and that management should closely monitor the needs of their largest clients. This creates an asymmetric motivation paradigm.

Margin Optimization and Customer Retention

When a new technology enters the market, it typically does so in a low-end foothold. For an incumbent firm, analyzing this new market reveals a customer base that is small, lacks purchasing power, and demands a product with lower gross margins than the incumbent's current offerings. The rational response for the incumbent's resource allocation process is to reject investment in the disruptive technology and instead funnel capital into sustaining innovations that serve high-end customers who demand better performance and are willing to pay premium prices 13.

This dynamic forces the incumbent to flee upmarket. As the incumbent abandons the low-margin tiers, the disruptive entrant claims them, generating revenue to fund further research and development. The entrant's product improves, eventually reaching the quality thresholds demanded by the mainstream market. By the time the disruptive product is capable of satisfying the incumbent's core customers, the entrant has achieved scale, established a lower cost structure, and built momentum that the incumbent cannot counter without destroying its own profit margins 15.

The Impact of Value-Based Equity Grants

The structural inability of incumbents to respond to disruptive threats is deeply exacerbated by modern executive compensation architectures. A substantial body of research indicates that specific equity-based compensation models systematically weaken executive motivation to pursue long-term, high-risk innovation 78.

The widespread adoption of value-based equity grants - where executives receive a fixed monetary value of stock regardless of the share price at the time of the grant - creates a specific disincentive for bold strategic pivots. Because the total value of the grant is effectively capped, stronger stock performance resulting from successful long-term innovation actually results in the executive receiving fewer shares in subsequent grants 7. This structure diminishes the reward for driving long-term shareholder gains and encourages executives to prioritize compensation predictability and short-term earnings per share optimization 79.

Studies spanning thousands of publicly traded firms in the United States between 2006 and 2022 confirm that companies relying heavily on value-based grants demonstrate a markedly reduced appetite for risk and lower levels of investment in research and development 7. In these environments, corporate governance mechanisms, even when robust, fail to correct the disincentives created by the compensation structure 7. Executives facing the innovator's dilemma - who must choose between a highly profitable, sustaining innovation with a guaranteed short-term return and a speculative, low-margin disruptive project - are structurally incentivized by their pay packages to choose the former.

Option Incentives and Innovation Capacity

Conversely, research demonstrates that altering the compensation model can effectively mitigate the innovator's dilemma. Firms that implement compensation frameworks aligning long-term equity holding with specific innovation metrics exhibit a higher propensity for systemic digital innovation 81011.

An analysis of executive compensation structures reveals that an increased proportion of CEO option compensation relative to total compensation significantly correlates with a rise in the number of patent applications and overall corporate innovation capacity 812. This effect is particularly pronounced in growth-stage enterprises and among male executives, who exhibit a higher baseline propensity for strategic risk-taking 812. In state-owned enterprises and emerging markets, empirical data highlights that long-term equity incentives play a critical role in promoting independent innovation capabilities, whereas short-term monetary incentives yield no measurable impact on innovation output 101113.

Historical Case Studies in Corporate Decline

To understand how the mechanics of margin optimization and rational resource allocation operate in practice, it is instructive to examine the systemic decline of dominant market leaders across different sectors. In each instance, failure was not the result of a lack of technical capability, but a structural inability to adopt a business model that conflicted with the core revenue engine.

Blockbuster and the Revenue Model Addiction

The collapse of Blockbuster Video in the face of competition from Netflix serves as a premier illustration of the innovator's dilemma driven by revenue model addiction. In 2000, Netflix, an unprofitable startup relying on postal delivery for DVD rentals, offered to be acquired by Blockbuster for $50 million 151617. The offer was rejected by Blockbuster's executive leadership, who categorized the DVD-by-mail service as a small, unprofitable niche business that posed no existential threat to their core operations 151714.

At the time, this decision was financially and strategically rational. Blockbuster was generating $6 billion in annual revenue and possessed an undisputed dominance in physical retail video rental 1516. Furthermore, a massive component of Blockbuster's profitability was derived from late fees, which accounted for approximately $800 million annually at the company's peak 1615. Netflix's subscription model, which explicitly eliminated late fees and allowed consumers to keep DVDs indefinitely, represented a direct threat to Blockbuster's most lucrative margin generator 1615.

To compete with Netflix, Blockbuster would have had to aggressively dismantle the physical retail infrastructure that served as its primary asset, while simultaneously sacrificing its $800 million late-fee revenue stream to adopt a lower-margin, capital-intensive centralized warehousing model 1516. Blockbuster's management chose to optimize its existing value network. By the time broadband internet enabled Netflix to pivot from physical DVDs to digital streaming, transitioning from a low-end product disruption to a completely new consumption paradigm, Blockbuster was structurally incapable of responding 1516. Netflix transformed into an enterprise valued in excess of $150 billion, while Blockbuster descended into bankruptcy 17.

Eastman Kodak and the Threat of Cannibalization

The trajectory of the Eastman Kodak Company highlights the vulnerability of firms possessing an overwhelming market share tied to highly profitable consumable goods. For much of the twentieth century, Kodak maintained an effective monopoly, controlling up to 90% of the United States film market and 85% of camera sales 162117. The company's business model relied on selling inexpensive hardware to generate recurring, high-margin revenue from photographic film, chemical development, and printing paper 1617.

Kodak's failure was not rooted in technological blindness; a Kodak engineer invented the first digital camera in 1975, and the firm invested heavily in digital imaging research throughout the 1990s 2118. Internal market studies accurately predicted the eventual rise of digital photography, forecasting a ten-year window before it would threaten traditional film 18. However, Kodak's executive leadership viewed digital technology as a direct threat to their chemical-based profit engine 18.

When Kodak did aggressively enter the digital camera market with its EasyShare brand, achieving the top position in United States digital camera sales by 2005 with $5.7 billion in revenue, the company was actually losing money on every hardware unit sold 1621. Because Kodak's organizational architecture and financial expectations were anchored to the lucrative printing business, leadership failed to recognize that digital photography had shifted the industry's value proposition from physical printing to online sharing and digital display 21. The company attempted to force a disruptive technology into a sustaining business model. Unwilling to sacrifice short-term profitability and cannibalize their legacy operations, Kodak ceded the future of digital media consumption to agile competitors, eventually filing for bankruptcy in 2012 211718.

Nokia and the Architectural Dilemma

Between 1992 and 2007, Nokia established sustained dominance in the global mobile phone industry, achieving a global market share of 38% in 2007 and controlling an estimated 70% of the nascent smartphone market 192021. Nokia's hardware was highly durable, and its Symbian operating system was masterfully engineered for devices with extreme hardware constraints, requiring as little as 128 MB of RAM to provide 48 hours of talk time 27.

The introduction of Apple's iOS in 2007 and Google's Android in 2008 precipitated Nokia's rapid decline, reducing its smartphone market share to just 3% by the early 2010s 20. The failure of Symbian was a classic architectural dilemma. Symbian was a device-centric, monolithic operating system written natively in C++ 1927. It was highly fragmented; by 2009, Nokia was simultaneously managing 57 incompatible versions of the software, as custom code had to be written for specific handset variations 192127.

Nokia's management, facing immense pressure to maintain margins on hundreds of millions of low-end and mid-tier devices, chose to continually patch the fragmented Symbian architecture rather than abandon their massive installed base to adopt a completely new ecosystem 202122. Nokia spent $3.9 billion on research and development in 2010 alone - nearly triple the average of its rivals - with a third of that budget dedicated to sustaining Symbian 19. Despite these immense resources, the firm collapsed because competition had fundamentally shifted from hardware optimization to software ecosystems and multi-sided digital platforms.

| Architectural Feature | Symbian (Nokia's Legacy System) | Android (The Disruptive Entrant) |

|---|---|---|

| Kernel Structure | C++ monolithic architecture. | Linux modular architecture. |

| Primary Advantage | Extreme resource efficiency and battery optimization. | Flexibility and rapid deployment of software updates. |

| Development Ecosystem | Closed and fragmented; highly customized per device model. | Open-source foundation with a unified Java/Kotlin stack. |

| Application Ecosystem | Limited third-party engagement; peaked at roughly 5,000 applications. | Vast developer community; scaled to millions of applications globally. |

| Touch Interface Strategy | Delayed adaptation; initially reliant on resistive touch and styluses. | Built for capacitive multi-touch gestures from inception. |

Evolution of Disruption Theory

As global markets have digitized and become increasingly interconnected, the mechanisms of corporate disruption have evolved beyond the original product-centric framework proposed by Clayton Christensen. Modern strategic management literature identifies new patterns of market upheaval driven by connectivity, platforms, and complex networks of partners.

Ecosystem Disruption and Value Inversion

Research led by strategy scholar Ron Adner expands the focus of disruption from head-to-head product substitution to the broader architecture of value creation. An ecosystem is defined as the alignment structure of a multilateral set of partners required for a focal value proposition to materialize 2923.

While classic disruption involves an entrant using a different technology to capture market share through lower costs, ecosystem disruption occurs when new value architectures redefine the nature of competition entirely, rendering traditional industry boundaries obsolete 24. This frequently involves complementors - entities that provide products or services that enhance an industry's core offering. Adner identifies a phenomenon termed "value inversion," wherein a complementary technology improves to a point where it ceases to enhance the core product and instead begins to undermine or substitute it entirely 23.

In these scenarios, the disruptive threat does not emerge from a traditional startup attacking from below, but from established partners within the value network shifting their strategic impact from positive to negative 23. Incumbents are often blind to ecosystem disruption because their strategic radars are calibrated exclusively to monitor direct, horizontal competitors rather than vertical complementors within their own supply chain.

Platform Disruption and Multi-Sided Markets

A distinct subset of ecosystem change is platform disruption. Multi-sided digital platforms erode conventional business logic by shifting value creation from a linear supply chain (a pipeline) to a networked market 252627. Platform disruption differs fundamentally from product disruption because it enables massive numbers of decentralized participants to coordinate for mutual benefit, effectively mobilizing excess capacity across society 28.

Once a platform achieves sufficient scale, network effects establish formidable barriers to entry, often resulting in a "winner-takes-most" market dynamic 2937. Incumbents operating traditional pipeline models are structurally disadvantaged against platforms because platforms scale with marginal acquisition costs approaching zero 37. Rather than requiring heavy internal capital expenditure to build physical assets, platforms leverage the assets of third-party producers, allowing them to expand globally at a fraction of the cost incurred by traditional enterprises 2837.

Big Bang Disruption

The digital economy has also given rise to the framework of "Big Bang Disruption," authored by Larry Downes and Paul Nunes. This theory describes innovations that do not follow the traditional, gradual incubation period in niche, low-end markets 253031. Enabled by exponential technologies and unencumbered development cycles, Big Bang disruptors enter the market offering products that are simultaneously better, cheaper, and more customized than incumbent offerings from the very beginning 253040.

Because these disruptors rely on existing digital infrastructure and multi-sided market structures, they bypass traditional customer segmentation entirely. They can capture majority market share almost instantaneously, leading to the rapid, catastrophic collapse of incumbent product lifecycles 2530. This forces incumbents to compete not against slightly inferior, cheaper alternatives, but against vastly superior, rapidly scaling global networks that dismantle entire value chains simultaneously.

Contemporary Manifestations of Ecosystem Disruption

The theoretical principles of disruption, resource allocation, and ecosystem transition are actively reshaping major global industries today. Two of the most prominent ongoing examples are the transition to digital mobile finance in developing markets and the global restructuring of the automotive industry toward electrification.

Mobile Payments and Financial Inclusion in Kenya

The proliferation of mobile money in Sub-Saharan Africa, pioneered by Kenya's M-Pesa, is a definitive example of new-market disruption leveraging network effects. Prior to 2007, legacy commercial banks in Kenya focused their resources on high-net-worth individuals and corporate clients, utilizing traditional branch-based banking models 323334. Serving the rural and low-income population was financially unviable for these traditional banks due to the high fixed costs associated with physical infrastructure and the exceptionally low value of individual transactions 3545.

Safaricom, a telecommunications operator, recognized an opportunity to serve this massive non-consumer base. By utilizing an existing network of airtime vendors as cash-in and cash-out agents, and by leveraging basic USSD technology on prevalent feature phones, M-Pesa bypassed the traditional banking infrastructure entirely 3545. The platform allowed users to transfer micro-amounts of money securely and at an exceptionally low cost, serving an immediate societal need that banks had deemed unprofitable.

Initially ignored by commercial banks as a niche service for low-value remittances, M-Pesa rapidly scaled via powerful network effects. By 2025, the Kenyan digital payments market reached an estimated valuation of $11.2 billion, with mobile money penetration across the adult population reaching 98% 4636. M-Pesa processes an annual transaction value equivalent to roughly 80% of the Kenyan Gross Domestic Product 46. The disruption forced legacy banks to fundamentally alter their business models to avoid obsolescence. To survive, large institutions such as KCB Group and Equity Bank had to integrate their core banking systems with mobile platforms and transition heavily toward digital-first strategies 344637. Today, the market has evolved beyond simple peer-to-peer transfers, shifting toward complex business-to-consumer ecosystems, micro-lending via mobile wallets, and cross-border remittances 354636.

Electric Vehicles and the Automotive Transition

The global automotive sector is currently experiencing a complex, multi-layered disruption driven by electrification, software integration, and shifts in global supply chains. For decades, legacy Western automakers optimized internal combustion engine manufacturing, utilizing strategic joint ventures to dominate emerging markets like China, which served as their primary growth engine 4938.

Companies like BYD approached the market from a distinct disruptive foothold. Originating as a battery manufacturer, BYD vertically integrated its supply chain to produce electric vehicles at a significantly lower cost structure than legacy automakers 5139. By initially targeting the mass market with affordable plug-in hybrid electric vehicles and battery electric vehicles, BYD rapidly expanded its scale. This strategy culminated in BYD unseating Volkswagen as the top-selling car brand in China in 2024, and delivering over 2.2 million electric vehicles globally in 2025 495340.

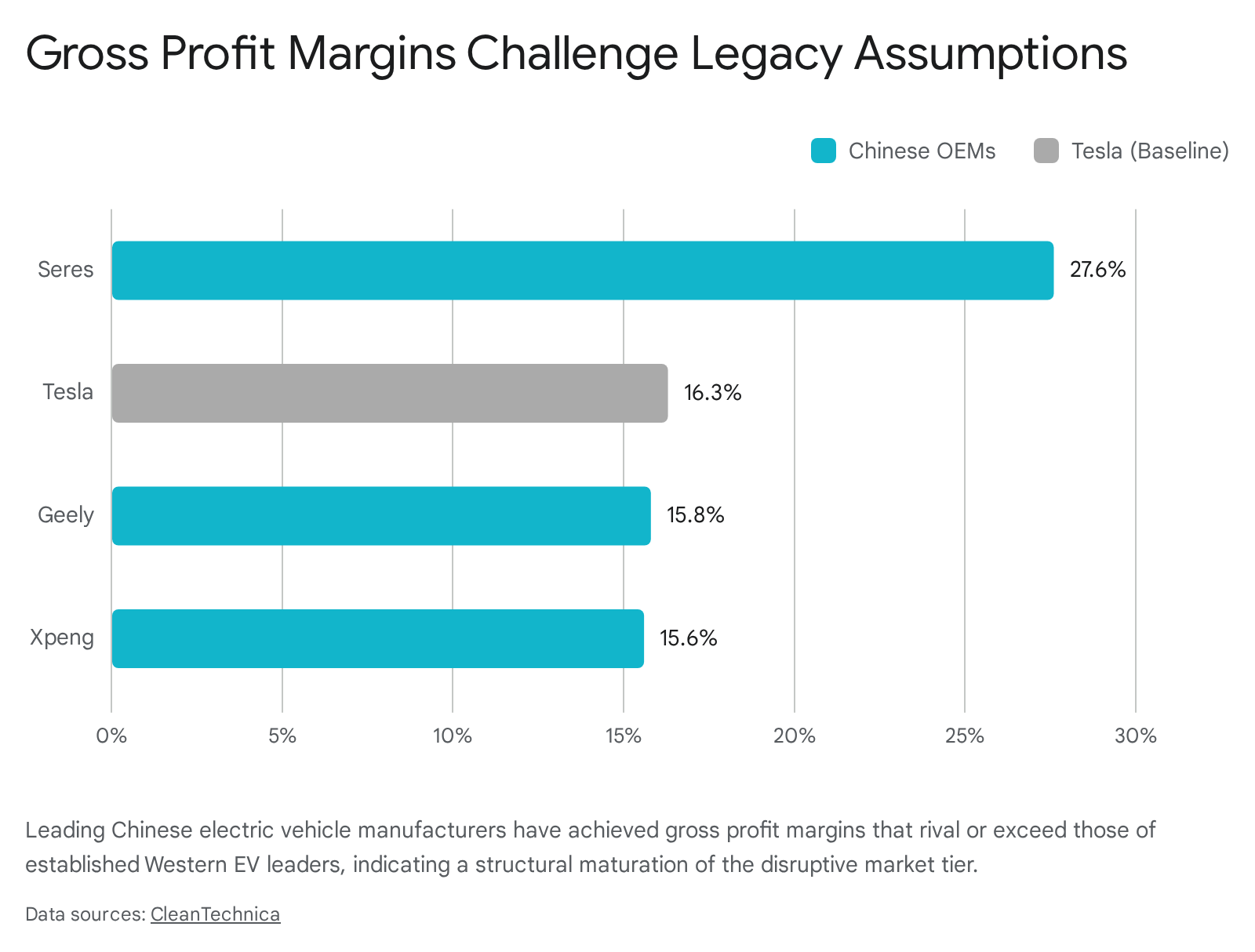

The disruption in the electric vehicle market challenges a core assumption of the traditional innovator's dilemma: the premise that disruptors must inherently suffer from low margins for extended periods. Recent financial disclosures reveal that Chinese pure-play electric vehicle manufacturers are achieving highly competitive profitability. While the broader Chinese auto industry experienced depressed overall profit margins of 4.1% to 4.4% throughout 2025 due to severe domestic price wars 4156, leading electric vehicle disruptors have achieved gross profit margins that challenge or exceed those of established Western leaders.

Despite the overwhelming momentum of the disruptors, the transition remains highly volatile and subject to macroeconomic forces. In early 2026, Volkswagen briefly reclaimed the top spot in passenger vehicle sales in China, capturing a combined 13.9% market share across its joint ventures, while BYD's share temporarily contracted to 7.1%, slipping to fourth place 4953424359. This reversion was primarily driven by the systemic fading of government subsidies for budget electric vehicles and plug-in hybrids, which disproportionately impacted domestic manufacturers reliant on those incentives 494359. Furthermore, legacy manufacturers like Toyota benefited temporarily during this window as consumers shifted back toward conventional hybrids in the absence of purchase tax exemptions for pure electrics 494243.

To illustrate the competitive volatility in the early 2026 Chinese passenger vehicle market, the following table summarizes the market share distribution during this period of subsidy realignment.

| Automaker | Q1 2026 Market Share (China) | Primary Market Strategy |

|---|---|---|

| Volkswagen (FAW/SAIC JVs) | 13.9% | Leveraged legacy brand strength during subsidy contraction. |

| Geely | 13.8% | Diversified portfolio spanning ICE, PHEV, and BEV architectures. |

| Toyota (GAC/FAW JVs) | 7.8% | Capitalized on consumer shifts toward conventional hybrid models. |

| BYD | 7.1% | Faced steep declines due to the expiration of budget EV tax exemptions. |

However, this temporary market share stabilization for incumbents in China does not negate the underlying global ecosystem disruption. Western automakers are simultaneously bleeding margins in crucial overseas markets and spending billions to re-architect their supply chains globally to compete in the electrification era 3851. In the European market throughout 2025, Volkswagen managed to outpace Tesla in total electric vehicle sales, indicating that legacy firms with massive capital resources can execute transitions if they aggressively commit to the new technological paradigm across their entire product portfolio 3960.

Yet, the fundamental structural threat remains severe. Chinese automakers are systematically combining low-cost, vertically integrated manufacturing with advanced digital platforms, forcing legacy incumbents to fight a brutal battle on hardware margins while simultaneously attempting to build the internal software capabilities they historically outsourced to third-party suppliers 3851.

Strategic Interventions for Incumbent Survival

To survive both traditional product disruptions and complex ecosystem transformations, incumbent firms must overcome the rational decision-making constraints that systematically optimize for short-term preservation. Strategic management literature and contemporary corporate case studies suggest several structural and governance interventions necessary to navigate the innovator's dilemma effectively.

First, organizations must recognize that disruptive projects cannot be managed within the same hierarchical structures and financial frameworks that oversee sustaining innovations. The metrics of success, the expected gross margins, and the operational cadence of disruptive technologies are fundamentally incompatible with legacy business models 161. A proven strategic intervention is the creation of highly autonomous business units or the execution of formal corporate spin-offs 6162. By legally and operationally separating the disruptive venture from the parent entity, the organization shields the new unit from the internal "antibodies" of the legacy business 6163. This separation allows the spin-off or autonomous unit to pursue low-margin, high-growth strategies, attract diverse venture capital, and iterate rapidly without being constrained by the parent company's heavy overhead costs or strict quarterly margin requirements 6164.

Second, the structural misalignment of executive incentives must be aggressively addressed by corporate boards. The reliance on rigid, value-based equity grants that penalize long-term risk-taking must be replaced with dynamic compensation philosophies 765. Implementing dual-compensation structures - where a distinct portion of executive remuneration is explicitly tied to long-term innovation metrics, non-financial ecosystem milestones, or the successful commercialization of new platform technologies - can realign management focus toward the extended strategic horizons necessary to survive industry disruption 106644. Providing long-term stock options rather than guaranteed value grants serves to align executive behavior with the risks inherent in deep technological transitions 812.

Finally, incumbents must fundamentally shift their strategic perspective from pipeline defense to active ecosystem orchestration. Rather than viewing emerging technologies solely as direct substitute threats to be defeated in a zero-sum hardware battle, organizations must analyze how broader value architectures are changing 2324. Leaders must determine how to position their firms as indispensable nodes within new multi-sided platforms, forming alliances and partnerships that leverage the innovations of external complementors 243745.

Ultimately, the organizations that survive the innovator's dilemma are those that possess the leadership courage to preemptively cannibalize their own historical profit engines before a disruptor renders them permanently obsolete. Adaptation requires not just technological awareness, but a willingness to fundamentally dismantle and rebuild the corporate architectures that drove past successes.