Asymmetric motivation and incumbent disruptive technology investment

The Theoretical Framework of Asymmetric Motivation

The phenomenon of industry incumbents failing in the face of technological shifts is frequently attributed to corporate inertia, managerial incompetence, or risk aversion. However, strategic management literature, deeply influenced by the foundational work of Clayton Christensen, points to a structural rather than psychological driver: asymmetric motivation 1134. Asymmetric motivation occurs when an established organization is highly incentivized to pursue one class of innovation while systematically avoiding another, creating strategic blind spots that agile entrants actively exploit.

The core of this theory posits that all firms naturally gravitate toward generating the highest possible return on investment. For a mature incumbent, the most rational path to growth is moving upmarket to serve highly demanding, profitable customers with improved iterations of existing products 123. Conversely, disruptive innovations usually emerge at the low end of the market or create entirely new markets out of non-consumers. These early disruptive products are frequently inferior by mainstream standards, operate on significantly lower profit margins, and serve customer segments that the incumbent has deliberately ignored or deemed economically unviable 48.

Because the disruptive opportunity appears financially unattractive compared to the incumbent's core business, the incumbent happily cedes the low-end tier to the new entrant. The entrant is highly motivated to capture these segments because, free of legacy overhead and historical profit expectations, the modest margins represent a highly lucrative growth opportunity 1. To contextualize the mathematics of this asymmetry, a large corporation generating one billion dollars in revenue requires one hundred million dollars in new sales to achieve a modest ten percent growth rate. If the emerging market segment for a disruptive technology is currently valued at two hundred million dollars, the incumbent would need to capture fifty percent of that nascent market in a single year just to move the needle on its corporate growth targets - a virtually impossible feat 1. However, for a startup generating zero revenue and carrying minimal overhead costs, that same two-hundred-million-dollar market represents an enormous and highly attractive opportunity 1. This asymmetry in size and cost structure shields the entrant from competitive retaliation during its fragile early stages.

Sustaining Versus Disruptive Trajectories

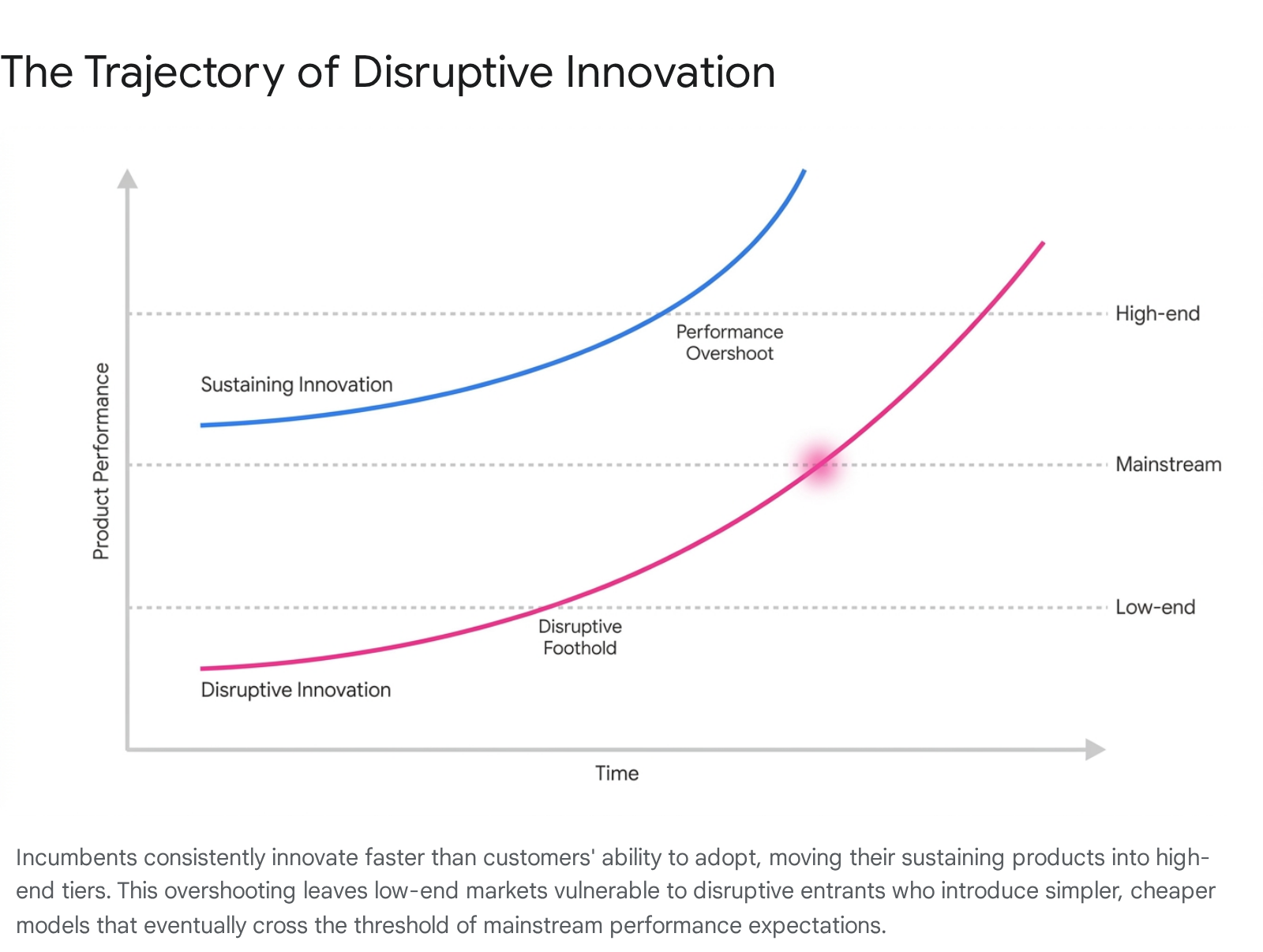

To understand asymmetric motivation, it is essential to distinguish between sustaining and disruptive trajectories. Sustaining innovations improve the performance of existing products along dimensions that mainstream customers historically value - such as faster processing speeds, clearer resolutions, or enhanced software integrations 85. Incumbents almost always win battles of sustaining innovation because the competitive landscape rewards assets they already possess: deep capital reserves, established distribution networks, brand trust, and massive research and development budgets 385.

Disruptive innovations, in contrast, fundamentally change the basis of competition. They introduce products that are cheaper, simpler, or more convenient, frequently utilizing a completely different business model and cost structure 3810. The entrant improves its initial sub-standard product over time. Because the pace of technological improvement typically outstrips the pace of customer demand, the disruptive product eventually crosses a critical threshold, becoming good enough for mainstream customers 8612.

At this inflection point, market share migrations accelerate rapidly, and the incumbent is caught defending an obsolete paradigm.

The distinction between these two trajectories requires examining specific operational characteristics. The underlying financial mechanics, market assumptions, and customer profiles dictate whether a company will view an emerging technology as an existential threat or an irrelevant distraction.

| Investment Profile Dimension | Sustaining Innovation Strategy | Disruptive Innovation Strategy |

|---|---|---|

| Primary Objective | Improve performance for existing high-tier customers | Create new markets or serve overserved, low-end customers |

| Market Size and Certainty | Known, measurable, and highly predictable demand | Initially small, poorly defined, and highly uncertain demand |

| Margin Profile | High and expanding; reinforces existing cost structures | Low initial margins; requires a fundamentally different cost structure |

| Incumbent Motivation | Extremely high (defends core operations, drives near-term returns) | Extremely low (dilutes overall margins, distracts from core accounts) |

| Competitive Advantage | Scale, brand trust, distribution networks, deep engineering capital | Agility, lower cost structure, specialized focus, zero legacy debt |

The Rationality of Incumbent Retreat

When viewed through the lens of asymmetric motivation, the failure of incumbents to invest in disruptive technologies is highly rational. From the perspective of a Chief Financial Officer allocating scarce capital, investing in a disruptive project requires diverting funds away from known, high-margin revenue streams toward unproven, low-margin ventures that actively threaten to cannibalize the core business 8. In these situations, the new business unit may look entirely unattractive compared with the core operations, featuring lower gross margins, smaller deal sizes, and weaker near-term returns 8.

When entrants attack the low end of a market, incumbents naturally choose flight rather than fight. Shedding low-margin, price-sensitive customers immediately improves the incumbent's aggregate profitability, making the initial stages of disruption look like a financial victory for the established firm 1. For example, when steel minimills entered the market by producing low-quality concrete reinforcing bars, integrated steel mills gladly ceded the low-margin business to focus on highly profitable sheet steel 48. It is only when the entrant's capabilities compound and penetrate the high-margin core that the devastating outcome of this highly rational retreat becomes apparent 38. The tragedy of the innovator's dilemma is that every step toward obsolescence appears entirely logical to the incumbent's management team at the time the decisions are made 18.

Internal Mechanisms Driving Underinvestment

While asymmetric motivation describes the macro-level strategic misalignment, the actual failure to invest is operationalized through specific internal mechanisms within the firm. These mechanisms - spanning resource dependence, sales force incentives, and research and development scaling constraints - function as institutional immune systems that systematically starve disruptive initiatives of capital and executive attention.

Resource Dependence and Customer Allocation

Resource Dependence Theory argues that organizations are inextricably bound by the external entities that provide their essential resources, primarily their largest customers and their institutional investors 478. According to this framework, a firm's freedom to pursue radical, paradigm-shifting innovations is highly constrained because dominant resource providers dictate the firm's strategic priorities. Large, premium customers demand sustaining improvements to the products they currently use; they rarely request disruptive, lower-performance alternatives 46.

Consequently, internal resource allocation processes are optimized to fulfill the requirements of the most important clients. An incumbent attempting to invest in a disruptive technology must consciously decide to allocate elite engineering talent and capital resources away from the customers generating the vast majority of current revenue. The inherent power imbalance between the firm and its key stakeholders acts as an internal constraint, enforcing a strict adherence to the status quo and exacerbating the asymmetric motivation to avoid disruptive markets 47.

Furthermore, internalization theory highlights how knowledge flows within multinational enterprises are concentrated to maximize returns on existing intellectual property rather than exploring highly uncertain new domains 910. The access to external knowledge can be achieved through internationalization and acquisitions, but incumbent management is primarily induced to invest resources in entrepreneurial activities that enhance their current monopoly-based rent 10. This behavior is further amplified in quasi-markets, where proprietary firms depend heavily on direct transfer payments or government contracts 8. The threat of losing scarce federal resources or failing to meet strict output floors ensures that these firms prioritize short-term efficiency over long-term technological pivots 8.

Sales Force Compensation Structures

A critical but frequently under-analyzed driver of asymmetric motivation is the structural design of sales force compensation. Personal selling represents the single largest marketing investment for business-to-business organizations, with corporations in the United States alone spending over eight hundred billion dollars annually on sales force compensation - an amount three times greater than their total advertising expenditures 17. These complex compensation frameworks rely heavily on performance-based variable pay, including strict commissions and quota-bonuses, which are explicitly designed to align the salesperson's day-to-day actions with the firm's immediate financial objectives 1112.

This precise financial alignment proves fatal when introducing disruptive technologies. Sales professionals operate rationally to maximize their personal income. Selling an established, high-priced sustaining product to an existing client requires significantly less effort and yields a high, predictable commission 17. In contrast, selling a disruptive product requires educating a new, unproven market, negotiating smaller deal sizes, and overcoming higher buyer skepticism - all for a substantially lower commission due to the disruptive product's inherently lower price point 1113.

Research assessing the allocation of sales effort reveals that representatives frequently misallocate their time. Rather than focusing on high-potential but difficult prospects, salespeople spend an excessive amount of time with existing customers with whom they have established rapport 17. Detailed surveys of time allocation indicate that reps spend significant portions of their day on administrative tasks and service calls, minimizing the time available to aggressively push unproven, disruptive solutions 21. Finance departments naturally try to ensure that these massive compensation plans have cost-control measures built into them, often offering flat commission rates that inadvertently penalize the sale of complex, lower-margin disruptive technologies 17.

The result is that even if the research and development department successfully develops a disruptive product, the sales organization will autonomously deprioritize it in favor of legacy offerings. Studies show that while high-performance work systems and empowerment climates can foster service-sales ambidexterity, the combination of behavior-based and outcome-based control systems typically funnels effort back into the most lucrative, sustaining channels 1114. A strategic tiering of incentives - integrating both extrinsic monetary rewards and intrinsic motivators like challenge-seeking - is necessary to overcome this internal resistance, but such hybrid structures are rarely implemented effectively by legacy incumbents 1113.

Research and Development Scaling Constraints

Research and development efficiency serves as another primary vector of asymmetric motivation. The average software company allocates roughly twenty percent of its total revenue to research and development, with some aggressive firms exceeding forty percent 1524. However, the common assumption that massive research budgets guarantee protection against disruption is structurally flawed. Research and development output does not scale linearly with organizational size or total expenditure.

Analyses of the Research and Development Index - a precise metric comparing one-year revenue growth against the percentage of revenue allotted to research - demonstrate that smaller software companies drastically outperform their larger competitors in returns from these investments 15. In a study analyzing nearly two hundred global software companies, firms generating under two hundred and fifty million dollars in revenue exhibited median index scores as high as 1.6, heavily boosted by rapidly compounding growth rates 15. Conversely, as companies matured and surpassed two billion dollars in revenue, their index scores tended to decline precipitously to median values of 0.6 15.

This steep decline in research efficiency occurs because large incumbents accumulate significant technology debt over time. As a software product matures, an ever-increasing proportion of the research budget must be diverted toward maintaining the existing architecture, addressing hyper-specific customer feature requests, and optimizing legacy codebases 1617. Incumbents face a constant internal resource war: funding a radical, disruptive new architecture requires pulling elite engineers away from the primary cash-cow product 1527. Consequently, the incumbent's massive research budget is effectively locked into a sustaining trajectory, leaving them structurally inflexible and highly vulnerable to agile entrants who possess zero legacy technical debt and can allocate their entire engineering capacity toward future innovation 117. Furthermore, when growth is primarily achieved through acquiring other companies, the research index tends to drop even further due to the high costs of integrating disparate technological platforms 1517.

Industry Dynamics and Incumbent Responses

The theoretical principles of asymmetric motivation are playing out with severe financial consequences across multiple modern sectors. Observing these dynamics in the automotive, financial, and artificial intelligence markets reveals how disruptive patterns adapt to different regulatory environments and capital constraints.

The Automotive Sector and Electric Mobility

The global transition from internal combustion engine vehicles to battery electric vehicles demonstrates how extreme capital intensity and physical supply chain rigidity exacerbate the innovator's dilemma. Legacy automakers - including industry giants like Ford, General Motors, Volkswagen, and Honda - possess highly optimized processes, supply chains, and labor forces dedicated to manufacturing complex mechanical drivetrains 11819.

The shift to electric mobility fundamentally alters the automotive value chain, moving the basis of competition away from mechanical horsepower toward computational power, software ecosystems, and advanced battery chemistry 19. For decades, legacy automakers viewed electric vehicles as low-margin compliance vehicles designed merely to satisfy environmental regulations. This view represented a highly unappealing economic prospect compared to the immense, reliable profitability of their internal combustion trucks and sport utility vehicles 1830. This classic asymmetric motivation allowed pure-play electric vehicle manufacturers to build critical momentum entirely unchallenged during the early stages of the market's development 1820.

| Automotive Strategy Dimension | Internal Combustion Incumbents | Electric Vehicle Disruptors |

|---|---|---|

| Core Revenue Engine | High-margin trucks and combustion SUVs | Software margins, batteries, and artificial intelligence |

| Manufacturing Constraint | Sunk costs in legacy assembly plants and union structures | Agile, purpose-built electric vehicle manufacturing facilities |

| Supply Chain Dynamics | High reliance on disparate Tier-1 external suppliers | Deep vertical integration and in-house component production |

| Distribution Model | Rigid franchise dealership networks with regulatory friction | Direct-to-consumer digital sales and continuous updates |

| Pace of Transition | Gradual hybridization designed to protect current profits | Aggressive global scaling, vertical integration, and rapid iteration |

The ascent of BYD in China and the broader global market is particularly instructive regarding the power of disruptive entry. Starting primarily as a battery manufacturer, BYD aggressively vertically integrated its supply chain. By producing its own semiconductors, power electronics, and proprietary battery technologies in-house, BYD eliminated its reliance on external suppliers 2122. This deep integration drastically reduced production delays and allowed for aggressive cost leadership that legacy automakers simply could not match without incurring massive financial losses 2122. Between 2017 and 2024, BYD scaled its production from five hundred thousand to over four million vehicles - an extraordinary seven hundred percent increase - driving its revenue to one hundred and seven billion dollars 21. By 2023, BYD surpassed Volkswagen to become the best-selling automobile brand in China, stripping VW of a title it had held since the Chinese automotive sector first opened to foreign investment 2234.

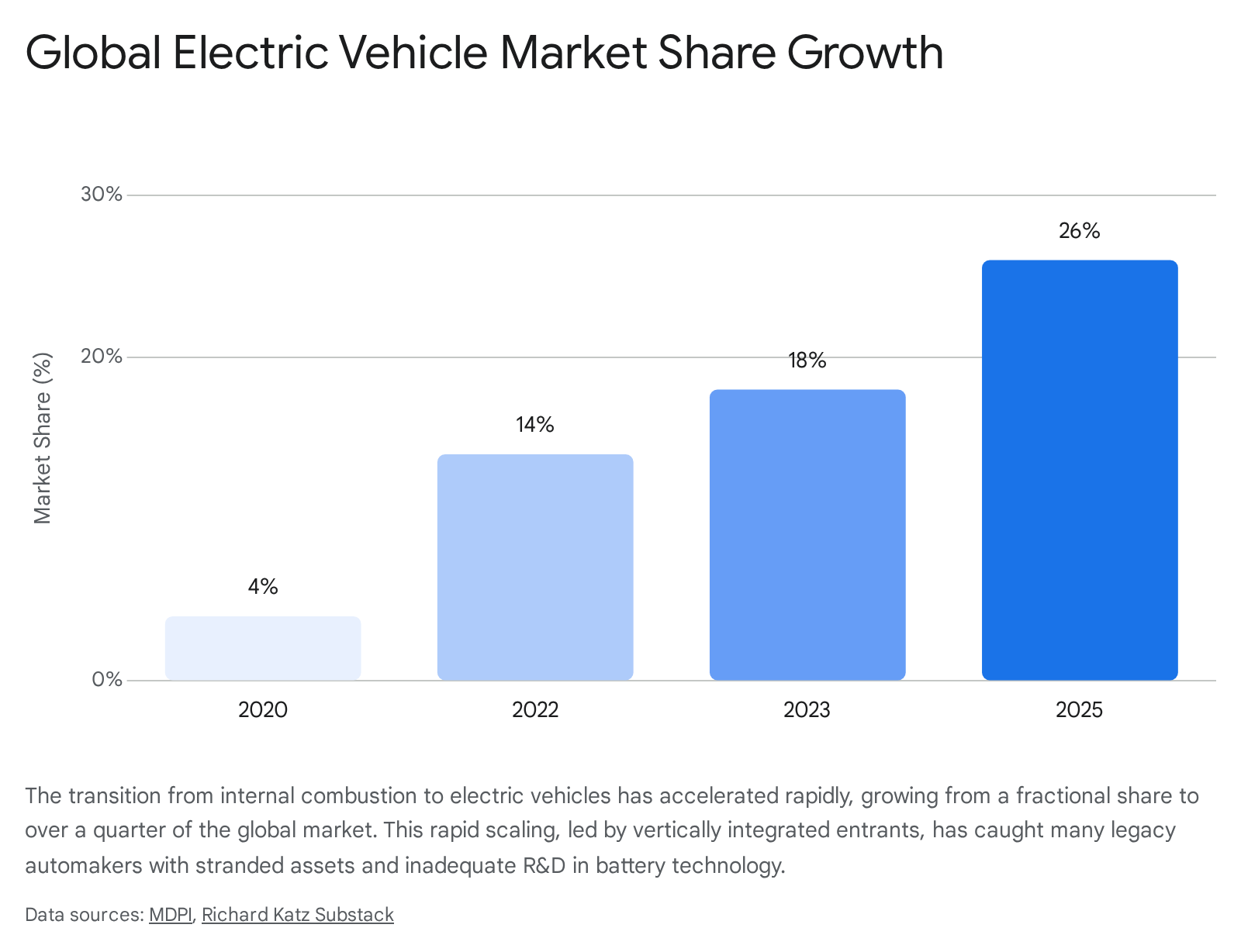

The financial toll of a delayed response driven by asymmetric motivation has been staggering for incumbents. Globally, electric vehicles grew from representing four percent of total auto sales in 2021 to an estimated twenty-six percent by 2025, surpassing the ten percent tipping point in thirty-nine different countries 30.

Burdened by outdated manufacturing techniques and declining internal combustion demand in critical markets, leading legacy automakers recently announced combined losses and factory write-offs exceeding one hundred and eighteen billion dollars tied to their struggling electric vehicle transitions 1830. Specifically, Honda absorbed sixteen billion dollars in write-offs, Stellantis lost twenty-six billion, and Ford lost nineteen billion dollars 30. In mid-2024, Ford disclosed a staggering thirty-six thousand dollar loss on every electric F-150 Lightning pickup it sold, underscoring the severe economic friction of dragging a legacy business model into a radically new technological paradigm 18. Rather than chasing the aggressive volume scaling of entrants, legacy firms have been forced into a defensive posture, relying on hybrid vehicles to fund their gradual transition 19.

Financial Services and Digital Banking

The global banking sector presents a textbook case study of both new-market and low-end disruption. Historically, traditional financial institutions focused their sustaining innovations on their most profitable corporate clients and high-net-worth individuals, offering complex wealth management platforms and highly tailored commercial lending products 2336. Conversely, the lower mass market and younger demographics were subjected to outdated legacy systems, high banking fees, predatory overdraft charges, and extreme interest rates 3637.

Nowhere is this dynamic clearer than in the Brazilian banking market. Prior to 2013, the financial system was completely dominated by an oligopoly of five legacy institutions - including Banco do Brasil and Itaú Unibanco - that controlled the overwhelming majority of the nation's banking assets 3724. This incumbent system systematically excluded millions of working-class Brazilians who had thin or non-existent formal credit files. Those fortunate enough to be banked faced annual credit card interest rates routinely exceeding three hundred percent, reflecting both the risk of lending in a market with weak infrastructure and a total lack of meaningful competition 37. Because serving low-income individuals with thin credit profiles represented a high-risk, low-margin proposition that did not fit into legacy risk-assessment models, the incumbents aggressively ignored them 37.

Nubank capitalized entirely on this asymmetric motivation. Operating strictly as a digital neobank with zero physical branches, Nubank drastically reduced its operational cost structure. The company utilized alternative data sources, machine learning, and advanced data science to build proprietary credit models capable of profitably underwriting the previously unbanked populations that legacy banks refused to serve 37. Because Nubank's customer acquisition and operating costs were a mere fraction of the incumbents', it could disrupt the market by offering zero-fee credit cards and high-yield digital accounts managed entirely through a smartphone application 25.

Incumbents predictably viewed Nubank's initial low-income customer base as fundamentally unprofitable and retreated further upmarket rather than competing on fees. However, by leveraging this low-end foothold, Nubank rapidly improved its offerings and steadily migrated into highly profitable segments. By 2024, Nubank allowed borrowers to transfer their highly lucrative payroll loans from traditional banks at an interest rate of 1.40 percent per month, significantly undercutting incumbents and forcing them to either reduce their own margins or hemorrhage customers 40. Furthermore, by leveraging small and medium-sized business deposits as collateral, Nubank began decoupling creditworthiness from traditional scoring, successfully entering the highly lucrative commercial banking segment 40. By late 2024, Nubank reached the milestone of one hundred million customers, achieving a twenty percent total market share in Brazil and officially dethroning Banco do Brasil - an institution founded in 1808 - as the top primary bank provider in the country 24. Across the global fintech landscape, established scaled fintechs generating over five hundred million dollars in annual revenue now account for roughly sixty percent of the global fintech industry's total revenue, signaling a permanent structural shift away from legacy banking architectures 26.

Generative Artificial Intelligence and Enterprise Software

The rapid emergence of Generative Artificial Intelligence introduces a complex nuance to the standard disruption theory. While initial analysis might classify generative AI as a classic disruptive threat to enterprise software incumbents, current market data suggests it may actually function as a powerful sustaining innovation for established technology giants 836.

Generative AI requires massive complementary assets to function effectively in an enterprise context - specifically, massive proprietary data sets and deeply embedded workflow distribution networks 27. Incumbents like Microsoft, Salesforce, and established financial platforms possess both the distribution channels and the idiosyncratic proprietary databases needed to maximize the utility of these new models 827. Rather than fleeing from the technology, these incumbents are heavily incentivized to bundle AI capabilities directly into their core platforms, aggressively defending their market share and increasing the average revenue per user 8. This dynamic is reflected in rapid adoption rates; generative AI has achieved a 39.5 percent adoption rate across businesses in just two years, vastly outpacing the historical adoption curves of the internet and personal computers 43. According to recent data, seventy-four percent of organizations report that investments in generative AI have met or exceeded expectations, and companies with fully modernized AI processes are achieving 2.5 times higher revenue growth than their peers 28.

However, a secondary mechanism of asymmetric motivation is emerging around human capital and the psychological impact of AI adoption. As organizations integrate generative AI to automate cognitive tasks, immediate productivity and task quality improve significantly 4529. Seventy-five percent of surveyed executives expect these tools to increase productivity across roles by 2027 45. Yet, academic research reveals a concerning psychological deprivation effect. In a large-scale study involving thousands of participants, researchers found that when employees switched from AI-assisted work back to independent, human-solo tasks, their intrinsic motivation dropped by an average of eleven percent, and feelings of boredom spiked by twenty percent 2947.

This psychological asymmetry presents a subtle but severe organizational risk. Because AI reduces the cognitive challenge that typically makes professional work fulfilling - such as critical thinking, complex problem solving, and creative synthesis - heavy reliance on these tools threatens to erode deep engagement 47. Companies must therefore balance the immediate operational productivity of AI tools with the long-term risk of eroding the foundational critical thinking skills necessary for future organizational innovation, particularly as younger cohorts enter the workforce heavily dependent on automated assistance 47. To succeed, business leaders must transition from treating AI as a novelty to ensuring deep, outcome-aligned utilization across the workforce 43.

Evolving Academic Critiques and Boundary Conditions

While the concept of asymmetric motivation remains highly influential in strategic management, recent academic discourse cautions against treating the incumbent's curse as an inescapable, deterministic absolute 3031. Detailed historical analyses of technological transitions indicate that the failure of established firms is heavily context-dependent and heavily moderated by the nature of the industry's underlying architecture.

The Moderating Role of Complementary Assets

Scholars emphasize that the success of a disruptive attack is highly dependent on whether the new technology requires access to specialized complementary assets that the incumbent currently controls 2730. In industries characterized by heavy regulation, massive capital requirements, or the need for specialized manufacturing equipment, the incumbent's likelihood of survival dramatically increases 3031. In these scenarios, the disruptive entrant must eventually partner with, or be acquired by, the incumbent to reach scale. This structural dependency effectively converts a disruptive threat into a sustaining enhancement for the legacy firm 2730.

Furthermore, empirical reviews of historical innovations - including a comprehensive analysis of over one hundred qualitative studies - show that incumbents are not universally paralyzed by discontinuous shifts 3031. Firms can successfully execute branching strategies, which involve deliberate expansion into new sectors while aggressively reconfiguring their core competencies. For example, during the catastrophic collapse of the photographic film market, Fujifilm successfully leveraged its deep chemical engineering expertise to pivot into highly profitable domains like cosmetics and pharmaceuticals, effectively avoiding the innovator's dilemma through rapid lateral movement 30. Market-driven innovations, as opposed to purely technological disruptions, sometimes allow incumbents to respond effectively without completely restructuring their organizational hierarchies 32.

Organizational Ambidexterity and Strategic Acquisition

To survive the pressures of asymmetric motivation, contemporary strategy literature highly recommends the pursuit of organizational ambidexterity - the ability to simultaneously exploit existing, profitable markets while fiercely exploring highly uncertain new ones. However, execution remains exceptionally difficult. The standard operational recommendation is to establish a completely independent business unit to pursue the disruptive opportunity, physically and financially insulating it from the parent company's strict margin requirements, legacy sales compensation plans, and rigid resource dependence constraints 3632.

Alternatively, incumbents frequently attempt to purchase disruption through mergers and acquisitions. While buying an agile entrant eliminates the immediate competitive threat, it rarely solves the internal capability gap. Post-acquisition, incumbents frequently force the disruptive startup to assimilate into the legacy corporate culture, subjecting the newly acquired subsidiary to the exact same asymmetric resource constraints that stifled internal innovation in the first place 317. If the incumbent does not actively preserve the acquired firm's autonomy and aggressively fund its research and development - even when that new technology threatens to cannibalize core sales - the acquired disruption quickly stagnates, destroying the value of the acquisition 17. Furthermore, utilizing corporate slack (surplus resources) to fund exploration only succeeds if the firm is willing to tolerate negative performance relative to its historical aspirations for a sustained period 33.

Ultimately, asymmetric motivation proves that disruptive vulnerability is rarely a symptom of ignorance, complacency, or poor management. It is the highly predictable outcome of rational organizations executing flawlessly against the financial metrics of their present reality. By perfectly optimizing their operations to serve their most demanding customers, incumbents inadvertently leave themselves strategically blind to the economics of the future, paving the way for entrants to fundamentally redefine the market.