The arena concept in competitive strategy analysis

Introduction: The Erosion of Sustainable Competitive Advantage

For over four decades, corporate strategy, executive decision-making, and academic literature within the strategic management discipline have been dominated by a singular, overarching premise: the primary objective of a firm is to achieve and defend a sustainable competitive advantage. This paradigm was formally codified in the late 1970s and 1980s, most notably when Harvard Business School Professor Michael E. Porter introduced the "Five Forces" framework in his seminal Harvard Business Review article and subsequent book, Competitive Strategy 121. Porter's macroeconomic-inspired model provided a rigid, structuralist view of competition, asserting that profitability was largely determined by the intensity of rivalry, the threat of substitutes, the bargaining power of buyers and suppliers, and the barriers to new entrants 123. In this traditional framework, strategy was an exercise in positioning a firm defensively within its specific industry - often defined by Standard Industrial Classification (SIC) codes - to extract maximum economic rents over prolonged, stable periods.

However, the acceleration of globalization, the digital revolution, the dematerialization of value, and the advent of platform economics have rendered the structural boundaries of traditional industries increasingly porous. Empirical observations of modern market dynamics suggest that sustainable competitive advantages are no longer the norm; rather, they have become the rare exception, applicable only to a dwindling number of highly regulated or capital-intensive monopolies 475. Leading scholars, most notably Rita Gunther McGrath of Columbia Business School, argue that strategic management must pivot toward the orchestrating of "transient advantages" 467. In her research, including The End of Competitive Advantage, McGrath posits that deeply ingrained organizational systems designed to extract maximum value from a prolonged advantage have become fatal liabilities in a high-velocity environment 812.

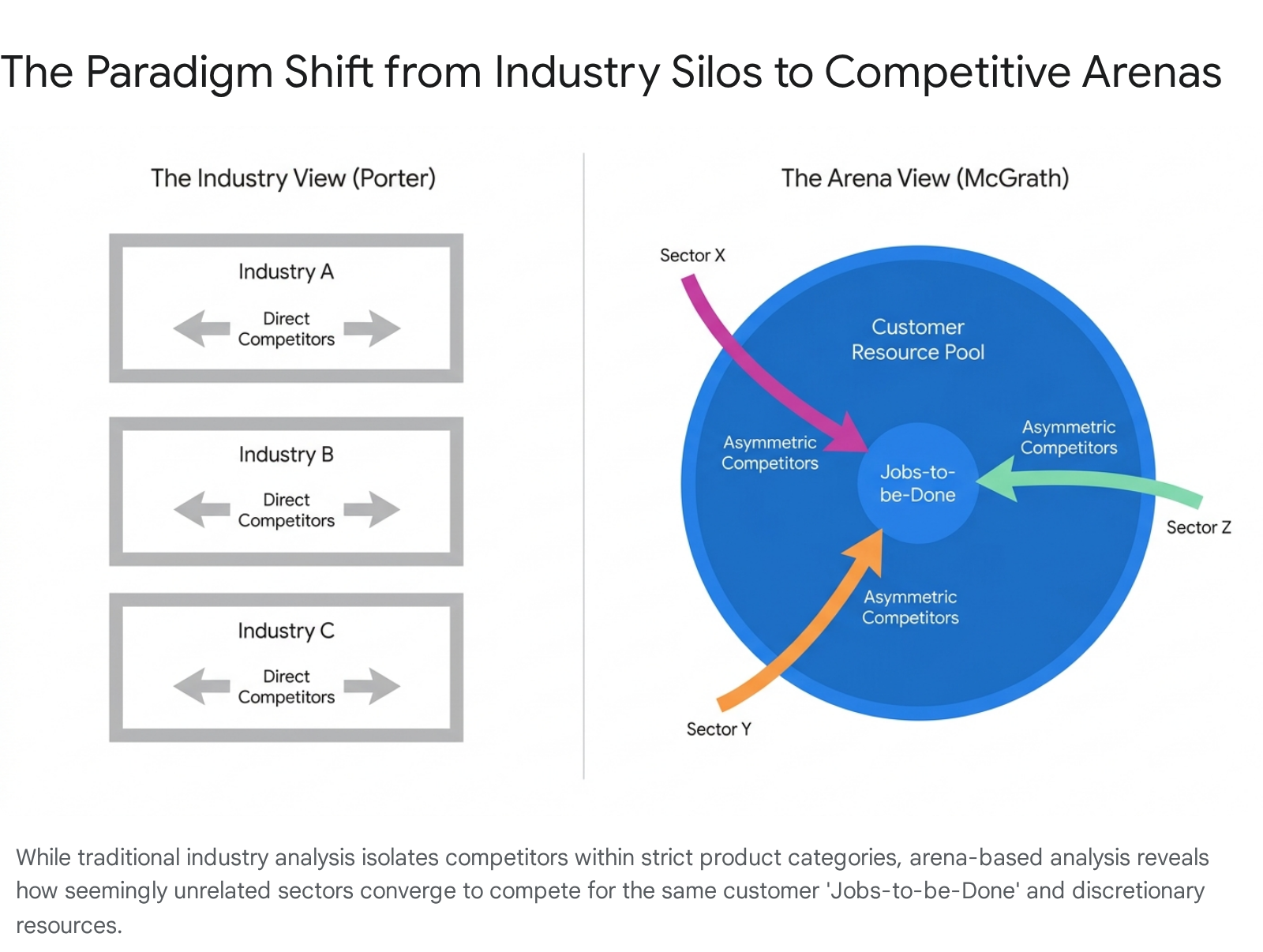

The transition from a stable industrial economy to a fluid, digital economy requires an epistemological shift in how competitive landscapes are defined. The foundational unit of analysis must shift from the "industry" - a supply-side definition grouping firms that produce similar products or services - to the "arena," a demand-side construct encompassing any entity competing for the same pool of resources or seeking to fulfill the same fundamental customer requirement 713149.

This comprehensive report investigates the theoretical foundations of the competitive arena concept, compares it against adjacent frameworks such as business ecosystems and blue ocean strategy, examines its operationalization through Discovery-Driven Planning, and evaluates the profound implications of post-2020 artificial intelligence (AI) disruptions on strategic inflection points.

Deconstructing the "Arena" Framework

The concept of the competitive arena fundamentally redefines who a firm's true competitors are and dictates where value migration is likely to occur. Traditional industry analysis creates analytical blind spots because it inherently assumes that a firm is primarily comparing itself to other organizations with similar supply chains and operational models 59. For instance, a traditional industry view assumes airlines compete with airlines, and retail banks compete with retail banks. Conversely, an arena is characterized by the intersection of a customer segment, a specific offering, and the geographic or digital space where that offering is delivered 710. It is defined by the connection between customers and solutions, rather than the conventional description of offerings as near-substitutes for one another 11.

The Core Components of an Arena Map

Mapping a competitive arena requires a fundamental departure from traditional market share analysis and product categorization. According to McGrath's frameworks, an arena map must identify the underlying mechanics of customer behavior and resource allocation. This mapping process forces strategic analysts to look beyond their immediate peers and recognize asymmetrical threats. The structural model for mapping an arena is composed of several interdependent elements that define the boundaries of competition.

| Arena Element | Conceptual Definition | Strategic Implication |

|---|---|---|

| Contested Resource Pool | The finite resources stakeholders possess, whether that resource is financial capital, disposable time, or cognitive attention. | Shifts focus from winning "market share" to capturing a share of a specific resource pool, revealing asymmetrical competitors. |

| Jobs-to-be-Done (JTBD) | The underlying task, problem, or goal a customer is attempting to resolve in a specific situation. | Prevents firms from defining themselves by their products, highlighting that customers "hire" solutions regardless of the provider's industry origin. |

| Contestants | Traditional rivals, asymmetric attackers, startups, and cross-sector incumbents possessing capabilities to address the JTBD. | Broadens competitive intelligence to track technology firms, platform aggregators, and adjacent market leaders entering the space. |

| Consumption Chains | The end-to-end lifecycle of how a job is executed, from initial awareness and selection to payment, delivery, and disposal. | Identifies friction points where agile competitors can insert themselves to disintermediate incumbents from the end customer. |

| Valued Attributes | The positive, negative, or neutral experiences and characteristics stakeholders associate with the current solutions. | Highlights areas where incumbent offerings are over-serving or under-serving the market, creating entry points for disruption. |

To illustrate the critical importance of identifying the correct contested resource pool, one must look at the apparel industry in the early 2000s. Retailers historically misidentified their competitive arena by focusing exclusively on other clothing brands and department stores 18. The actual arena was "American teen discretionary spending," which in 2007 was estimated at $80 billion 18. The most devastating competitors to apparel brands during this period were not other fashion labels, but mobile phone manufacturers and telecommunications providers. Devices and data plans successfully captured that specific financial resource pool, leaving apparel retailers blindsided because they were looking at the wrong competitive set 18. Similarly, in the energy sector, traditional oil and gas incumbents are increasingly finding themselves in a shifting arena where their competitors for capital and mobility solutions are technology firms like Tesla and Apple, rather than just other fossil fuel extraction companies 19.

Transient Advantage and Continuous Reconfiguration

The logical conclusion of competing in arenas rather than structurally defined industries is that competitive advantages are inherently fleeting. As a result, the mandate of corporate strategy shifts from erecting defensive moats to mastering the capability of "continuous reconfiguration" 6812. Organizations can no longer afford to spend months crafting a single, rigid, long-term strategic plan; they must instead curate a portfolio of multiple transient advantages that can be rapidly built, exploited, and abandoned 45.

The lifecycle of a transient advantage consists of distinct, rapidly accelerating phases. It begins with the innovation and launch phase, where resources are allocated to explore a new arena. This is followed by a ramp-up period where the firm scales the offering, leading to a period of intense exploitation where profits and market share are captured 57. However, unlike the traditional model where this exploitation phase lasts decades, the transient advantage model recognizes that success immediately spawns intense, asymmetrical competition, weakening the advantage 5. The firm must then enter a reconfiguration phase to keep the advantage fresh, or, crucially, an organized disengagement phase 5711.

Firms that operate under the outdated illusion of sustainable advantage typically hold on to declining business models far too long. They engage in fierce defense of the status quo, hoarding assets and building bureaucracies that inhibit risk-taking and iterative learning, ultimately leading to catastrophic value destruction when the market inevitably shifts 512. The demise of companies like Kodak or Nokia illustrates the danger of remaining anchored to a core competence when the arena itself has fundamentally changed 14112021. Conversely, organizations built for the transient advantage economy institutionalize healthy disengagement. They possess the organizational "deftness" to reallocate capital and talent rapidly away from fading arenas and into emerging ones long before a crisis forces their hand 68. In McGrath's longitudinal study of global growth outliers - companies that achieved consistent year-over-year profit growth for over a decade, such as HDFC Bank, Cognizant, and Infosys - a common denominator was their relentless pursuit of new arenas and their unsentimental willingness to dismantle existing advantages 61211.

Theoretical Adjacencies: Arenas, Ecosystems, and Blue Oceans

As the concept of the rigid industry boundaries erodes within academic literature, several parallel theoretical frameworks have emerged to describe modern, interconnected competitive dynamics. While frequently used interchangeably in superficial managerial discourse, the terms "Arenas," "Business Ecosystems," and "Blue Oceans" describe highly distinct strategic phenomena. Delineating their precise boundaries is critical for rigorous strategic analysis and the application of appropriate management practices.

Business Ecosystems: Symbiosis and Network Orchestration

Originating from biological metaphors introduced by James Moore in a 1993 Harvard Business Review article, a business ecosystem emphasizes the co-evolution of capabilities around a new innovation or platform 221224. Unlike an arena, which is inherently a theater of competition for a finite resource pool, an ecosystem is a community of interdependent organizations - encompassing suppliers, distributors, complementors, regulatory institutions, and customers - that interact to support a focal value proposition 2213142728.

Ecosystem theory, particularly as advanced by scholars in the Strategic Management Journal and MIT Sloan Management Review, focuses heavily on network externalities, architectural control, and the alignment of diverse actors 222829. In a business ecosystem, participants must delicately balance competition with cooperation (co-opetition) to ensure the viability and growth of the entire system 121330. If the competitive arena is understood as the overarching battlefield where disparate actors fight to fulfill a customer's job-to-be-done, the ecosystem is the complex supply chain, alliance network, and technological platform required to successfully field an offering in that specific battle. For example, technology giants like Apple and Samsung compete fiercely within the consumer electronics arena, yet they exist symbiotically within a broader global business ecosystem, with Samsung manufacturing critical components essential for Apple's hardware delivery 31.

Blue Ocean Strategy: Escaping Competition via Value Innovation

Developed by W. Chan Kim and Renée Mauborgne, Blue Ocean Strategy focuses on creating uncontested market space, theoretically making the competition irrelevant through a process of simultaneous differentiation and cost reduction, termed "value innovation" 3233. While both the Arena perspective and Blue Ocean Strategy agree that adhering strictly to traditional industry boundaries is a recipe for stagnation, their prescriptive models diverge significantly regarding the nature of competitive longevity.

Blue Ocean strategy is primarily a front-end innovation framework aimed at escaping competition by identifying white spaces located between existing substitute industries 32. The Arena perspective, conversely, embraces a more turbulent reality, acknowledging that even the most pristine, entirely new "Blue Oceans" will rapidly turn "Red" due to the low barriers to entry and the transient nature of modern technological advantages. Therefore, while successfully navigating into a Blue Ocean is a highly valid and lucrative tactic during the innovation and launch phase of the transient advantage lifecycle, Arena strategy explicitly dictates that firms must immediately prepare for the inevitable and swift commoditization of that newly discovered space 59.

Comparative Taxonomy of Strategic Frameworks

To synthesize these concepts, the distinctions between these macroeconomic and managerial frameworks can be categorized by their core unit of analysis, their primary strategic objective, and their underlying assumptions regarding the duration of competitive advantage.

| Strategic Framework | Primary Unit of Analysis | Core Strategic Objective | View of Advantage Duration | Leading Academic Proponents |

|---|---|---|---|---|

| Five Forces (Industry) | Structural industry boundaries (e.g., SIC codes) | Defendable market positioning; sustained economic rent extraction. | Long-term; sustainable via high structural barriers to entry. | Michael Porter |

| Blue Ocean Strategy | Uncontested market space | Value innovation; rendering existing competition irrelevant. | Medium-term; sustainable until inevitable imitators arrive. | W. Chan Kim & Renée Mauborgne |

| Business Ecosystems | Interdependent networks, platforms, and complementors | Orchestration; mutual co-evolution; aligning stakeholder incentives. | Continuous evolution through mutual symbiosis and network effects. | James Moore, Michael Jacobides |

| Competitive Arenas | Customer Jobs-to-be-Done & Contested Resource Pools | Continuous reconfiguration; rapid exploitation followed by disengagement. | Transient; advantages are short-lived and rapidly rotate. | Rita Gunther McGrath |

Competing Views: The Enduring Defense of Porter's Five Forces

Despite the compelling logic of the transient advantage economy and the widespread adoption of ecosystem thinking, it would be academically negligent to declare traditional industry analysis entirely obsolete. Michael Porter's Five Forces model, which he forcefully reaffirmed and updated in a landmark 2008 Harvard Business Review article, remains a foundational analytical tool for corporate strategy, particularly when applied within specific macroeconomic and physical contexts 1223.

The Persistence of Structural and Capital Barriers

Critics of the universal application of the "transient advantage" hypothesis argue that the absolute necessity of continuous, rapid reconfiguration is largely confined to hyper-competitive, deeply digitized sectors such as consumer electronics, enterprise software, media, and telecommunications 3415. In industries characterized by immense capital intensity, complex physical infrastructure requirements, and heavy regulatory oversight - such as aerospace manufacturing, basic materials, utility power distribution, and large-scale resource extraction - competitive advantages prove to be remarkably durable over decades 22415.

In these heavy industry sectors, the Five Forces framework remains highly predictive of structural profitability. The threat of new entrants in the advanced semiconductor fabrication industry or the commercial wide-body airliner market is virtually non-existent due to multi-billion-dollar fixed capital requirements, specialized supplier networks, and incredibly steep learning curves 216. Therefore, companies like Boeing and Airbus, or TSMC and ASML, operate in environments where defending a core competitive advantage through traditional structural barriers, supply chain dominance, and scale remains a highly rational, necessary, and lucrative strategy. For these firms, abandoning long-term strategic planning in favor of purely transient agility could be disastrous.

The Heuristic Value of Clear Industry Definition

Furthermore, operationalizing the broad arena concept poses significant practical difficulties for mid-level management and execution teams. Defining a competitive arena purely by abstract "jobs-to-be-done" can lead to conceptual boundarylessness, where a firm views entirely disparate macro-trends as immediate competitive threats, potentially leading to strategic paralysis, dilution of brand identity, or a severe lack of focus 1517. As Porter notes, drawing industry boundaries correctly and narrowly clarifies the immediate, proximate causes of profitability and dictates tactical resource allocation on a day-to-day basis 1.

While McGrath is undoubtedly correct that long-term existential threats usually emerge from asymmetric arenas outside the traditional industry, short-to-medium-term profitability and operational survival are still heavily dictated by direct, head-to-head rivalry 12216. A company cannot effectively plan next quarter's pricing strategy or supply chain logistics based solely on abstract arena dynamics. Thus, while the arena concept is vital for executive leadership, long-range innovation portfolios, and strategic foresight, traditional industry analysis remains indispensable for near-term operational optimization, tactical pricing, and margin defense 2217.

Strategic Inflection Points and "Seeing Around Corners"

A central pillar of successfully competing in fluid arenas is the organizational ability to anticipate structural market shifts before they obliterate existing, profitable business models. In her 2019 publication Seeing Around Corners, McGrath codifies the anatomy of a "strategic inflection point" - a concept initially popularized by former Intel CEO Andrew Grove - as an environmental shift that creates a 10x change in what is technologically or economically possible, fundamentally altering the constraints and rules of a competitive arena 381840.

Navigating Complexity by Leading Indicators

Inflection points do not occur randomly or overnight; they are the culmination of a slow burn, a process that builds subtly over time through technological advancements, regulatory shifts, or changing consumer behaviors 134041. The failure of incumbent firms to navigate these shifts is rarely a failure of intelligence; it is an epistemological failure regarding the specific metrics they choose to monitor and prioritize 4243.

Management systems and corporate boards are overwhelmingly biased toward the monitoring of lagging indicators. Lagging indicators, such as EBITDA, return on net assets, or historical revenue growth, reflect the financial outcomes of past decisions and are virtually useless for predicting future disruptions 134243. Current indicators, such as operating cash flows or real-time inventory levels, describe the present operational state but offer little forward-looking foresight 1343.

To effectively "see around corners," organizations must systematically develop, track, and empower decisions based on leading indicators 13184243. These metrics are often qualitative, highly emergent, and based on weak signals detected at the periphery of the firm's awareness 1343. Leading indicators transform abstract hypotheses about the future into observable empirical data, signaling when a foundational assumption underlying the current business model is beginning to fracture 43. McGrath emphasizes an inverse relationship between signal strength and strategic degrees of freedom: by the time a disruptive signal is clear enough to be captured unequivocally in lagging financial indicators, the inflection point has already occurred, and it is generally too late for the incumbent to mount an effective, non-reactionary response 131843.

Post-2020 Disruptions: AI and the Transformation of Professional Services

The rapid integration and scaling of advanced Artificial Intelligence (AI) and Generative AI (GenAI) systems post-2020 represents a textbook strategic inflection point, creating massive 10x shifts across multiple global arenas 133819. While the impact of AI is ubiquitous, its disruptive force is perhaps most profoundly felt in knowledge-based sectors, specifically within the professional services, consulting, and legal arenas.

Historically, the dominant business model of elite law firms, management consultancies, and financial advisory practices was rigidly anchored to the "billable hour" 4520. Within this paradigm, time served as an accepted proxy for value, effectively transferring the economic risk of uncertainty, complexity, and inefficiency directly onto the client 20. However, as AI systems continuously demonstrate the capability to execute complex cognitive tasks at scale - such as drafting a 95% complete IPO prospectus in minutes or reviewing tens of thousands of corporate contracts instantaneously - the historical linkage between time spent by a human professional and value delivered to the client has ruptured irreparably 4520.

As McGrath observed in analyses regarding the future of work in 2025 and 2026, AI renders time an increasingly meaningless measure of value in these arenas 4120. The legal and consulting arenas are experiencing an accelerated, structural erosion of the billable hour, transitioning forcefully toward value-based pricing (VBP) models 2047. Firms that fail to recognize the death of the billable hour as a critical leading indicator will continue to optimize their operations for human hour accumulation, inadvertently punishing their own profitability when adopting efficiency-enhancing AI 20. Conversely, forward-thinking organizations recognize that AI will not replace high-level strategic thinking, but will augment human sense-making. By blending human imagination and strategic context with AI's massive data-crunching capabilities, these firms are aggressively mapping new arenas and anticipating future inflection points, thereby securing a transient advantage in the newly redefined professional services landscape 3821.

Operationalizing the Arena: Discovery-Driven Planning

Recognizing a transient advantage, identifying a shifting arena, or spotting an inflection point is insufficient for corporate survival; organizations must possess the internal structural models and processes to safely operationalize this knowledge. Traditional strategic planning methodologies, which rely on extrapolating historical data into precise, long-term financial forecasts (such as Net Present Value or discounted cash flow analysis), are wholly inadequate and often highly destructive when applied to highly uncertain, nascent arenas 44950. When launching initiatives into uncharted territories, assumptions vastly outnumber known facts, making precise financial forecasting an exercise in corporate fiction.

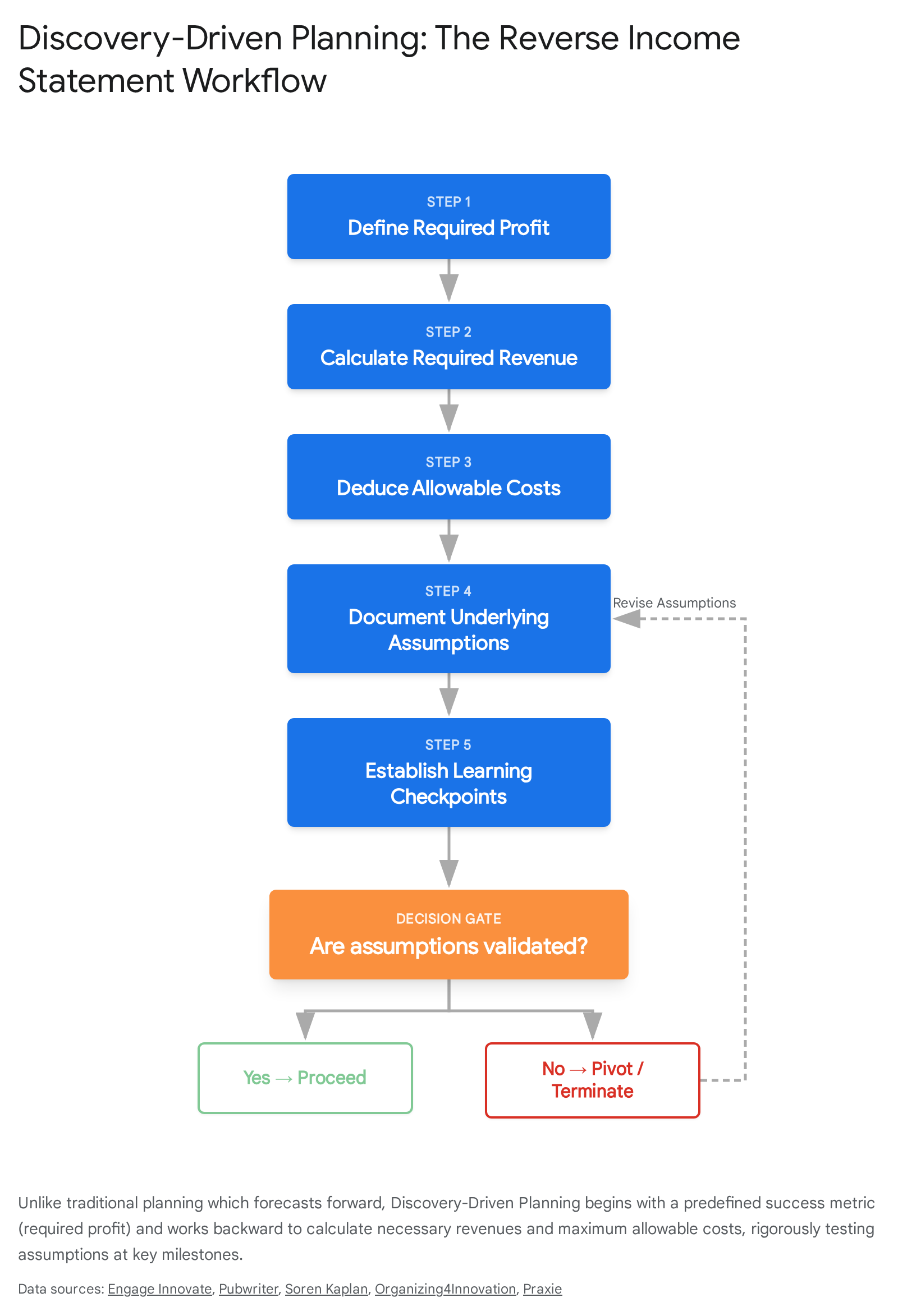

The Mechanics of the Reverse Income Statement

To mitigate the extreme risks associated with arena exploration, McGrath and Ian MacMillan developed "Discovery-Driven Planning" (DDP) 495051.

DDP is a disciplined, highly structured methodology that explicitly recognizes the high ratio of assumption-to-knowledge inherent in innovation, enforcing rigorous, low-cost testing before significant capital is committed 4950.

The DDP framework operates on a sequence of distinct, counter-intuitive steps that flip traditional planning on its head:

- Define Success via the Reverse Income Statement: Rather than blindly forecasting future market share and revenues to see what profit might eventually emerge, DDP begins with the required end state. Planners determine the mandatory profit margin required by the corporation to justify the venture's risk, and then calculate backward to deduce the maximum allowable costs and the required top-line revenues 49505152.

- Rigorous Market Benchmarking: The mathematically deduced metrics from the reverse income statement are strictly compared against empirical market realities. Planners must assess if the required pricing, adoption rates, and sales volumes are realistic compared to industry benchmarks, preventing delusional forecasting 5053.

- Specify Granular Operational Requirements: Every single activity, process, and partnership necessary to produce, sell, and deliver the solution is mapped out. This ensures that hidden structural costs - often overlooked in optimistic business plans - are explicitly exposed and accounted for in the allowable cost calculation 5053.

- Document and Prioritize Assumptions: This is the crux of the DDP method. Every variable in the reverse income statement that is not an empirically proven fact is logged as an assumption. These assumptions are then rigorously ranked by their potential to derail the entire project 505153.

- Set Checkpoints and Learning Milestones: In a DDP environment, project funding is not released based on the calendar or annual budget cycles, but solely upon the successful empirical validation of key assumptions at predefined milestones 505153. If an assumption proves false during a low-cost test, the project is rapidly pivoted, reconfigured, or cheaply terminated before massive capital is destroyed.

Implementation Difficulties: Organizational Silos and the General Ledger

While the theoretical underpinnings of arena strategy, transient advantage, and Discovery-Driven Planning are robust, their practical implementation within legacy organizations often encounters fatal friction 17. The primary antagonist of corporate agility and continuous reconfiguration is not external competition, but the traditional corporate structure itself, specifically the persistence of functional silos, localized KPIs, and command-and-control financial budgeting 5455565758.

The Paradox of Traditional Financial Discipline

Traditional financial discipline, enforced by rigid general ledgers and annual budgeting cycles, structurally incentivizes vertical, siloed thinking 55. Corporate managers are measured, evaluated, and compensated based on their ability to optimize their specific department's performance metrics (e.g., Sales quotas, Marketing lead generation, IT uptime) independently of the broader organizational goals 5458. However, the systemic "Jobs-to-be-Done" that define competition in an arena rarely fit neatly into a single functional silo; delivering true systemic value to a customer requires horizontal integration and frictionless data flow across the entire customer journey 545558.

When the logic of a transient advantage demands that capital and top talent be rapidly stripped from a historically profitable legacy product line and injected into an uncertain emerging arena, silo owners fiercely defend their turf. They view budget reductions as a loss of personal power, creating massive bureaucratic gridlock and hoarding critical information 5555758. The financial toll of these silos is staggering; across industries, poor-quality data caused by fragmented, siloed systems costs companies an estimated $3.1 trillion annually, while dramatically slowing decision speed 57.

Organizations frequently attempt to solve this vertical isolation through the implementation of matrixed leadership structures. However, research indicates that this often exacerbates complexity, leading to competing KPIs, an untenable number of incompatible projects being funded simultaneously across various silos, and a fundamental inability to aggressively allocate resources toward genuine innovation 545557.

Architecting the Integrated Operating Model

To successfully overcome these implementation gaps and operationalize an arena strategy, organizations must transition away from viewing innovation as a series of project-based, siloed continuous improvement initiatives 56. Instead, strategic agility must be embedded into a digitally integrated operating model 56. This structural evolution requires abandoning isolated, vertical KPIs in favor of horizontal, outcome-based metrics that track the complete consumption chain and measure true customer value creation 5558.

Furthermore, executive leadership must actively cultivate a "permissionless" culture. In this environment, initial exploration and experimentation are decoupled from massive, career-defining budget approvals. A culture optimized for transient advantage ensures that failure at an early DDP checkpoint is celebrated as cheap, valuable learning, rather than punished as a career-limiting mistake 54721.

Non-Western Case Studies in Arena Competition

The paradigm shift from rigid industry competition to fluid arena orchestration is perhaps most starkly visible in rapidly digitizing emerging markets. Freed from the heavy legacy infrastructure and deeply entrenched, century-old industry paradigms characteristic of Western economies, corporations in Asia and Africa have aggressively pursued arena-based strategies. These regions provide definitive case studies in the power of ecosystem orchestration, asymmetrical disruption, and transient advantage management.

India: Reliance Jio and the Digital Lifestyle Arena

The explosive entry of Reliance Jio into the Indian telecommunications sector in 2016 serves as a definitive masterclass in redefining a competitive arena to outmaneuver entrenched incumbents. Traditional telecom operators in India, such as Airtel, Vodafone, and Idea, viewed their industry through a highly conventional lens: they competed fiercely on voice tariffs, SMS bundles, and marginal improvements in 3G data costs within a saturated market 596061.

Reliance Jio, however, did not intend to compete within the confines of the traditional telecom industry; they correctly identified their target arena as the broader "digital enablement and lifestyle of the Indian consumer" 6162. Backed by the financial muscle of Reliance Industries and an unprecedented $32 billion capital investment in pan-India 4G LTE infrastructure, Jio launched with an aggressively predatory pricing model - offering free unlimited voice calls and drastically subsidized data plans 596062.

By doing so, Jio intentionally commoditized the core revenue-generating asset of the traditional telecom industry (voice calls) to construct a vast, highly profitable digital ecosystem encompassing media streaming (JioCinema, JioSaavn), e-commerce (JioMart), and digital payments 596162. Jio fundamentally understood that the customer's "Job-to-be-Done" was no longer simply making a phone call, but rather participating fully in the modern digital economy 6062. By aligning their strategy with the national "Digital India" initiative and targeting previously ignored rural demographics with affordable connectivity, Jio secured an insurmountable transient advantage 606162. By 2023, Jio commanded over 470 million subscribers, handling an astonishing 8% of global mobile data traffic, and entirely reconfiguring the Indian digital arena while devastating legacy rivals who failed to see beyond their traditional industry boundaries 5960.

China and Southeast Asia: The "Super-App" Phenomenon

The rapid proliferation of "Super-Apps" across the Asia-Pacific (APAC) region exemplifies the total obsolescence of single-industry competition in digital environments. A super-app is a centralized, highly integrated platform that consolidates multiple, seemingly disparate services - messaging, e-commerce, ride-hailing, food delivery, healthcare consulting, and sophisticated financial services - into a single, ubiquitous user interface 63642266.

Tencent's WeChat (China), Grab (Southeast Asia), KakaoTalk (South Korea), and Gojek (Indonesia) represent the premier examples of this strategy 19636466. WeChat, launched in 2011, began its lifecycle as a simple messaging application. However, under the guidance of continuous reconfiguration, it rapidly expanded into an all-encompassing lifestyle arena 636422. By embedding mobile payments (WeChat Pay) directly into the social ecosystem, Tencent successfully bypassed the traditional retail banking industry to capture the daily financial transactions of over a billion active users 636422.

These super-apps are engaging in a relentless battle to control the "front end" of consumer attention, which ultimately dictates who owns the primary customer relationship and the associated behavioral data 22. In this digital arena, Western concepts of strict industry separation are entirely irrelevant. A messaging conglomerate (WeChat) competes directly with an e-commerce giant (Alibaba's Alipay), while a company originally founded for ride-hailing (Grab) competes with traditional insurance providers and commercial banks 63642266. The super-app strategy relies heavily on establishing massive network effects and overcoming multi-homing dynamics. This proves that when companies compete for a broad, fundamental "pot of resources" (the user's daily digital life and financial throughput), continuous reconfiguration, ecosystem orchestration, and rapid expansion into completely new service offerings are absolutely essential for survival 196422.

Sino-Indian Resource and Influence Arenas in Africa

On a geopolitical and macroeconomic scale, the analytical concept of the arena extends far beyond consumer software and retail markets. The strategic engagement of both China and India across the African continent illustrates intense competition within the broader, high-stakes arena of global supply chains, critical resource security, and geopolitical influence 232425. Neither nation approaches Africa merely through the traditional lens of an export market; rather, they view the continent as a critical arena for securing the strategic minerals required for the global clean energy transition and guaranteeing future manufacturing dominance 25.

While both emerging powers operate within the exact same arena, their strategic execution and ecosystem orchestration differ vastly. China primarily leverages its state-backed policy banks for rapid, turnkey infrastructure development, tying financing directly to resource extraction agreements within the overarching framework of the Belt and Road Initiative (e.g., establishing strategic port access in Djibouti) 2425. India counters this strategy with a highly distinct, partnership-oriented approach. By utilizing capacity-building initiatives, Exim Bank lines of credit, and deep private sector integration, India aims to build enduring soft power and distinct competitive advantages based on shared developmental goals 2526. This dynamic clearly illustrates how distinct operational capabilities and divergent interpretations of the ultimate "Job-to-be-Done" (e.g., sheer infrastructure speed versus long-term technological and educational partnership) can be deployed symmetrically and competitively in the exact same resource arena.