5 Startup Term Sheet Clauses Founders Misunderstand

A startup term sheet dictates the company's governance, future dilution, and exit economics long before the first wire transfer is initiated. While founders often fixate entirely on the headline valuation, the true cost of venture capital is buried in control mechanisms and downside protections that can ultimately leave a founding team with nothing. Understanding these five standard clauses is the difference between securing a fair financial partnership and making a fatal structural misstep.

Beyond the Headline Valuation: The Anatomy of a Term Sheet

A term sheet is a primarily non-binding blueprint that outlines the core financial and governance terms under which an investor will provide capital to a startup 12. While a few specific clauses - such as confidentiality agreements and "no-shop" exclusivity periods (typically lasting 30 to 60 days) - are legally binding, the vast majority of the document serves merely as the foundation for the definitive legal paperwork that will eventually follow 123. These documents include the stock purchase agreement, the investor rights agreement, and the amended corporate charter 41.

The post-2022 venture capital reset has fundamentally altered the baseline for these negotiations. Following the Zero Interest Rate Policy (ZIRP) era of 2020 to 2022 - which saw an unprecedented capital overhang and wildly founder-friendly terms - the market has stabilized into a more rigorous underwriting environment 27. By nearly every measure, 2025 represented a strong recovery for the venture asset class. Startups tracked on the equity management platform Carta raised a combined $119.5 billion in new funding in 2025, representing a nearly 17% increase year-over-year 3. Furthermore, early-stage valuations demonstrated remarkable resilience; median Series A valuations in the first quarter of 2025 approached $49 million, nearing all-time highs 4.

However, this abundance of capital - heavily concentrated in artificial intelligence and machine learning sectors - masks a highly structured downside protection environment 73. Investors are deploying capital with much stricter governance requirements than they did during the peak of the bull market 25. As the industry adapts to a landscape where large-scale initial public offerings (IPOs) remain challenging and "higher-for-longer" interest rates persist, investors are increasingly utilizing complex legal mechanisms to shield their capital from down rounds and distressed exits 3411.

To navigate this landscape, founders must look past the pre-money valuation - the theoretical worth of the company before the new capital is added - and rigorously scrutinize the legal architecture of the proposed deal 613. A highly attractive valuation paired with predatory term sheet clauses can easily result in the founding team losing operational control or being entirely wiped out during an acquisition.

1. Liquidation Preferences: The Exit Hierarchy

Liquidation preferences are universally considered the most financially consequential terms in any venture capital transaction. They dictate the precise order and the exact magnitude of payouts when a company experiences a "liquidation event" - which typically includes a sale, a merger, an IPO, or a bankruptcy winding-down process 2147.

Understanding Preferred vs. Common Stock

When venture capitalists and institutional funds invest in an early-stage startup, they almost never purchase common stock. Instead, they purchase preferred stock 1316. The defining characteristic of preferred stock is its payout priority. In the event of a sale or liquidation, preferred stockholders are legally entitled to receive their designated proceeds before the common stockholders - which consist almost exclusively of the founders and the employee option pool - receive a single cent 138.

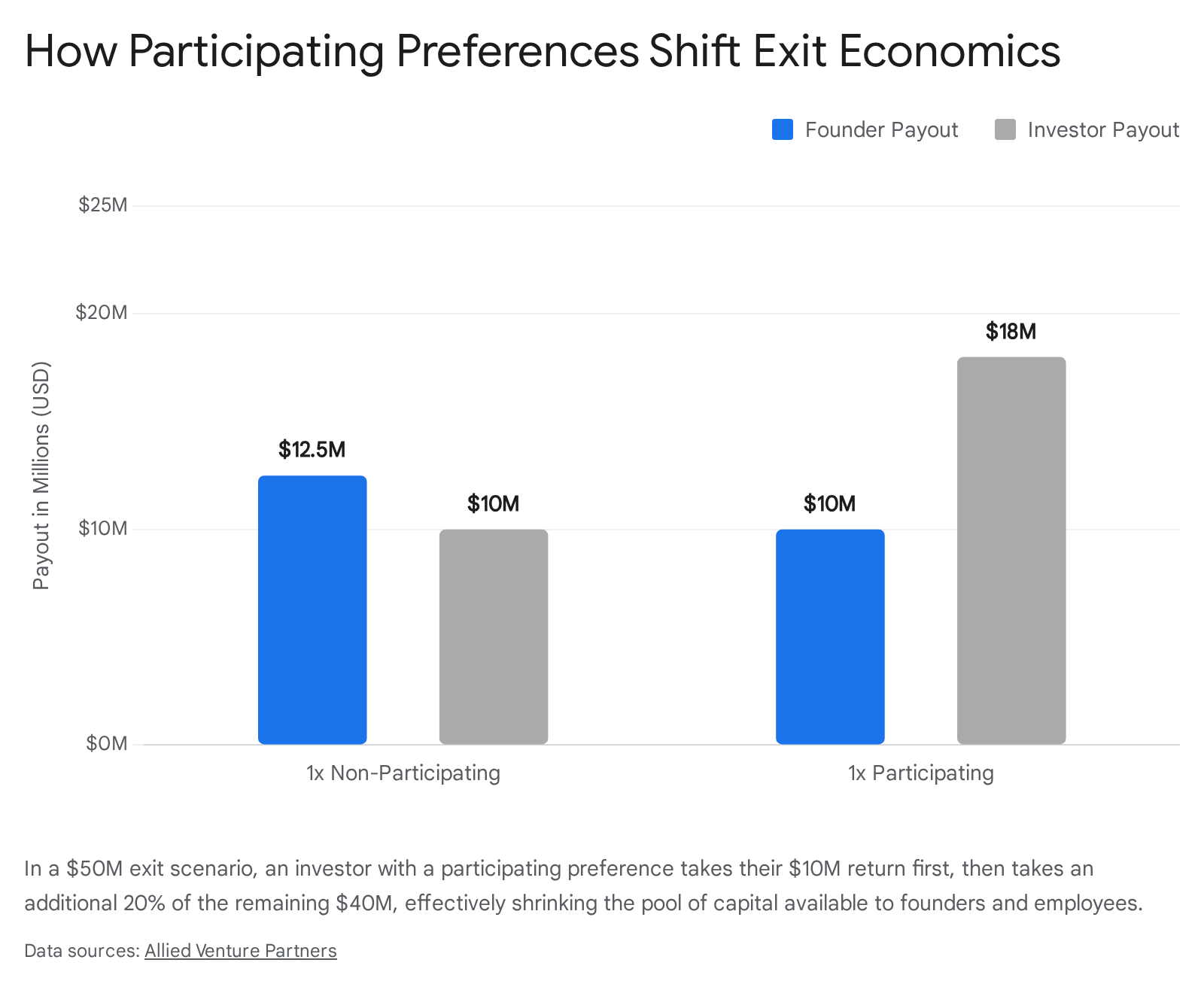

The industry standard for early-stage venture capital is a 1x non-participating liquidation preference 1218. Recent data from Cooley's venture financing reports indicates that an overwhelming 98% of early-stage deals utilized this 1x structure, making it the non-negotiable baseline for a standard, healthy fundraising round 12.

A 1x non-participating preference offers the investor a simple choice at the time of an exit: 1. The Downside Protection Option: They can exercise their preference to receive exactly one times (1x) their original investment amount back off the top of the sale proceeds 219. 2. The Upside Conversion Option: If the company is sold for a massive premium, the investor can choose to forfeit their 1x preference, convert their preferred shares into standard common stock, and take their proportional percentage of the total sale 1619.

For example, if an investor puts $20 million into a startup for a 20% equity stake, and the company is later sold for $50 million, the investor will look at the math. If they take their 1x preference, they get $20 million. If they convert to their 20% proportional ownership, they get $10 million. Naturally, they will choose the $20 million preference, leaving $30 million for the founders and employees. However, if the company is sold for $200 million, their 20% proportional stake is worth $40 million. They will convert to common stock, abandon the 1x preference, and take the $40 million upside 1620.

The Danger of Participating Preferences

The financial danger to founders arises when investors demand a participating preference - a structure colloquially known in the industry as "double-dipping" 1921.

Under a participating structure, the investor does not have to choose between their downside protection and their upside proportion. Instead, they receive their 1x original investment back first, and then they additionally participate in the distribution of the remaining proceeds alongside the common shareholders according to their percentage ownership 1922.

While rare in standard early-stage deals, participating preferences become common in distressed funding environments or later-stage growth rounds where investors perceive higher risk 19. In the first quarter of 2025, participating liquidation preferences appeared in 30% of all down rounds, representing a massive structural shift from just 8% in 2024 4.

Multiples and The Preference Stack

In riskier deals, investors may push for a multiple on their liquidation preference, such as a 2x or 3x multiple 1819. If a venture capital firm invests $50 million with a 2x liquidation preference, they are legally guaranteed the first $100 million of any acquisition before the common stock is assigned any value 823.

As a startup raises consecutive rounds of capital (Series A, Series B, Series C), these liquidation preferences "stack" on top of one another 1922. If a company raises $100 million across four rounds, all $100 million acts as a senior debt-like hurdle that must be cleared during an acquisition before founders see a return 22. Typically, the most recent investors sit at the absolute top of the preference stack, meaning Series C gets paid before Series B, which gets paid before Series A 7.

The FanDuel and Divvy Cautionary Tales

The devastating power of the liquidation preference stack is best illustrated by high-profile exits where massive headline acquisition numbers masked the reality that founders were entirely wiped out.

In July 2018, Paddy Power Betfair (now Flutter Entertainment) acquired the daily fantasy sports startup FanDuel for $465 million in cash 21. To the general public, this appeared to be a monumental victory for the founders and employees who built the platform. However, during previous fundraising rounds, FanDuel's two lead private equity investors had negotiated aggressive liquidation preferences 21. These preferences dictated that the lead investors were entitled to the first $559 million of any liquidity event 21. Because the $465 million acquisition price fell short of the $559 million preference hurdle, the two lead investors legally absorbed every dollar of the transaction. The founders and the employees walked away with absolutely nothing 21. Adding insult to injury, the founders could not block the sale because the investors utilized contractual "drag-along" rights to force the common shareholders to comply with the transaction 1821.

A similar dynamic played out more recently with Divvy, a rent-to-own real estate startup that was acquired for $1 billion 23. Despite reaching unicorn status, the complex financing structures and stacked liquidation preferences required to achieve that high valuation meant that common shareholders, including early employees and founders, reportedly received zero proceeds from the billion-dollar sale 23. Similarly, the UK commission-free investment platform Freetrade was acquired by IG Group for £160 million in early 2025; due to preferences, some later-stage retail crowdfunders faced losses exceeding 80% of their principal, while early preferred investors saw significant returns 23.

Founders must constantly model their exit scenarios. A lower pre-money valuation with a clean 1x non-participating preference will almost always mathematically outperform a higher valuation saddled with a participating structure or a 2x multiple in any moderate exit scenario 2224.

2. Anti-Dilution Protection: The Down-Round Shield

Venture capital operates on the assumption that a startup's valuation will continually increase with each subsequent funding round. When a company raises new capital at a higher price per share than the previous round, it is called an "up round" 425. However, if the company underperforms, or if macroeconomic conditions deteriorate, the company may be forced to raise capital at a lower price per share. This is known as a "down round" 2526.

In 2024, the venture market saw a significant stabilization, yet down and flat fundraising rounds still represented roughly 30% of all completed deals 11. When a down round occurs, the percentage ownership of early investors is heavily diluted, and the overall paper value of their investment drops 2527.

To retroactively protect themselves from this exact scenario, investors demand anti-dilution provisions in their term sheets. If a startup issues new shares at a lower price than the previous investor paid, the anti-dilution clause forces the company to issue additional shares to the previous investor - or lower their conversion price - to partially or fully compensate them for the loss in value 1425.

The Math of Protection: Broad-Based vs. Full Ratchet

Think of anti-dilution protection like buying a ticket to a premium industry conference for $1,000. If the event organizers suddenly drop the price to $500 a week before the event to fill empty seats, an anti-dilution clause acts as a retroactive refund, granting you an extra ticket to ensure you received the actual market value of what you paid 28.

The critical negotiation lies in the specific mathematical formula used to calculate exactly how many "extra tickets" the investor receives. There are two primary mechanisms:

1. Broad-Based Weighted Average: This is the industry standard and widely considered the fair, founder-friendly approach 2026. The weighted average formula does not simply look at the new, lower price; it factors in the magnitude of the down round and the amount of new money being raised relative to the total number of shares already outstanding in the company 2629. By spreading the dilution impact across the entire capitalization table (including the employee option pool), it softens the blow for both the investors and the founders 26. According to the Q1 2025 Entrepreneurs Report by Wilson Sonsini (WSGR), 100% of all reported venture rounds that utilized an anti-dilution provision relied on the broad-based weighted average formula, cementing it as the undisputed market norm 4.

2. Full Ratchet: The full ratchet is a highly aggressive, investor-friendly provision that is extremely toxic to founders 1830. A full ratchet completely ignores how much money is being raised in the down round. It simply resets the earlier investor's original purchase price to the new, lower price 2530. For example, if a Series A investor originally bought shares at $10.00, and a distressed Series B round issues even a handful of shares at $5.00, a full ratchet provision retroactively acts as if the Series A investor bought all their original shares at $5.00 25. This effectively doubles the Series A investor's share count overnight, absorbing massive amounts of equity directly from the founders and the employee option pool 2527. Full ratchets are highly punitive, can destroy morale, and act as a severe deterrent to new investors looking to inject fresh capital into a struggling business 2627.

The Rise of "Pay-to-Play" Mechanisms

While broad-based weighted average protection is the standard, investors are increasingly attaching conditions to its enforcement. Enter the "pay-to-play" provision.

A pay-to-play clause stipulates that an existing investor must participate in the new, distressed down round by investing additional capital (usually their pro-rata amount) to retain the benefit of their anti-dilution protection 30. If the investor refuses to put more money into the struggling company, they are penalized. The penalty usually involves losing their anti-dilution rights, losing their board seat, or having their existing preferred shares forcibly converted into standard common stock 30.

In the post-ZIRP environment, these provisions have skyrocketed as venture funds attempt to force syndicates to support struggling portfolio companies. In the first quarter of 2025, the percentage of pay-to-play provisions in down rounds spiked dramatically to 50%, up from just 27% in 2024 4. This trend highlights a fierce landscape where late-stage investors are aggressively hedging against downside risk and punishing early-stage investors who lack the dry powder to participate in bridge rounds 49.

3. Pro-Rata Rights: The Cap Table Crowd-Out

Pro-rata rights - frequently referred to as pre-emptive rights or participation rights - grant an existing investor the contractual option to participate in future funding rounds to maintain their exact percentage of ownership in the company 201011.

The concept is straightforward. If you think of a startup as a pizza, each investor owns a specific slice. Every time the company raises a new round of funding, it issues new shares, effectively baking a larger pizza 34. Without pro-rata rights, the existing investors' slices mathematically shrink (dilution) relative to the size of the new pie 34. Pro-rata rights give the investor the option to pitch in additional capital to buy enough of the new pizza to ensure their slice remains the exact same size 3435.

For venture capitalists, pro-rata rights are vital. They allow funds to double down on their winning portfolio companies, protecting against dilution while signaling conviction to their own Limited Partners (LPs) 1134. The right is strictly an option, not an obligation; the investor can walk away if the new valuation is too high or the company is underperforming 3435.

The Founder's Dilemma: Overcrowding the Round

While granting pro-rata rights to early seed investors feels like a fair reward for their early conviction, it creates a massive structural headache for founders during the Series B or Series C rounds. This phenomenon is known as cap table crowd-out 3435.

When a new lead venture capitalist approaches a startup to lead a Series B round, they generally demand a meaningful ownership stake - typically 20% to 25% of the company - to justify their time, their due diligence costs, and their firm's economic models 36.

However, if every angel investor, seed fund, and Series A investor exercises their contractual pro-rata rights, the total allocation of new shares will be rapidly consumed 1135. The founders are then trapped in a mathematical paradox: there is not enough equity to satisfy the existing investors and give the new lead investor their required 20% 11. To make the math work, the founders are usually forced to expand the total size of the round, issuing far more shares than originally planned and suffering severe, unnecessary personal dilution 3435.

Strategic Defenses: Thresholds and Decay

Founders must carefully manage pro-rata rights from the very first term sheet. The most effective defense is to restrict pro-rata rights strictly to "Major Investors" 3435. By setting a high financial threshold - for example, granting the right only to entities that write checks over $250,000 - founders prevent dozens of small angel investors from cluttering the capitalization table and complicating the administrative logistics of future rounds 135.

Another emerging concept in the venture community is the idea of "decaying" pro-rata rights. Prominent venture capitalists have noted that guaranteeing a permanent right to maintain ownership forever becomes mathematically unsustainable. A decaying pro-rata right operates like a half-life: an early-stage investor might be allowed to maintain 100% of their pro-rata in the Series A, but only 50% in the Series B, and 25% in the Series C, organically freeing up equity allocation for new growth investors as the company scales 36. While not yet an industry standard, the concept highlights the immense friction these rights cause in later stages.

4. Board Control and Protective Provisions

A term sheet is a governance document just as much as it is a financial one. It establishes the permanent power dynamics of the corporation, dictating exactly who holds the authority to fire the executive team, pivot the product roadmap, or execute an IPO 1437.

Board Composition

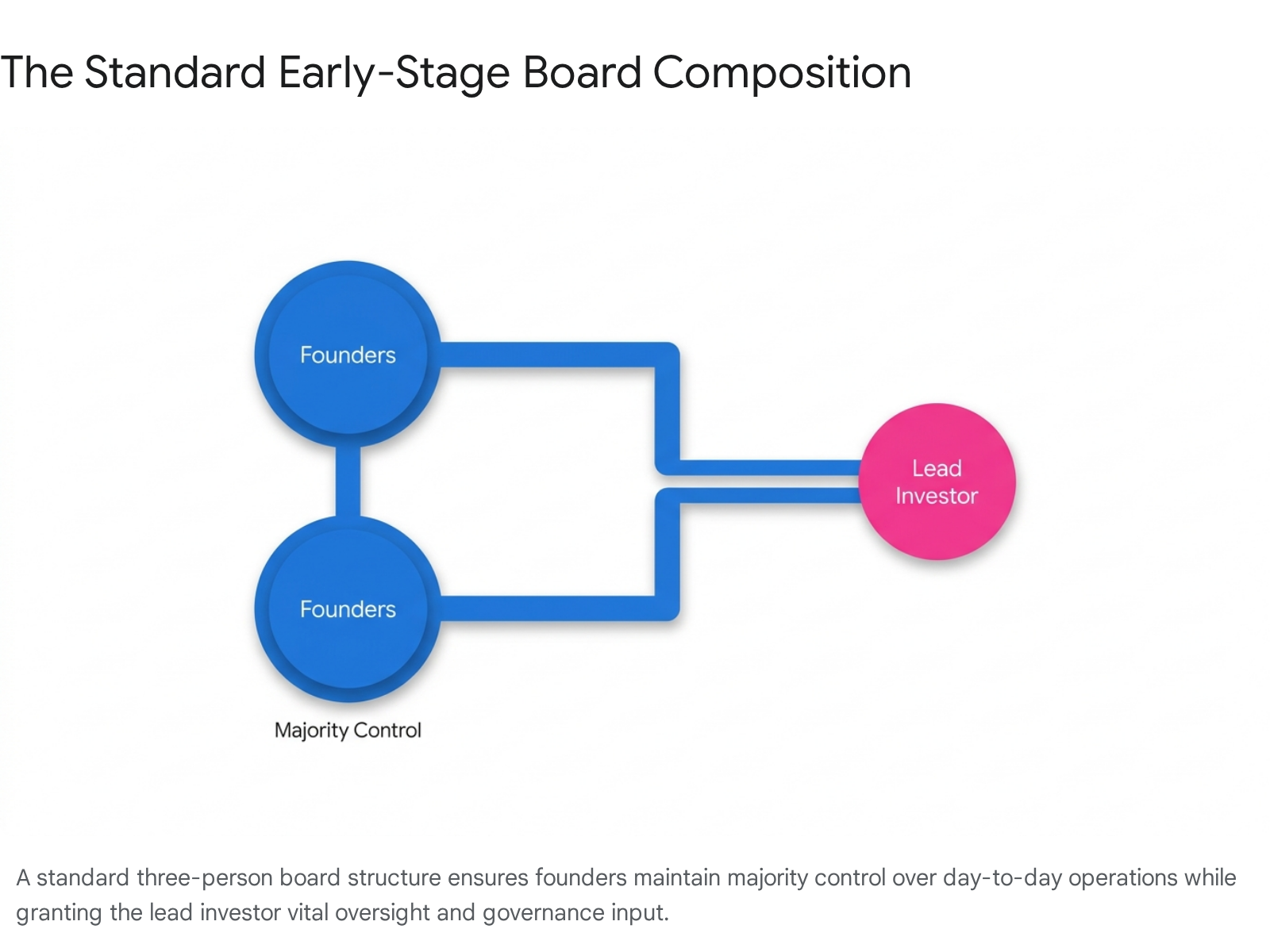

The Board of Directors is the ultimate governing body of a startup. At the Seed or Series A stage, the market standard is a concise, three-person board: two seats allocated to the founders (usually the CEO and one co-founder), and one seat allocated to the lead venture capital investor 22838. This structure is inherently founder-friendly, ensuring that the founding team maintains majority voting control over day-to-day operations while giving the institutional investor a formal fiduciary voice and direct insight into strategic planning 239.

As the company raises subsequent rounds, the board generally expands to five members. A standard Series B board might consist of two founders, two investors (the Series A lead and the Series B lead), and one mutually agreed-upon independent director recruited from the broader business community 2438. Founders must be hyper-vigilant about conceding board seats early in the company's lifecycle. A term sheet that demands an investor-majority board at the seed stage is a glaring red flag, as it legally permits the investors to replace the founder as CEO without cause 3940.

Protective Provisions (Veto Rights)

Even if the founders safely maintain a majority of the board seats, investors guarantee their influence through contractual "protective provisions." Also known as negative covenants or veto rights, protective provisions are a list of fundamental corporate actions that the company legally cannot undertake without the explicit, separate consent of the preferred shareholders 2841.

These provisions are standard in almost all venture deals. However, the exact scope of what actions require an investor veto is intensely negotiated. A standard, balanced term sheet will restrict protective provisions to massive structural or economic changes, such as: * Selling the company or merging with another entity 218. * Liquidating or dissolving the corporation 42. * Issuing new shares that are senior to or equal to the current investors' stock 1642. * Taking on massive amounts of debt outside the normal course of business 29. * Changing the number of authorized board seats 716.

The danger arises when investors attempt to slip broad operational vetoes into the protective provisions. Founders should aggressively push back against term sheets that require investor consent for routine business moves, such as setting annual budgets, altering standard employee compensation, hiring or firing non-C-suite executives, or signing standard commercial leases 162940. Handing investors veto power over daily operations functionally strips the CEO of their ability to run the company 40.

Global Disparities in Control Governance

It is critical to note that market standards for governance and veto rights vary radically depending on the legal jurisdiction in which the startup is domiciled. The globalization of venture capital has led to three dominant regional frameworks that shape how term sheets are constructed.

| Regional Model | Market Standard Documentation | Stance on Founder Control & Veto Rights |

|---|---|---|

| United States | National Venture Capital Association (NVCA) | Highly Founder-Friendly. Driven by fierce competition for top talent. Veto rights are strictly limited to major corporate actions impacting economic or governance rights 1213. |

| Europe & UK | British Private Equity & Venture Capital Association (BVCA) | Balanced / Investor-Protective. Historically influenced by traditional private equity. Includes more granular controls, though the 2023 updates shifted slightly closer to US founder-friendly norms 1245. Pre-emptive rights are statutory rather than just contractual 1314. |

| Asia & Middle East | Venture Capital Investment Model Agreements (VIMA / Singapore) & Local Standards | Highly Investor-Friendly. Term sheets frequently include extensive operational protective provisions. Investors routinely negotiate enhanced redemption rights, robust veto powers over day-to-day matters, and higher liquidation multiples 1213. |

Founders operating in emerging markets or European jurisdictions must be aware that "Silicon Valley standard" NVCA terms are not automatically applicable globally, and local investors will expect significantly more structural control over the business 1213.

The catastrophic potential of misaligned contractual jurisdiction and intellectual property control is perfectly illustrated by the Skype acquisition saga. When eBay attempted to sell Skype in 2009 for billions of dollars, the deal was paralyzed because Skype's original founders, Niklas Zennström and Janus Friis, had retained ownership of the core peer-to-peer technology through a separate company called Joltid 15. Joltid sued in US courts to terminate the software license, leveraging the fact that the original contract assumed UK jurisdiction. By leveraging IP rights and contractual fine print across international borders, the founders successfully stalled a massive corporate transaction and forced a settlement 15. While a unique scenario, it underscores how governance, jurisdiction, and contractual control mechanics dictate the ultimate fate of billions of dollars.

5. Founder Vesting: Earning Your Own Shares

Perhaps the most counterintuitive concept for first-time founders is that, upon taking venture capital, they do not immediately own their shares outright. Investors view the founders - their vision, their technical capability, and their leadership - as the primary asset of an early-stage startup 14. If a founder were allowed to retain 100% of their equity and quit the day after a $5 million seed round closed, the investors would be left holding a worthless shell company.

To mitigate this risk, term sheets universally require founder equity to be subjected to a vesting schedule 144048.

The industry standard for founders is a four-year vesting schedule paired with a one-year "cliff" 4016. This means that the founder must remain employed by the company for 12 continuous months to earn their first tranche (25%) of equity. If they leave or are fired on day 364, they walk away with exactly 0% permanent equity 4016. After the one-year cliff is cleared, the remaining 75% of the shares vest in equal monthly increments over the next 36 months 4016.

Acceleration Clauses: Protecting the Downside

A major point of negotiation in founder vesting is the acceleration clause, which dictates what happens to unvested shares if the company is acquired before the four-year schedule is complete 2016.

- Single-Trigger Acceleration: This is highly founder-friendly. It dictates that if the company is sold, 100% of the founder's unvested shares immediately vest and convert to cash or acquiring company stock. The "single trigger" is the sale of the business 2016.

- Double-Trigger Acceleration: This is the more common, investor-preferred compromise. For the shares to accelerate, two events must occur: (1) the company must undergo a change of control (sale), and (2) the founder must be terminated without cause or forced to take a severely diminished role by the new acquiring company within a specific timeframe (usually 12 months) 2016. This protects the acquiring company, allowing them to retain the founders via "golden handcuffs" while assuring the founders they cannot be fired immediately after the deal closes simply to strip them of unvested stock.

Leaver Provisions and the US vs. European Divide

How a company handles a departing founder before an exit is another area marked by massive geographical disparities.

Under the US model governed by NVCA standards, founder vesting is managed through a repurchase right 45. If a founder leaves the company, the company simply executes its right to buy back the unvested portion of their shares at a nominal cost (often fractions of a penny) 45. The departing founder is generally permitted to keep all of the shares that have already vested, regardless of why they left, and they retain their voting rights on those vested shares 4514. The US model rarely employs "Bad Leaver" penalties, and recent 2024/2025 updates to NVCA guidelines formally removed founders' personal liability for representations and warranties, cementing a founder-favorable environment 1314.

Conversely, the UK and European model, governed by BVCA standards, is significantly more punitive. European term sheets routinely feature "Good Leaver / Bad Leaver" clauses embedded directly into the shareholders' agreement 451450. A "Good Leaver" is typically someone who leaves due to death, severe illness, or wrongful termination. They are allowed to keep their vested shares. A "Bad Leaver" is defined broadly as a founder who resigns without "good reason" or is terminated for cause 45. Crucially, if designated a Bad Leaver, a European founder can be legally forced to sell all of their shares - including their fully vested shares - back to the company or the remaining shareholders, effectively wiping out their entire economic interest in the business they started 4514.

The Ultimate Weapon: Corporate Restructuring

Founders who assume that their raw percentage of ownership makes them untouchable fundamentally misunderstand corporate law. Vesting mechanics, combined with board control, can be weaponized in founder disputes to systematically dilute and erase early partners.

The most infamous example in modern tech history is Eduardo Saverin's ousting from Facebook. Originally, Mark Zuckerberg, Eduardo Saverin, and Dustin Moskovitz formed TheFacebook.com as a Florida Limited Liability Company (LLC) 51. Saverin held roughly 30% of the equity, while Zuckerberg held 65% 51. Because of the LLC structure and Saverin's massive stake, he held effectively unassailable voting blocks regarding certain corporate actions 52.

When Facebook secured its first major angel investment from Peter Thiel, the investment was contingent upon the company reorganizing from a Florida LLC into a standard Delaware C-Corporation, which is the gold standard for venture-backed startups 5152. Saverin, who was living on the East Coast and increasingly disconnected from operations, reportedly lagged on providing his required member vote to authorize the transition 52.

Rather than remain stagnant, Zuckerberg and his legal team executed a complex, hostile corporate maneuver. They formed an entirely new entity in Delaware. This new Delaware corporation then formally acquired the old Florida LLC 5152. The existing members of the LLC were granted shares in the new Delaware entity proportional to their old holdings, resulting in Saverin owning roughly 24% of the new company 51.

However, the new Delaware C-Corp was structured with a massive block of newly authorized, unissued shares 5253. Because Saverin had ultimately signed an agreement relinquishing his intellectual property rights and certain voting powers during the transition, he lacked the protective provisions to stop what happened next 5153. In early 2005, Zuckerberg issued millions of new shares in the Delaware entity as compensation to himself, Moskovitz, and active employees - explicitly excluding Saverin, who was no longer an active employee 5153. Because Saverin's shares were not protected by anti-dilution clauses against employee option pool expansions, this massive issuance of new stock mathematically crushed his percentage ownership 5153. Subsequent venture rounds further diluted Saverin, reducing his stake from 30% down to less than 10% by the time of the IPO 5153.

While Saverin eventually sued for breach of fiduciary duty and settled for a stake that made him a multi-billionaire, the strategy employed against him was ruthlessly effective 5254. The Facebook saga serves as the ultimate case study in why raw ownership percentages are meaningless without the underlying legal architecture to protect them. Without strict board representation, protective provisions, and a clear understanding of corporate restructuring mechanics, an unwanted founder can be legally diluted into irrelevance 5253.

Bottom line

A startup term sheet is far more than a simple mechanism to establish a company's pre-money valuation; it is the legal DNA that governs the future of the business. By understanding how liquidation preferences divert exit capital, how anti-dilution clauses shift economic risk during down rounds, and how board composition and veto rights dictate ultimate operational control, founders can negotiate from a position of profound strength. While macroeconomic venture capital markets will inevitably fluctuate between favoring investors and founders, standardizing and defending these five key clauses ensures that the individuals building the company retain the value they ultimately create.