How Funding Rounds Affect a Startup's Cap Table

A startup's capitalization table mathematically transforms during each funding round as new shares are issued to venture capitalists, systematically diluting the percentage owned by early founders and employees. This evolution introduces complex preferred stock rights, such as liquidation preferences and anti-dilution protections, which dictate the ultimate financial payout during a company sale or initial public offering. Understanding these mechanisms is crucial, as owning a large percentage of a company on paper does not guarantee a proportional financial return in a modest exit.

What Is a Capitalization Table?

A capitalization table, universally referred to as a cap table, serves as the definitive legal and mathematical ledger of a company's ownership structure. In the earliest days of a startup, this document is usually a simple spreadsheet indicating that the founding team owns one hundred percent of the company's equity 12. However, as the company matures and begins accepting external capital, the cap table evolves into a highly complex, multi-sheet financial model. It must meticulously track the issuance of common shares, preferred shares, stock options, warrants, and convertible debt instruments like Simple Agreements for Future Equity (SAFEs) 34.

The cap table is not merely a historical record; it is a dynamic forecasting tool that dictates corporate governance, voting rights, and the precise mathematical distribution of capital during a liquidity event 356. Errors or oversights in maintaining this document can lead to severe legal complications during fundraising audits and can significantly diminish the financial returns expected by early stakeholders 31.

The Transition from Common to Preferred Stock

To comprehend how a cap table evolves, one must first distinguish between the two primary classes of equity: common stock and preferred stock.

Founders, early employees, and advisors typically hold common stock 2910. In corporate finance, common stock represents a "residual claim" on the company's assets and earnings 2101112. This means that in the event of a company sale, liquidation, or bankruptcy, common shareholders are entitled only to the capital that remains after all creditors, debt holders, and preferred investors have been fully satisfied 9101113. If a startup achieves a massive valuation, common stock performs exceptionally well. However, in an average or distressed exit, common shareholders are positioned at the bottom of the payout hierarchy and are the most vulnerable to being wiped out 2.

Conversely, venture capitalists and institutional investors purchase preferred stock 291012. Preferred stock is a hybrid financial instrument designed to provide downside protection while maintaining upside potential 11012. It legally sits above common equity on the balance sheet and comes bundled with aggressively negotiated contractual rights 101213. These rights include liquidation preferences, anti-dilution protections, dividend accruals, and specialized voting controls that govern the risk profile of the company 91012. The introduction of preferred stock in a Series A financing round is the moment a cap table permanently shifts from a simple percentage split into a tiered financial hierarchy.

Authorized Versus Issued Shares

A frequent source of confusion for early-stage founders is the distinction between authorized shares and issued shares. When a startup formally incorporates as a C-Corporation, it must state the maximum number of shares it is legally permitted to create. This ceiling is known as the authorized share count 14. Often, startups will authorize a large pool, such as ten million shares, to provide flexibility for future growth 114.

However, the company does not immediately hand out all ten million shares. The founding team might initially issue themselves a total of eight million shares, splitting them evenly 14. At this stage, eight million shares are issued and outstanding, and the founders own one hundred percent of the equity 14. The remaining two million authorized shares sit essentially dormant, resembling unbaked clay, ready to be issued to future investors or placed into an employee stock option pool 114. Ownership percentages are calculated strictly based on the shares that have been issued, not the total number authorized 14.

The Mechanics of Equity Dilution

A fundamental misconception among first-time founders is visualizing their startup's equity as a single pizza that is sliced into increasingly smaller pieces to accommodate new investors 15. This analogy misrepresents corporate law. In reality, equity dilution occurs through the expansion of the total share count, a concept better visualized as adding new bricks to a growing wall 15.

The Expanding Pie Analogy

When a startup raises money, it does not transfer the founders' existing shares to the venture capitalist. Instead, the company issues entirely new shares of preferred stock to the investor in exchange for cash 151617. This action dilutes the ownership percentage of all existing shareholders by increasing the denominator in the ownership equation 151618.

Consider a basic example: A founder starts a company and holds one hundred shares, representing one hundred percent ownership 16. The founder decides to raise external capital and issues twenty-five brand-new shares to an angel investor. The founder still owns exactly one hundred shares, but the total number of shares outstanding has increased to one hundred and twenty-five. The founder's ownership stake mathematically drops to eighty percent, while the investor secures twenty percent 1619. Nobody "took" the founder's equity; there are simply more shares in existence.

The strategic rationale behind accepting dilution is the expectation that the injected capital will dramatically increase the overall enterprise value of the startup. Founders accept a smaller percentage of ownership because they believe the new funds will allow the company to grow faster, making their reduced slice of the pie far more valuable in absolute dollar terms than total ownership of an unfunded, stagnant business 1617.

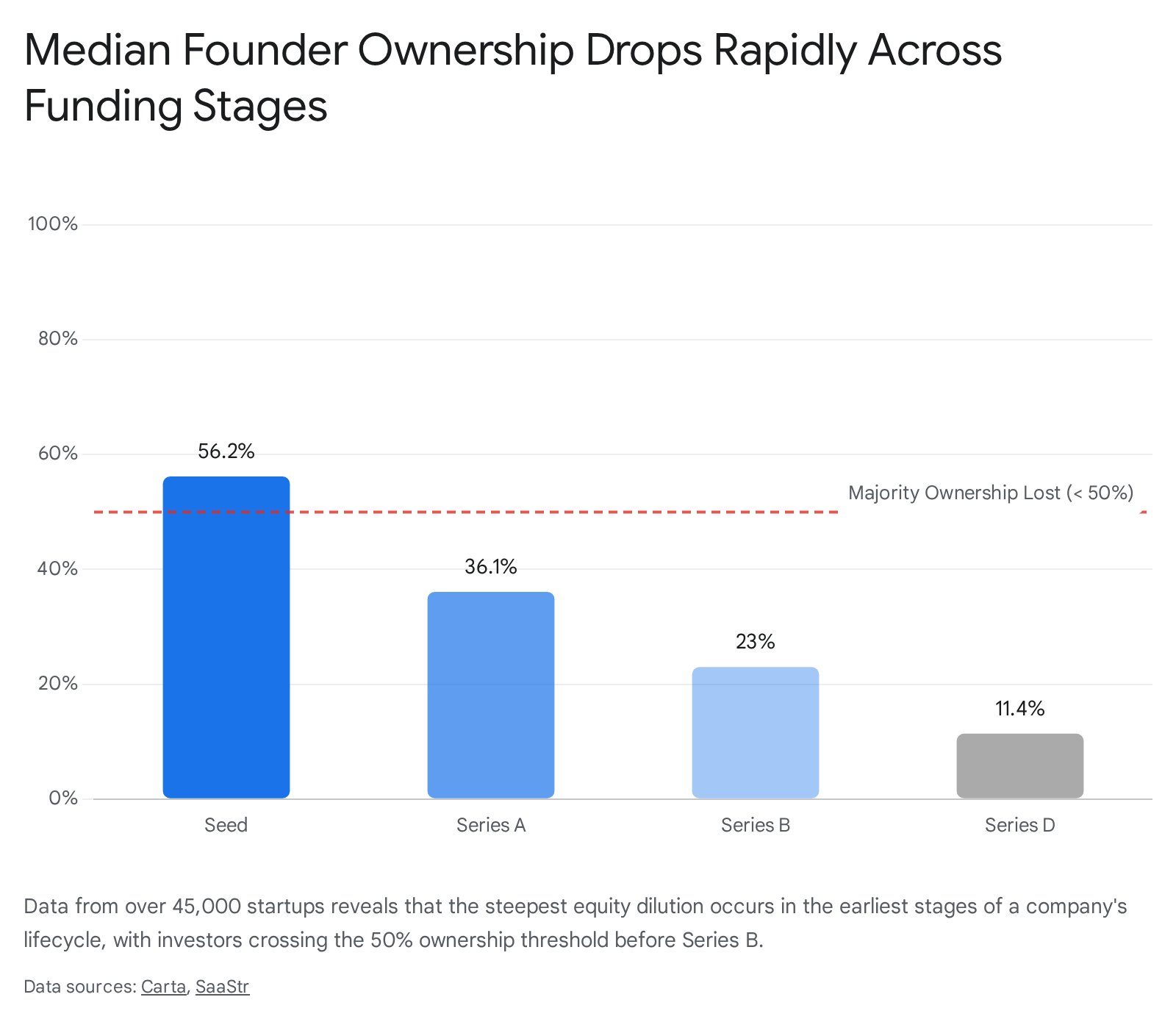

Median Founder Ownership Data by Stage

Because nearly every successful venture-backed technology company requires multiple rounds of capital to scale, dilution on the cap table is compounding and unavoidable. Recent market data analyzed by equity management platforms like Carta, which evaluated over forty-five thousand startups incorporated over the last decade, illustrates precisely how aggressive this dilution curve is across the startup lifecycle 321.

The data shows that founder ownership deteriorates most rapidly during the earliest funding stages, where institutional investors demand larger equity stakes to offset the immense risk of backing an unproven product 322. Following a formal priced Seed round, the median founding team collectively retains 56.2 percent of their startup's equity 323. The dilution suffered in a standard Seed round typically averages around 19.5 percent 16.

As the company progresses to a Series A round, the dilution accelerates. The median Series A round demands roughly 17.9 to 18 percent of the company's equity, pulling the median founder ownership down to just 36.1 percent 1634. The interval between a Seed round and a Series A round has also stretched significantly in recent years, reaching a median of 2.1 years, forcing founders to operate leaner operations before securing follow-on capital 23.

By the time a startup successfully closes a Series B round, the median founding team owns just 23.0 percent of the business 323. This means that by the growth stage, external investors and employees collectively own more than three-quarters of the cap table. If a company survives to raise a late-stage Series D round, founders are statistically left holding a median of 11.4 percent of the equity 23. Consequently, venture capital investors cross the threshold into majority ownership somewhere between the Series A and Series B milestones 23.

Interestingly, while the dilution curve remains steep, the composition of founding teams has shifted. The percentage of venture-backed startups led by a solo founder has doubled over the past ten years, reaching thirty-five percent of all incorporations in 2024 3. However, solo founders face systemic hurdles in fundraising, accounting for only seventeen percent of the companies that actually managed to close a venture capital round that same year 3.

Valuations and the Option Pool Shuffle

As a startup navigates from informal angel checks to formal priced equity rounds led by institutional venture capitalists, the mathematical translation of cash into shares is governed by a few critical formulas. The valuation of the company sets the price per share, which directly dictates exactly how much of the cap table the new investors will absorb 1255.

Pre-Money vs. Post-Money Mathematics

When entering term sheet negotiations, founders must be hyper-vigilant regarding the distinction between pre-money and post-money valuations. A single misunderstood word in a term sheet can inadvertently shift millions of dollars in equity value from the founders to the investors 27.

The core formulas driving cap table expansion are straightforward in theory: 1. The post-money valuation is equal to the pre-money valuation plus the total new investment amount 52728. 2. The investor's ownership percentage is calculated by dividing their investment amount by the post-money valuation 2552728. 3. The price per share is calculated by dividing the pre-money valuation by the total fully diluted share count existing immediately prior to the investment 255.

If an investor offers an entrepreneur a term sheet for a two million dollar investment based on an eight million dollar pre-money valuation, the post-money valuation becomes ten million dollars 2829. The investor will purchase twenty percent of the company's equity. This calculation seems simple, but venture capital term sheets rarely apply this math in a vacuum. They almost universally introduce a structural mechanism that silently lowers the effective valuation for the founders.

How the Option Pool Penalizes Founders

To recruit and retain top-tier talent without depleting cash reserves, startups utilize an employee stock option pool (ESOP) 13031. During a fundraising event, venture capitalists almost invariably require the company to create or expand this option pool so that the business has enough equity to hire key executives over the next twelve to eighteen months 2830326. The industry standard size for an option pool typically ranges between ten and twenty percent of the company's fully diluted post-money equity 252831326.

The mathematical controversy lies in how this pool is funded. Investors routinely insist that the unallocated option pool be carved out of the pre-money valuation rather than the post-money valuation 25527282930326. This widespread practice is known as the "option pool shuffle" 272830326.

By forcing the option pool into the pre-money capitalization, the entirety of the dilution required to create those future employee shares is borne exclusively by the founders and existing early shareholders 527283032. The new investor's percentage is calculated after the founders have mathematically diluted themselves to create the pool 27. This structure effectively lowers the "true" pre-money valuation the founders are receiving for their business 25527282930326.

| Metric | Founder Assumption (No Pool Adjustment) | The Reality (The Option Pool Shuffle) |

|---|---|---|

| Headline Pre-Money Valuation | €5,000,000 | €5,000,000 |

| Investment Amount | €1,000,000 | €1,000,000 |

| Post-Money Valuation | €6,000,000 | €6,000,000 |

| Value of Required Option Pool | €0 | €900,000 (15% of €6M Post-Money) |

| Effective Pre-Money for Founders | €5,000,000 | €4,100,000 |

| VC Ownership Stake | 16.7% | 16.7% |

| Option Pool Stake | 0% | 15.0% |

| Founder Retained Equity | 83.3% | 68.3% |

Table: The severe mathematical impact of creating a 15% option pool in the pre-money valuation. The required pool's value is carved directly out of the founders' equity, reducing their effective valuation significantly and compounding their dilution 32.

The irony of the option pool shuffle is that if the startup is eventually acquired, any unissued options remaining in the pool are typically canceled. Because the total number of outstanding shares shrinks, all shareholders - including the investors - benefit proportionally from the unused pool, even though the founders paid the entire dilution cost to create it upfront 1630. Consequently, a primary defense strategy for founders entering term sheet negotiations is to build a highly precise, bottom-up hiring plan. By proving exactly which roles need to be filled, founders can justify a smaller option pool requirement (for example, ten percent instead of twenty percent), thereby minimizing unnecessary equity surrender 18567.

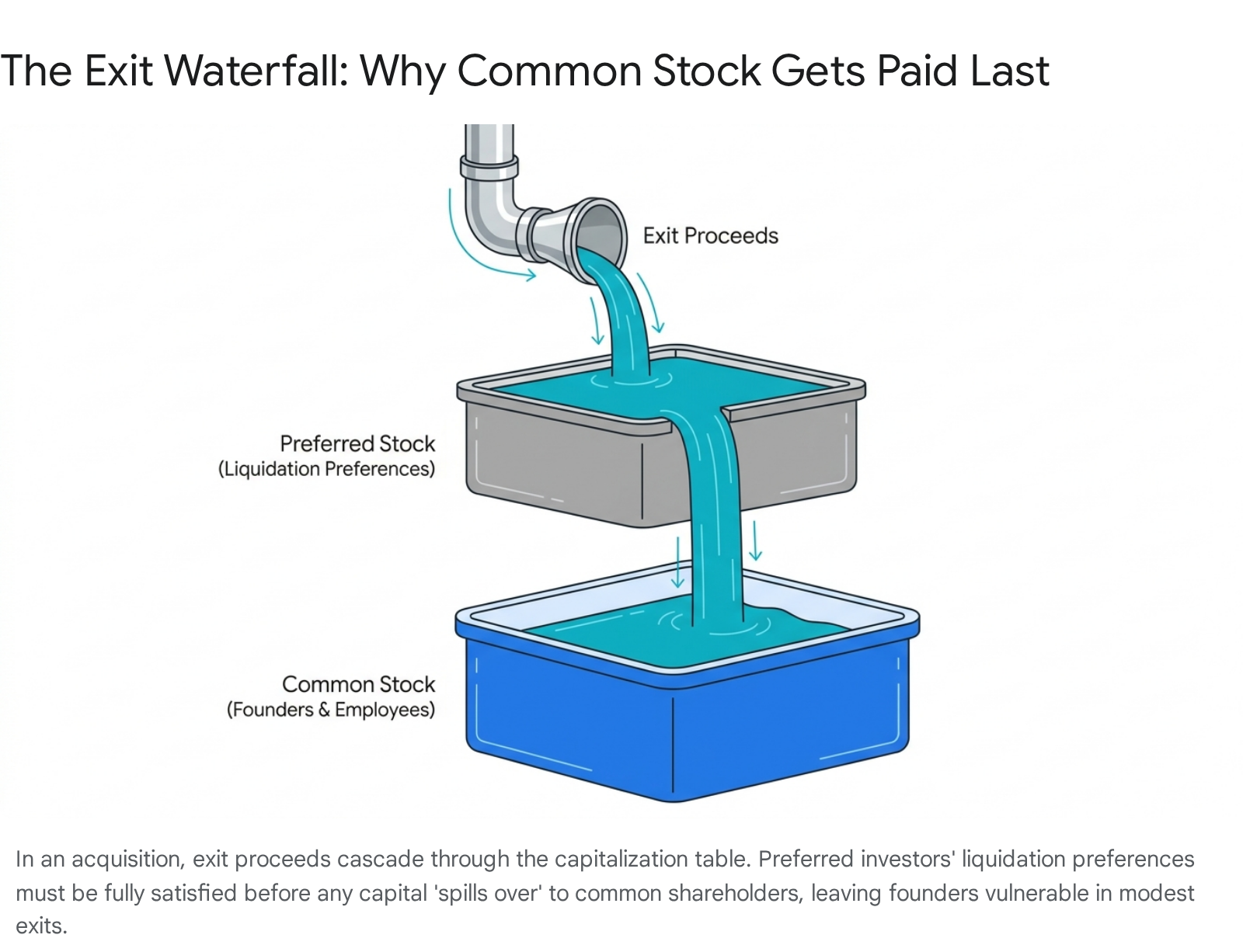

The Exit Waterfall and Liquidation Preferences

The ultimate test of a capitalization table occurs during a liquidity event, such as a corporate acquisition or a public offering. The percentage ownership listed on a spreadsheet rarely translates directly into the actual percentage of cash a shareholder receives 35. Instead, the financial payout is calculated via a "waterfall analysis," which models how the cash proceeds flow down through the company's capital structure, tier by tier, according to the contractual rights embedded in the preferred stock 135368.

Priority Payouts and Multiples

The cornerstone of the exit waterfall is the liquidation preference. This contractual clause acts as a foundational safety net, guaranteeing that preferred investors recover their initial capital investment before any common shareholder receives a single dollar 93583894010.

The size of this priority payout is determined by a preference multiple. A standard 1x liquidation preference ensures the investor gets exactly their original investment amount returned to them 93594042. Higher multiples - such as 2x or 3x - dictate that the investor must be paid double or triple their initial check before the waterfall overflows to the founders 9404211. While punitive high multiples were common in early historical market bubbles, modern venture ecosystems heavily favor 1x preferences, with roughly 96 percent of deals in late 2024 featuring a standard 1x multiple 404412.

If a startup's exit value falls short of the total capital raised across all funding rounds, the cap table enters a scenario occasionally referred to as the "zero zone" 2. For example, if a startup raises thirty million dollars across three funding rounds and is later acquired for a disappointing twenty-five million dollars, every dollar of the acquisition price is swallowed by the investors satisfying their liquidation preferences. Even if the founders theoretically own forty-five percent of the company's equity on paper, they will receive absolutely nothing from the sale 240.

Participating vs. Non-Participating Preferred Stock

Once an investor recovers their initial capital via the liquidation preference, the cap table rules dictate how the remaining proceeds are distributed. This mechanism splits preferred stock into two distinct and highly debated categories:

Non-Participating Preferred Stock: This structure is widely considered the market standard and is the most founder-friendly approach 240. Under non-participating terms, investors face a fork in the road: they can either claim their guaranteed 1x liquidation preference, or they can choose to convert their preferred shares into common stock and take a purely percentage-based share of the total exit value 935363840. They cannot do both. Rational investors will run the math at the time of the exit and choose whichever option yields the higher financial return.

Participating Preferred Stock: This structure is deeply unfavorable to founders and actively enables investors to "double-dip" into the exit proceeds 29354010. Under participating terms, the investors first extract their 1x liquidation preference right off the top of the waterfall. After their initial capital is secured, they do not step aside. Instead, they participate pro-rata alongside the common shareholders in whatever proceeds remain, leveraging their equity percentage to take a second massive bite of the remaining capital 9353638401046.

To grasp how drastically participating preferred stock alters the cap table mathematics, consider a scenario where a startup has raised thirty million dollars in exchange for forty percent of the company, leaving the founders with sixty percent. Years later, the company is sold for fifty million dollars 2.

- Under 1x Non-Participating Terms: The investors calculate that converting to common stock yields twenty million dollars (forty percent of the fifty-million-dollar exit), which is less than their thirty-million-dollar liquidation preference. They opt to take the thirty-million-dollar preference. The remaining twenty million dollars flows entirely to the founders and employees. The founders receive twenty million dollars 2.

- Under 1x Participating Terms: The investors take their thirty-million-dollar preference off the top. This leaves twenty million dollars in the waterfall. Because they hold participating rights, they additionally claim forty percent of that remaining twenty million dollars (an additional eight million dollars). The investors walk away with thirty-eight million dollars, leaving the founders with just twelve million dollars despite owning the vast majority of the company 2.

To mitigate the catastrophic severity of participating stock, founders will occasionally negotiate a "participation cap," usually set at a 2x or 3x multiple 940101146. This limits the investor's double-dipping behavior. Once the investor's combined returns reach the capped multiple, they stop participating in the remainder and must fully convert to common stock if they want a larger share of a massive exit 9401146.

| Preference Type | Mechanism in an Exit Scenario | Impact on Founder Payout | Market Standard |

|---|---|---|---|

| Non-Participating | Investor chooses the greater of their liquidation preference or their pro-rata ownership percentage. | Highly Favorable. Creates a clean split of proceeds once the exit clears the preference threshold. | Yes. Comprises the vast majority of modern venture financings. |

| Participating | Investor takes their liquidation preference and then double-dips to take their pro-rata percentage of the remaining capital. | Punitive. Severely diminishes the cash available to common shareholders in moderate exits. | No. Typically seen only in distressed rounds or heavily investor-favored markets. |

| Capped Participating | Investor double-dips until their total return hits a predetermined multiple ceiling (e.g., 3x), at which point participation stops. | Moderate. Acts as a compromise, allowing investors extra upside while protecting founders in large exits. | Occasional. Used as a middle ground during difficult negotiations. |

Table: A comparative breakdown of liquidation preference structures and their impact on common stockholders during an exit event 2935363840.

Preference Stacking and Seniority

As startups raise multiple successive funding rounds (Series A, Series B, Series C), the cap table accrues multiple, overlapping layers of liquidation preferences. How these layers interact within the waterfall is determined by the negotiated seniority structure 3810424412.

The most common approach in multi-round companies is the Standard Seniority structure, often referred to as a stacked or Last-In, First-Out (LIFO) model 381044. Under this hierarchy, the investors from the latest funding round (e.g., Series C) get paid their full liquidation preference first. If any capital remains in the waterfall, the Series B investors are paid, followed sequentially by Series A, and finally, the common shareholders 381044. This structure heavily protects late-stage institutional capital but places early angel investors and founders at immense risk in a mediocre exit 38401044. Data indicates that demands for senior preferences surged significantly during the recent market tightening, appearing in forty-seven percent of later-stage deals in 2023 4412.

The alternative approach is a Pari Passu structure, a Latin term meaning "on equal footing." Under pari passu, all preferred investors across all funding rounds are treated equally 36838. If the exit proceeds are insufficient to satisfy all the outstanding liquidation preferences, the available funds are distributed proportionally among the investors based on the size of their original capital contributions 38. This structure is generally considered friendlier to founders and early backers, as it prevents late-stage investors from monopolizing a modest exit 38.

Navigating Down Rounds and Anti-Dilution Provisions

Corporate valuations do not strictly move upward. When macroeconomic conditions sour, consumer trends shift, or a company fails to hit its ambitious growth benchmarks, a startup may be forced to raise capital at a lower valuation than its previous funding round. This painful scenario is universally known as a "down round" 47481350.

The 2024 Market Reset and Down Round Surge

The technology startup market experienced a severe valuation correction beginning in 2022. By the first quarter of 2024, the proportion of down rounds and flat rounds hit a ten-year high, constituting a staggering 27.4 percent of all venture capital deals in the United States 135152. Beyond the immediate psychological damage to employee morale and the negative signaling to the broader market, down rounds are incredibly dangerous because they trigger latent, defensive mathematical mechanisms embedded deep within the cap table: anti-dilution provisions 47135153.

Weighted Average vs. Full Ratchet Anti-Dilution

When a startup raises money at a high valuation, early investors expect the company to grow into that price. If the company subsequently raises a down round, early investors argue that management failed to execute the business plan, and the early backers should not be penalized for severely overpaying in the prior round 14. To protect their equity stake from being brutally compressed, preferred stock contracts include anti-dilution provisions. These clauses retroactively adjust the share price the early investors paid, effectively awarding them free shares at the direct expense of the founders and employees 13531455.

The severity of this cap table adjustment depends entirely on which of two mathematical formulas is written into the corporate charter:

1. Full Ratchet Anti-Dilution (The Punitive Mechanism) Full ratchet is an aggressive, highly punitive provision that provides absolute, dollar-for-dollar price protection to the investor 5355565758. If a company raised its Series A round at ten dollars per share, and later struggles and raises a Series B round at five dollars per share, a full ratchet provision completely resets the Series A investor's historical conversion price to five dollars. Their original investment capital now converts into exactly double the number of shares 5758.

This drastic share increase occurs regardless of how small the new down round is 5556. The massive influx of newly minted preferred shares comes directly out of the common stockholders' percentages, resulting in catastrophic equity dilution for the founders 555657. Because it can effectively destroy the management team's financial incentives by wiping out their ownership stake, full ratchet provisions are considered "company unfriendly" and are rare in modern, healthy ecosystems, though they tend to resurface as coercive threats when capital markets dry up 565715.

2. Weighted Average Anti-Dilution (The Industry Standard) To provide a more balanced and equitable approach, the vast majority of professional venture capital deals utilize a weighted average anti-dilution formula 5657581661. Rather than blindly resetting the historical price to the new lowest mark, this formula calculates a blended conversion price that accounts for both the lower share price and the magnitude (the total number of shares issued) of the new down round 555657.

If the company issues only a tiny fraction of shares at a lower price to bridge a cash gap, the early investor's protected price is adjusted downward only slightly 5657. The formula ensures a proportional adjustment. Within this category, a "broad-based" weighted average is the most common and founder-friendly variant, as it factors in the company's fully diluted share count - including all unissued options - into the mathematical denominator, which softens the severity of the price adjustment 565862.

Pay-to-Play Provisions

During prolonged market downturns, lead investors may realize that a portfolio company requires a drastic capital infusion to survive. However, these lead investors generally refuse to carry the financial burden alone while earlier, passive investors free-ride on the bailout. To force collective participation, lead investors deploy coercive mechanisms known as "pay-to-play" provisions 6364.

A pay-to-play clause stipulates that existing investors must participate in a new funding round, usually requiring them to maintain their pro-rata ownership percentage. If an investor refuses or simply lacks the capital to participate, they are severely penalized 6364. Their preferred stock is forcefully converted into standard common stock. This punitive conversion strips the non-participating investor of their liquidation preferences, their anti-dilution protections, and their specialized board voting rights 6364.

While pay-to-play maneuvers are highly effective at cleaning up a messy cap table and forcing venture syndicates to financially support struggling companies, they drastically reshape the underlying equity dynamics. As penalized investors are downgraded and converted to common stock, the overall pool of common shares swells dramatically. This drives heavy secondary dilution for the founders and employees who already reside in the common stock pool 63. Following the broader market reset, the prevalence of pay-to-play provisions surged, featuring in 9.3 percent of late-stage venture agreements by late 2024 6317.

What Employees Should Know About Common Stock

While founders obsess over cap table mechanics during fundraising, early employees are often entirely in the dark regarding the true value of their equity compensation. Startups frequently attempt to recruit talent by offering large, nominal grants - such as fifty thousand shares - which sounds impressive but is mathematically meaningless without context 661819.

Vesting, Options, and the Residual Claim

To understand the value of an equity grant, an employee must know the company's fully diluted shares outstanding (FDSO) to calculate their actual percentage ownership 661819. Furthermore, employees must understand that their equity is generally issued as common stock or options to purchase common stock, which sits at the very bottom of the exit waterfall 1066. If the startup has raised multiple rounds of preferred stock with aggressive liquidation preferences, the company must be sold for an astronomically high price before the common stock has any financial value whatsoever 18.

Employee equity is also tethered to strict vesting schedules designed to ensure retention. The industry standard remains a four-year vesting period with a one-year "cliff" 6619. This means an employee earns nothing for the first twelve months of employment; upon their first anniversary, twenty-five percent of their grant vests immediately, with the remainder vesting in monthly increments over the following three years 6619. Startups issue this equity through various vehicles, primarily Incentive Stock Options (ISOs), which carry distinct tax benefits but are restricted to actual employees, or Nonqualified Stock Options (NSOs), which lack specialized tax treatment and are often used for advisors and contractors 66. Later-stage startups often transition to Restricted Stock Units (RSUs) to manage dilution 66.

Post-Termination Rights and Liquidity Events

A critical component of employee equity often buried in the fine print is the post-termination exercise period (PTEP) 18. When an employee leaves a startup, they typically have a highly restricted window - historically just ninety days - to purchase their vested options. If they cannot afford the exercise price and the associated tax burden, the options expire and return to the company's option pool 18. Because the shares remain highly illiquid until an acquisition or IPO, employees must essentially pay out of pocket to hold lottery tickets. Consequently, a minority of mature startups have begun allowing secondary market sales, permitting employees to sell vested equity to private buyers prior to a formal corporate exit 18.

Employees should also inquire about acceleration clauses. If the startup is acquired before an employee's options are fully vested, standard agreements may simply cancel the unvested portion. However, employees with leverage can negotiate for vesting acceleration - either "single-trigger" (vesting accelerates immediately upon the company's sale) or "double-trigger" (vesting accelerates if the company is sold and the employee is subsequently terminated by the acquiring entity) 1969.

Strategies for Founders to Minimize Dilution

Because dilution mathematically compounds across Seed, Series A, and Series B rounds, founders who negotiate poorly in the early stages often find themselves functionally disenfranchised by the time their company reaches maturity 18. Maintaining control of the cap table requires proactive financial defense and a deep understanding of alternative capital structures.

Venture Debt and Non-Dilutive Capital

The most direct and effective strategy to limit equity dilution is to reduce the company's reliance on priced equity rounds. Founders should aim to bootstrap early operational milestones to prove commercial traction, allowing them to command significantly higher pre-money valuations when they finally engage institutional capital 2071.

When bridging a cash flow gap is necessary, startups generating reliable, recurring revenue can increasingly turn to alternative, non-dilutive financing options, such as revenue-based financing or venture debt 1972071. While venture debt agreements often include warrants - a contractual right for the lender to purchase a small amount of equity at a later date - the resulting cap table dilution from exercised warrants is merely a fraction of what would occur during a standard equity raise 197. Crucially, debt lenders do not demand board seats, operational control, or the complex liquidation preferences that venture capitalists require 19.

Furthermore, founders must resist the vanity metric of raising massive, oversized funding rounds purely for the accompanying press coverage. Accepting fifteen million dollars when only eight million is required to reach the next milestone results in profound, unnecessary dilution 181920. Over-raising sets an aggressive, artificially inflated valuation bar that the company is mathematically forced to grow into, drastically increasing the likelihood of a punitive down round during the next fundraising cycle 1819282021.

Tightening the Option Pool and Cap Table Discipline

Founders must exercise rigorous discipline regarding the issuance of convertible securities. In early stages, startups frequently issue SAFEs and convertible notes to quickly secure capital without setting a formal valuation. However, issuing too many notes at varying discount rates and valuation caps creates an invisible debt overhang. When these instruments finally convert into equity during a priced round, the sudden, combined dilution can shock a founder who failed to model the cascading effects 1873871.

The interplay of pre-money option pools, participating preferences, and seniority stacks makes it entirely impossible to understand the true financial implications of a term sheet by simply reading the headline valuation 2528. Founders must maintain a dynamic, meticulously updated cap table and run thorough waterfall analyses. They must simulate multiple exit scenarios - ranging from distressed fire sales to billion-dollar IPOs - before signing any binding investment agreement 18353873. Only by charting the exact payout distributions across these various scenarios can a founder spot a toxic, investor-heavy cap table structure. In many cases, accepting a slightly lower pre-money valuation with "clean" terms - such as 1x non-participating preferred stock and broad-based weighted average anti-dilution - will yield millions of dollars more for the founding team upon exit than a seemingly higher valuation laden with aggressive, predatory investor protections 2528.

Bottom line

A startup's cap table transforms from a simple ledger of founder ownership into a complex hierarchy of financial rights as venture capital is injected over successive rounds. While issuing new shares organically dilutes the founders' percentage, the actual economic fallout is driven by the structural terms of preferred stock. Mechanisms like liquidation preferences, option pool shuffles, and anti-dilution protections operate beneath the surface to guarantee investor returns, meaning a high equity percentage on paper does not guarantee a proportional financial payout in a modest exit.