When to Use Venture Debt and What Current Terms Look Like

Venture debt has definitively evolved from a specialized financial lifeline into a primary, structural pillar of startup capitalization, reaching record deployment levels in 2026 as founders aggressively seek to preserve their equity. High-growth companies are currently securing massive, non-dilutive credit facilities sized at roughly thirty percent of their last equity rounds, backed by double-digit interest rates and equity warrants. However, a surging private credit default rate underscores that this capital comes attached to strict financial covenants, which are increasingly forcing sweeping layoffs and lender-mandated liquidations across the technology sector.

The Macroeconomic Shift and the Maturation of Venture Debt

For decades, the standard narrative surrounding early and growth-stage startup financing was almost exclusively focused on venture capital equity. Founders raised consecutive funding rounds - progressing from Seed to Series A, Series B, and beyond - trading increasingly larger portions of their ownership for the capital required to scale their operations. Throughout this period, debt was frequently considered a taboo subject within the startup ecosystem. It was often viewed either as a distress signal indicating that a company was struggling to attract tier-one equity investors, or simply as an irrelevant instrument for software companies that lacked physical collateral.

By 2026, that historical stigma has entirely evaporated. The global startup ecosystem has fundamentally restructured its approach to the capital stack, shifting toward a highly sophisticated blend of equity and debt 1. The era of "growth at all costs" that heavily defined the 2021 and 2022 venture boom has been definitively replaced by an era of intense capital discipline and an overarching focus on unit economics 23. In a macroeconomic environment where the cost of capital remains highly calibrated by global central banks, startup founders and chief financial officers are treating their capital structure as a deliberate, strategic choice rather than a default mechanism.

From Last Resort to Strategic Pillar

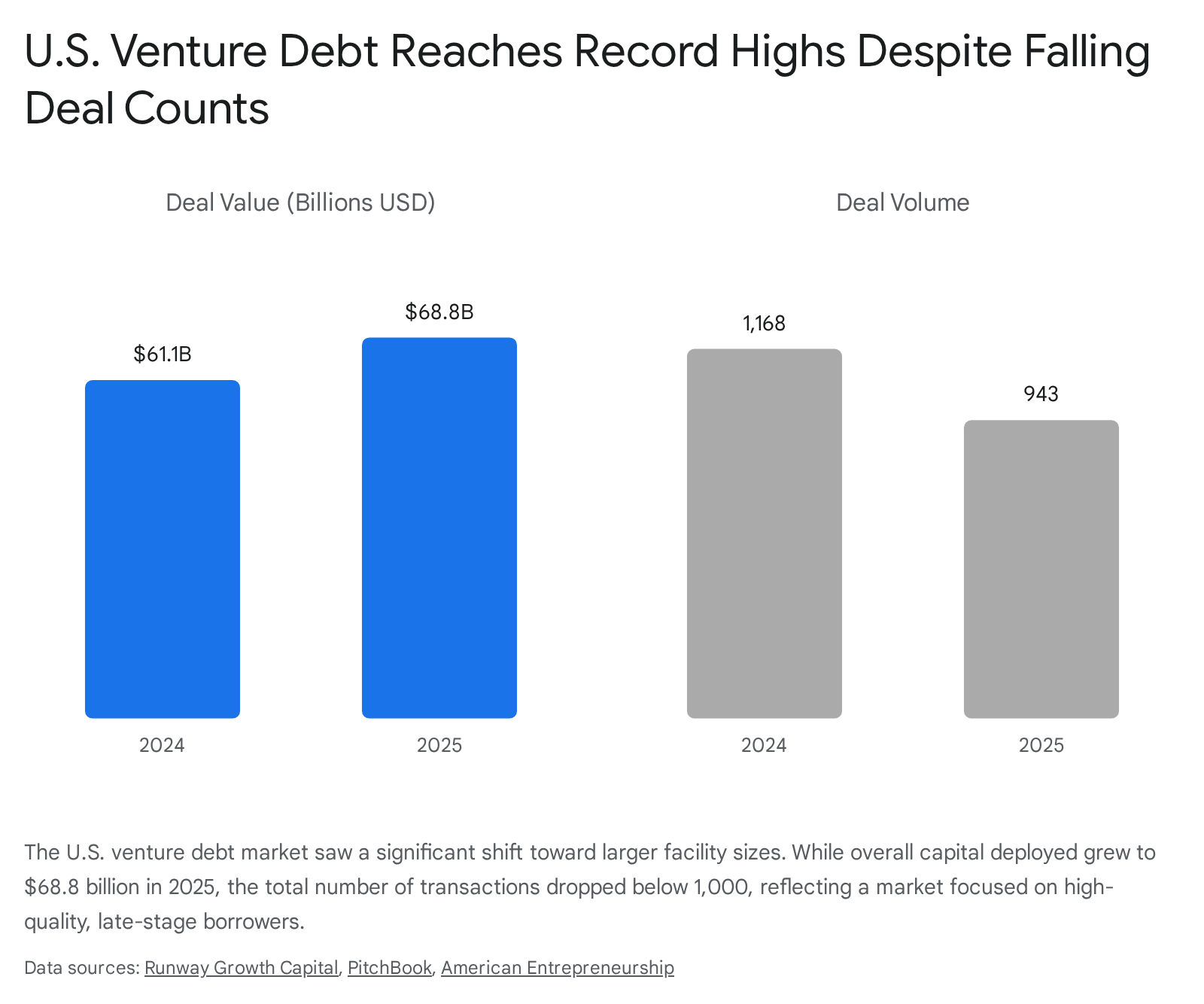

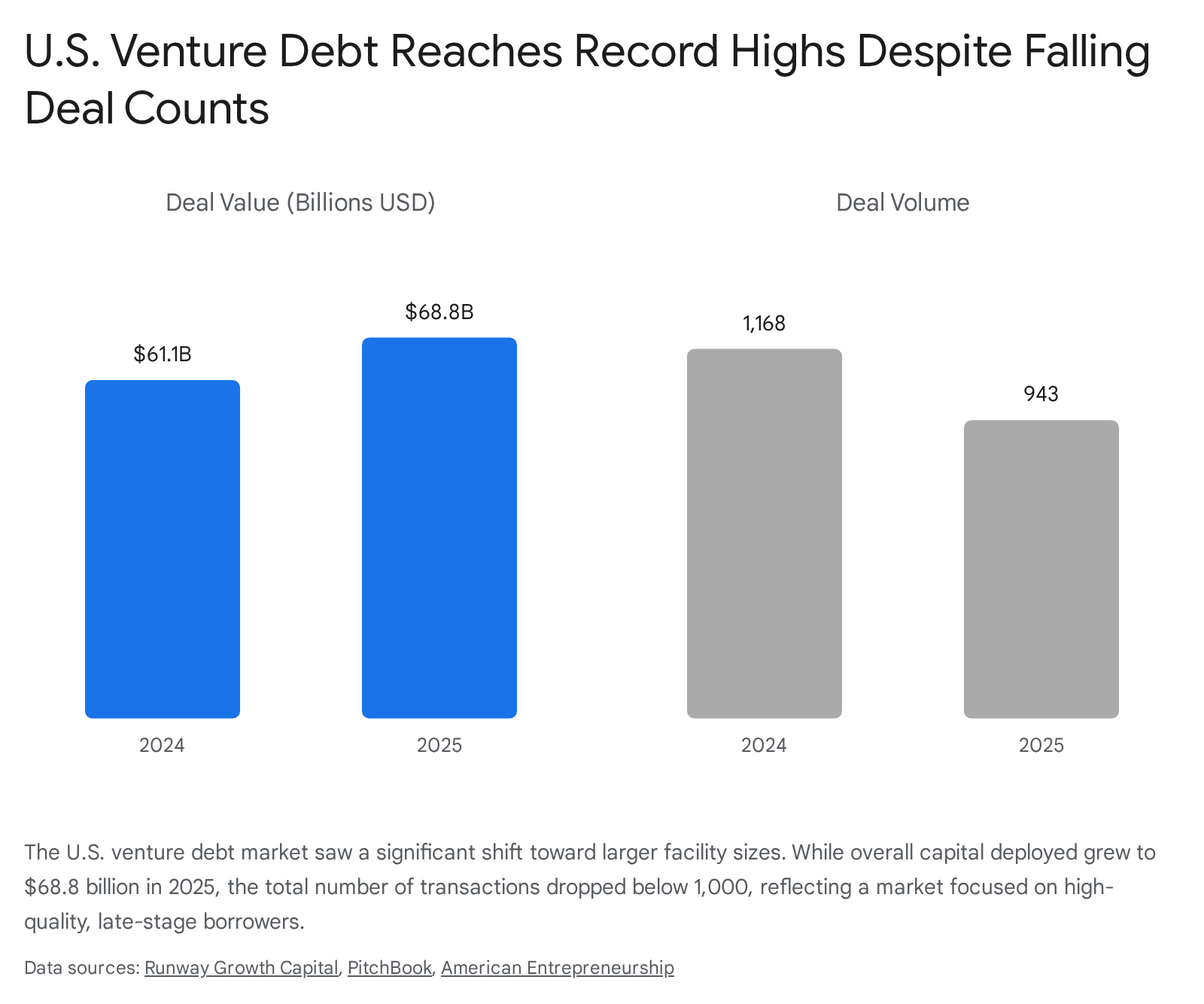

The numerical data perfectly reflects this systemic market shift. In the United States, venture debt reached a record $68.8 billion in 2025, solidifying its place as a permanent and necessary feature of the venture ecosystem 245.

Intriguingly, this record deployment volume was achieved despite the actual absolute number of debt deals shrinking. United States deal counts dropped by 19.3% - falling from 1,168 transactions in 2024 to just 943 in 2025 6.

This divergence indicates that while fewer companies are successfully securing venture debt overall, the borrowers that do qualify are taking on significantly larger, more strategic debt loads 6.

The average late-stage venture debt deal in the United States climbed to $68.2 million in the first quarter of 2026, with the median deal reaching a decade-high of $10.8 million 7. This dynamic illustrates a maturing market where lenders are concentrating their capital among the highest-quality borrowers rather than indiscriminately funding the broader startup ecosystem.

The European and Asian Market Expansion

This concentration of capital and surge in deal size is precisely mirrored in the European markets. European venture debt has demonstrated remarkable resilience amid elevated valuations and a persistently constrained initial public offering (IPO) environment, pulling in €5.9 billion in deployed capital in the first quarter of 2026 alone 89. This aggressive deployment pace positions the European debt segment to exceed its full-year 2025 total by more than 18% 8. Similar to the United States market, European deal sizes have ballooned to unprecedented levels. The average deal size in Europe reached €90.5 million in early 2026, nearly tripling the prior year's average of €35.9 million, even as the absolute deal count marked its fourth consecutive quarterly decline 89.

Simultaneously, the Asian venture debt ecosystem is maturing at a rapid pace, shedding its former reputation as a marginal financing option. This regional growth is largely driven by massive institutional players, particularly the Singaporean state-owned investment company Temasek. Temasek, often in joint ventures with major banks like United Overseas Bank (UOB) and DBS Bank, has launched several specialized regional platforms 101112.

InnoVen Capital, a joint venture between Temasek's Seviora and UOB, has established itself as the leading venture debt provider across India, China, and Southeast Asia 1013. Since its inception, InnoVen has disbursed over $900 million in loans, backing prominent Asian unicorns such as Swiggy, Byju's, and Carsome 1414. InnoVen's expansion into managing external capital via dedicated Southeast Asia and India funds signals that global limited partners are increasingly comfortable with the risk-return profile of emerging market venture debt 1415.

Another major institutional player, EvolutionX Debt Capital - a $500 million private credit joint venture between Temasek and DBS Bank - made strategic headlines throughout 2024 and 2025 by shifting its investment focus heavily toward India and Southeast Asia 1216. Citing macroeconomic concerns and sluggish growth, EvolutionX actively reallocated capital away from China, aiming to allocate up to 70% of its massive fund to India's expanding private credit market 16. In Southeast Asia, venture debt is no longer viewed as a "lender of last resort" but as an essential, sophisticated tool for accelerating the digitization of the region's economy while optimizing equity dilution for founders 1113.

The underlying driver of this global market behavior is a deep bifurcation in the broader venture capital landscape. While traditional equity markets have become highly selective, intensely disciplined, and entirely unforgiving of poor unit economics or mismanaged cash burn, private credit and venture debt markets have dramatically expanded in scale to serve high-quality, capital-efficient businesses 218. Institutional lenders are deliberately moving down-market to write larger checks, and founders are increasingly utilizing these debt vehicles to extend their cash runways, bridge internal valuation gaps, and sidestep punitive pre-IPO equity dilution 678.

Analyzing the Financing Spectrum in 2026

To understand exactly why a founder chooses to leverage venture debt in 2026, one must first thoroughly understand the structural limitations of the alternative financing methods. When a technology startup requires a significant influx of capital to scale - whether the goal is to hire elite engineering talent, aggressively expand into new international geographic markets, or build out massive physical infrastructure - the executive team generally evaluates three primary financing avenues: venture capital equity, traditional commercial bank loans, and venture debt 17.

The Cost of Venture Capital (Equity)

Venture capital involves a straightforward transaction: selling a percentage of the company's equity ownership to institutional investors in exchange for permanent capital 2018. Because early-stage startups carry an extraordinarily high failure rate, venture capitalists require a massive potential return on their successful investments to mathematically offset their losses across a broader portfolio.

The primary, undeniable advantage of venture capital equity is that it never has to be repaid 1819. If the company ultimately fails and liquidates, the investors absorb the financial loss entirely. Furthermore, top-tier venture capitalists provide much more than just cash; they offer invaluable strategic guidance, operational support, recruiting assistance, and access to lucrative corporate networks 20.

However, the true financial cost of equity is mathematically infinite and permanent 1. If a startup founder sells 20% of their company for $10 million during a Series B round, and the company later successfully exits via IPO for $1 billion, that initial $10 million cash injection ultimately cost the founders and early employees $200 million in lost upside. In 2026, as private market valuations continue to face significant downward pressure and "down-rounds" (raising capital at a lower valuation than previous rounds) become highly punitive, founders are fiercely protective of their cap tables. They are highly hesitant to price new equity rounds and suffer further dilution unless it is absolutely necessary 17.

The Limitations of Traditional Commercial Bank Loans

Traditional commercial bank loans operate on a fundamentally different paradigm. Conventional banking institutions underwrite loans based on a company's historical cash flows, demonstrated profitability, and the presence of hard, tangible collateral 1720. A conventional bank loan officer will meticulously evaluate a company's debt service coverage ratio (DSCR), which is a strict financial measure of the cash flow available to safely pay current debt obligations.

Because early and growth-stage technology startups intentionally operate at a net loss in order to aggressively capture market share, they rarely, if ever, generate the positive EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) required to pass a traditional bank's underwriting criteria 20. Furthermore, software, artificial intelligence, and broad technology companies possess very few tangible assets. Their actual enterprise value lies in proprietary intellectual property, highly complex codebases, and the promise of future recurring revenue. None of these elements satisfy a traditional commercial bank's strict hard-collateral requirements 21.

Consequently, standard commercial term loans or revolving lines of credit, despite offering highly attractive interest rates that typically range from 7% to 12% APR for qualified legacy businesses, remain largely inaccessible to modern venture-backed startups 222627.

The Venture Debt Middle Ground

Venture debt exists in the precise, highly calibrated middle ground between purely dilutive equity and inaccessible traditional debt. It is a highly specialized form of corporate lending designed specifically for high-growth, venture-backed companies that currently lack positive cash flow or significant tangible assets 1723.

Instead of underwriting a loan based on historical profitability and EBITDA, venture debt lenders underwrite based on the company's future growth trajectory, the institutional quality of its existing venture capital backers, its implied enterprise value, and its strategic pathway to future profitability 172024. The core, operating tenet of this specific asset class is that "venture debt follows venture capital" 1720. Debt lenders essentially leverage the rigorous due diligence already performed by top-tier venture capital firms as a reliable proxy for the startup's operational viability and market potential.

Crucially, venture debt is structurally designed to extend a company's cash runway - the exact amount of time it has before its bank account reaches zero - by a critical six to twelve months 17. This strategic extension provides the startup with the necessary time to achieve critical product development milestones or hit targeted revenue metrics. By reaching these milestones using debt rather than equity, the startup can subsequently raise its next round of venture capital at a significantly higher valuation, thereby minimizing the overall dilution suffered by the founders and early investors 11720.

2026 Financing Avenues Comparison

| Feature | Venture Capital (Equity) | Traditional Bank Loan | Venture Debt |

|---|---|---|---|

| Primary Underwriting Metric | Future market dominance and exit potential 20 | Historical cash flow (EBITDA), profitability, and DSCR 20 | Quality of VC backers, enterprise value, and cash runway 1720 |

| Cost of Capital | Infinite (25% to 40% IRR expected by investors) 1 | 7% to 12% APR 2627 | 10% to 13.5% APR (SOFR + Spread) 117 |

| Founder Dilution | High (Typically 15% to 20% per round) 117 | None 23 | Minimal (1% to 5% via warrant coverage) 17 |

| Repayment Obligation | None; permanent capital 1819 | Immediate fixed principal and interest monthly 20 | Interest-only period (3-12 months) followed by amortization 212225 |

| Collateral Required | None 19 | Hard assets (real estate, inventory, heavy equipment) 2022 | Blanket lien on corporate assets, often including Intellectual Property 2122 |

| Board Control | Usually requires a Board seat and voting rights 20 | None | None (though restrictive covenants apply) 2018 |

Who Uses Venture Debt and Why?

The deployment of venture debt in 2026 is highly concentrated among specific borrower profiles. It is no longer an indiscriminate capital source available to any struggling startup seeking bridge funds; it is actively reserved for companies with highly predictable software business models or those possessing massive, collateralizable hardware infrastructure needs 22026.

Artificial Intelligence and the Infrastructure Mega-Deals

The single most dominant force shaping the 2026 venture debt market is artificial intelligence. The global race to build advanced foundational AI models, alongside the physical infrastructure required to train and run them - specifically hyper-scale data centers and massive GPU clusters - is incredibly capital-intensive 6727.

Within this specific sector, venture capital equity is widely considered "too expensive" for the purpose of purchasing physical hardware infrastructure 7. As a direct result, massive AI infrastructure players are utilizing heavily structured venture debt to finance their servers and data centers. In February 2026, London-based AI hyperscaler Nscale successfully secured a massive $1.4 billion Delayed Draw Term Loan (DDTL) backed directly by GPU systems 827. The facility was carefully structured so that the debt is collateralized by the physical GPUs, and the actual capital deployment is strictly tied to executed customer contracts rather than speculative market expansion 27. This mechanism allowed Nscale to build out massive, renewable-energy-powered server clusters in Norway and Iceland without aggressively diluting its equity holders ahead of an anticipated $2 billion Series C round 82728.

Similar physical infrastructure plays dominate the United States debt market. Crusoe, an energy-first AI infrastructure provider, secured a massive $750 million credit facility from Brookfield Asset Management to accelerate the buildout of purpose-built AI data centers in Texas 629. Elon Musk's xAI secured a massive $5 billion loan from Morgan Stanley, and aerospace manufacturer SpaceX saw its debt load surge to an astonishing $23 billion as the company sought to finance capital-intensive hardware expansion without suffering further equity dilution 67.

In these unique mega-deal scenarios, lenders are not relying on traditional SaaS metrics. Instead, they rely heavily on the company's clear "path to profitability" and the immense, validated enterprise value supported by previous venture capital equity mega-rounds 7. For context on the scale of equity supporting these debt loads, OpenAI has raised approximately $186 billion in equity alongside $4 billion in debt, while Anthropic has raised roughly $69 billion in equity against $2.5 billion in debt 7.

Vertical SaaS and the Rule of 40

Outside of the multi-billion-dollar AI hardware and foundation model space, the primary, reliable consumers of standard venture debt are Software-as-a-Service (SaaS) companies 2. Specifically, Vertical SaaS - software platforms custom-built for the unique operational needs of specific niche industries like healthcare, logistics, legal compliance, or real estate - is highly favored by underwriters 3031.

Venture debt lenders inherently prefer SaaS companies because their recurring subscription business models provide highly visible, predictable revenue streams 18. In 2026, underwriters rigorously evaluate these software companies using the "Rule of 40." This financial framework states that a software company's annual revenue growth rate plus its profit margin should equal or exceed 40% 1.

A vertical SaaS company demonstrating a Rule of 40 score above the threshold, combined with strong net revenue retention, low customer churn, and a clear, modeled path to profitability, can access venture debt on highly favorable terms 1220. These companies utilize the non-dilutive capital to aggressively fund customer acquisition, marketing expansion, and product development without pricing a new equity round 1820. This model is proving highly successful; in late 2025, vertical software companies captured over 55% of the total venture capital deal share, demonstrating immense market maturity and stability 30. Healthtech and cleantech startups are also seeing strong year-over-year growth in securing debt financing, particularly across Europe where sustained policy shifts strongly support green technology infrastructure 226.

The Anatomy of a 2026 Venture Debt Term Sheet

In 2026, the specific financial terms of venture debt facilities have evolved considerably to reflect a macroeconomic climate characterized by stabilized, yet elevated, base interest rates 27. Following the aggressive series of rate hikes executed by global central banks between 2022 and 2024 to combat rising inflation, the fundamental cost of corporate borrowing has reset 2732. While venture debt is undeniably more expensive today than it was during the zero-interest-rate phenomenon of 2021, it remains a highly attractive, strategic alternative to pricing a punitive down-round in the stagnant equity markets 111.

Typically, an established startup can raise a venture debt facility equivalent to 25% to 35% of their most recent priced equity round 17. For example, if a startup successfully raises a $20 million Series B equity round, they can generally access a venture debt facility ranging from $5 million to $7 million.

Interest Rates, SOFR, and Euribor Spreads

Venture debt interest rates are almost always structured as floating rates, meaning they are explicitly tied to a baseline benchmark rate that fluctuates in tandem with the broader economy. In the United States, this benchmark is typically the Secured Overnight Financing Rate (SOFR) or the Wall Street Journal Prime Rate 17. In European markets, loans are frequently pegged to the Euro Interbank Offered Rate (Euribor), which sits around 1.9% to 2.8% depending on the specific maturity window in mid-2026 3839.

Venture debt lenders add a fixed "spread" on top of this baseline benchmark to mathematically compensate for the inherent risk of lending capital to an unprofitable startup. In 2026, a standard growth-stage venture debt facility carries a spread of 6% to 9% over the benchmark rate 17.

With SOFR hovering around 4.5% in early 2026, the total all-in interest rate generally ranges from 10% to 13.5% annually 117. Startups with higher risk profiles, shorter operating histories, or weaker venture backing may see those rates approach 15% or higher 17.

While a 13.5% APR might appear steep, it is significantly cheaper than the alternatives available to un-bankable companies. Online alternative lenders and merchant cash advances, which underwrite based purely on daily revenue rather than venture backing, frequently utilize "factor rates" ranging from 1.1 to 1.5 2640. When annualized, these factor rates can translate to an effective APR ranging anywhere from 20% to well over 50% 262733.

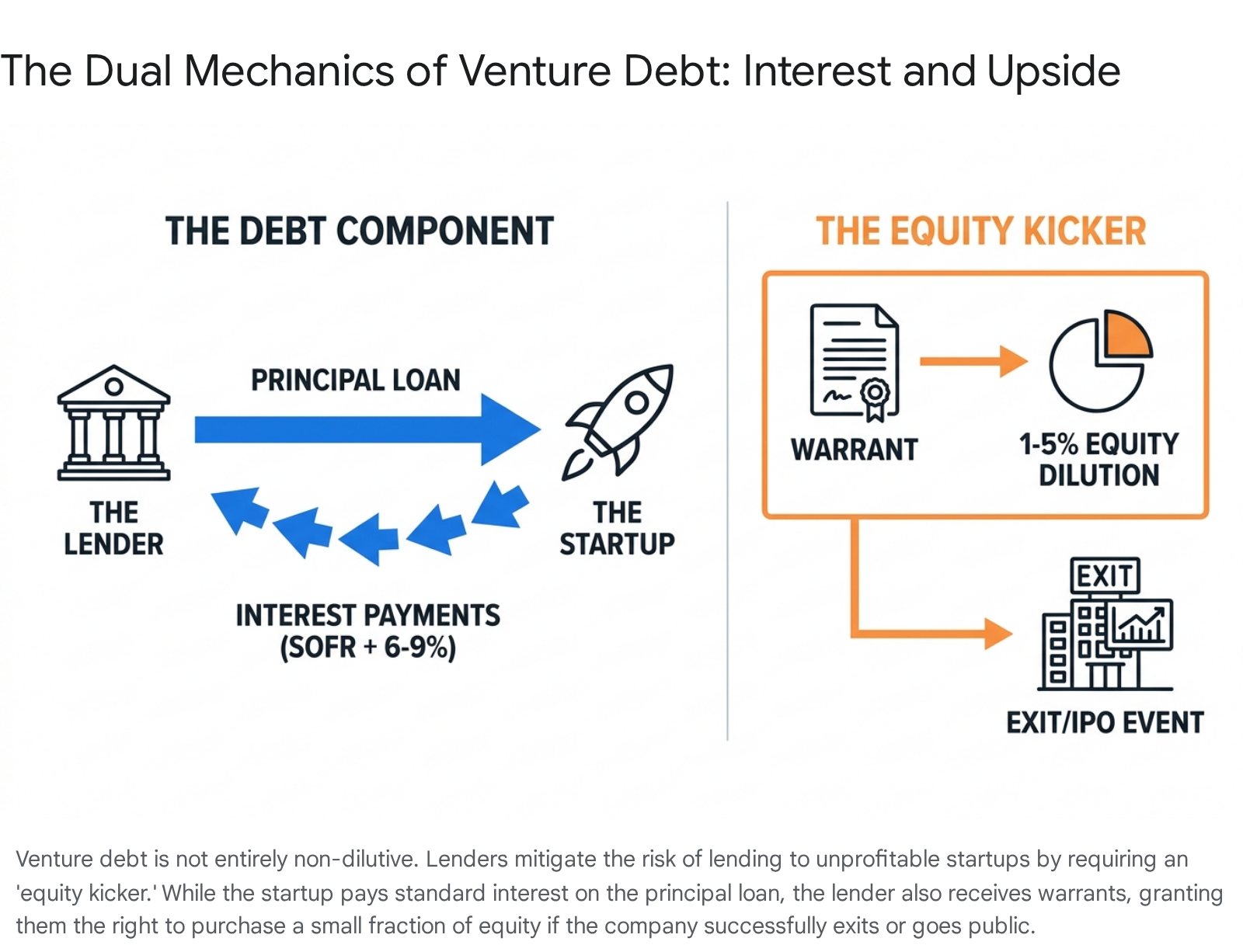

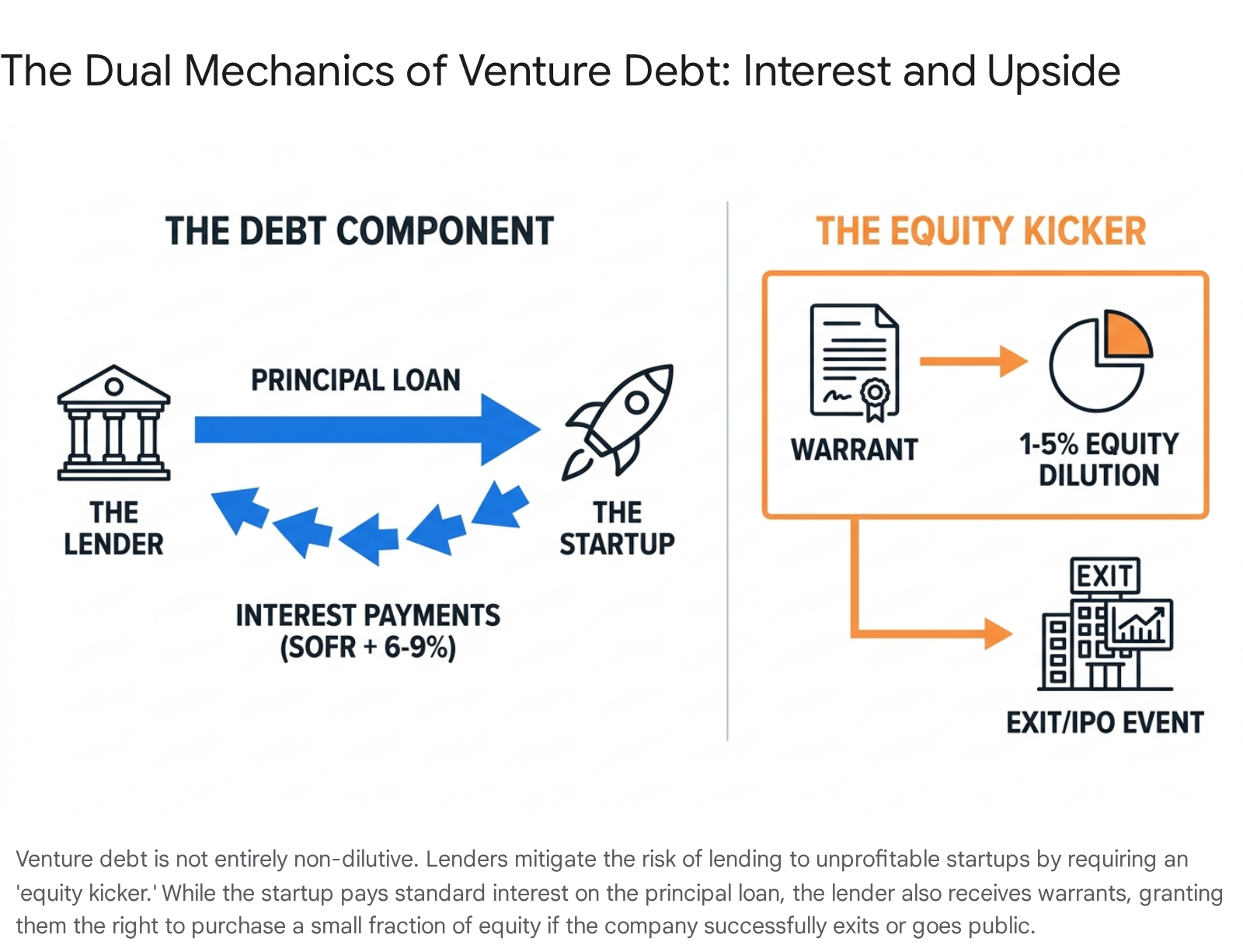

The Equity Kicker: Understanding Warrants

To effectively bridge the massive risk-reward gap inherent in lending to cash-burning startups, venture debt lenders require an "equity kicker" in the form of stock warrants 2534. A warrant is a financial derivative instrument that grants the lender the legal right to purchase a specific number of shares of the startup's stock at a predetermined price (known as the "strike price") at a later date 2223.

Warrants serve to directly align the lender's financial interests with the startup's long-term success 22. If the startup achieves a massive acquisition exit or successfully executes an IPO, the venture debt lender exercises their warrants and realizes a highly lucrative equity upside, entirely in addition to the standard interest payments collected over the life of the loan.

In 2026, standard warrant coverage in a venture debt deal requires issuing warrants equivalent to 0.1% to 1.5% of the company's fully diluted equity 1.

From the perspective of the startup founder, this is widely considered to be extremely "cheap equity" when directly compared to the devastating 15% to 20% dilution typically suffered during a standard venture capital financing round 117.

Facility Structure, Amortization, and Drawdown Periods

Because the primary, overarching goal of venture debt is to provide a startup with extended cash runway, the repayment structure of the loan is heavily tailored to the unique startup lifecycle. Traditional commercial loans begin amortization - the mandatory repayment of the core principal - immediately upon issuance 20. Venture debt, however, is typically structured over a three- to four-year term that strategically includes an initial "interest-only" period 2125.

For the first six to twelve months of the loan's life, the startup is only required to pay the accrued monthly interest, thereby preserving maximum cash flow for vital product development, marketing, and engineering hiring 2225. After this interest-only grace period expires, the loan amortizes, and the startup must begin aggressively paying down the principal alongside the interest in fixed monthly installments until the loan reaches full maturity 182021.

Furthermore, many venture debt deals are smartly structured as "drawdown facilities" or delayed draw term loans 2127. This means the startup does not have to take all of the approved cash on day one; they can draw down the funds in sequential tranches as they hit specific, pre-negotiated operational milestones, paying expensive interest only on the capital they have actually deployed 21.

The Invisible Strings: Navigating Debt Covenants

While venture debt allows founders to preserve their precious ownership stakes, it is absolutely not without strict governance and oversight. Lenders manage their downside risk through debt covenants - legally binding conditions baked directly into the loan agreement that explicitly dictate what a startup must or must not do during the life of the loan 22264344.

If a startup breaches a covenant, the lender possesses the legal authority to declare a technical default. This grants the lender the right to call the entire loan due immediately, seize intellectual property collateral, or force a total corporate restructuring 214344. In 2026, following several high-profile market failures, lenders have become highly selective and are rigorously, unapologetically enforcing these covenants 218.

Affirmative and Negative Covenants

Affirmative (or positive) covenants obligate the startup to perform specific, ongoing actions 43. These clauses are primarily designed to ensure the lender maintains deep, uninterrupted visibility into the company's financial health 44. Standard affirmative covenants in 2026 require the startup to deliver audited financial statements on a strict monthly or quarterly basis, maintain their primary operating bank accounts directly with the lending institution, and maintain adequate corporate liability and intellectual property insurance 2244.

Conversely, negative covenants restrict the startup's operational freedom and agility. They typically forbid the company from taking on additional senior debt from competing lenders, explicitly ban paying out dividends to equity shareholders, and prevent the executive team from selling off core assets, subsidiaries, or intellectual property without the lender's prior, explicit written permission 2144.

Financial Covenants and Material Adverse Change (MAC) Clauses

Financial covenants represent the most dangerous territory for early-stage companies. While venture debt agreements usually avoid the strict EBITDA or fixed charge coverage ratios (FCCR) demanded by traditional banks, they frequently include rigid liquidity and operational performance thresholds 21. A common financial covenant might dictate that the startup must maintain a minimum cash balance equivalent to three months of operating runway at all times, or that it must achieve a specific, minimum threshold of monthly recurring revenue (MRR) to unlock future funding tranches 212443.

Perhaps the most contested and legally ambiguous clause within a term sheet is the "Material Adverse Change" (MAC) provision 21. A MAC clause is a highly subjectively enforceable covenant that allows the lender to unilaterally halt future funding tranches or declare a sudden default if they believe the startup's overall financial condition, market position, or venture investor support has suffered a fundamental, negative shift 21.

The Dark Side of Debt: Defaults, Restructurings, and Layoffs

The rapid expansion of the private credit and venture debt markets over the past five years was largely marketed to limited partners - the pension funds, endowments, and institutions supplying the capital to the debt funds - as a revolutionary way to generate equity-like returns with bond-like steadiness and security 18. However, as the massive volume of loans issued during the lax diligence period of the 2021-2022 technology boom reach their maturity dates in a stubbornly high-interest-rate environment, that promised steadiness is being severely tested 1845.

Rising Default Rates in Private Credit

When easy private money meets weak business models that cannot be successfully refinanced or propped up by new equity, the inevitable result is a sharp uptick in defaults. By April 2026, the United States private credit default rate reached 6.0%, representing the highest reading since the index was created in 2024 18. Another major industry index tracking 697 senior-secured and unitranche loans noted defaults rising rapidly from 1.84% to 2.73% within a single quarter 18.

Because debt holders possess absolute repayment priority over equity holders in the capital structure, lenders legally dictate the outcome when a startup inevitably runs out of cash 45. If a company breaches its financial covenants and cannot raise an emergency equity bridge round from its existing venture capitalists, the venture debt lender will ruthlessly step in to minimize their own financial losses 45. Frequently, this results in a lender-forced fire sale or forced acquisition 45. In these grim scenarios, the lender is made whole (or partially whole) from the acquisition proceeds, while the founders, rank-and-file employees, and venture capital equity investors are wiped out entirely, receiving absolutely zero financial payout for their years of work 45.

Liquidations and Restructurings

When a fire sale to a competitor isn't possible, struggling companies are forced to liquidate entirely or attempt desperate restructurings. Some startups are currently attempting to negotiate their way out of crushing debt burdens before they hit the wall. For example, in May 2026, Genesis Holdings publicly announced it had begun direct discussions with its convertible debt holders to radically restructure the debt into long-term preferred equity 46. This move represents a desperate attempt to clean up a toxic balance sheet, drastically reduce the crushing cost of capital, and avoid formal bankruptcy proceedings 46.

Other highly-funded startups simply collapse under the weight of their debt service. A prime example from 2026 is Picnic, a Seattle-based food automation startup that raised over $50 million in venture capital to build complex pizza-making robotics 353637. Despite partnering with massive global brands like Domino's Pizza and securing financial backing from prominent investors including Vulcan Capital, the company struggled severely with high hardware manufacturing costs, slow restaurant industry adoption, and an inability to raise further equity in a highly disciplined market 353637.

Unable to pay its mounting debts or service its loans, Picnic was forced to shut down entirely 35. Rather than filing for a standard Chapter 7 bankruptcy, the company executed a "General Assignment for the Benefit of Creditors" (ABC) in May 2026 3536. This specific state-level legal mechanism allows an insolvent company to hand over all its remaining physical assets and intellectual property to a third-party liquidator (in this case, CMBG Advisors), who then sells off the assets outside of the formal bankruptcy court system to pay back the secured creditors 3637.

Similar fates have befallen consumer brands. Foxtrot, a venture-backed upscale convenience store chain that raised over $100 million in VC funding to fuel rapid expansion, abruptly closed all its locations nationwide 38. Unable to manage its debt and unpaid vendor bills following a rapid period of over-expansion, the company held a virtual liquidation auction, leaving employees without notice and resulting in lawsuits for violating the WARN Act 38. These failures highlight the severe, existential risks of taking on debt for hardware-heavy or physically expansive business models that lack proven, immediate scalability and positive unit economics 3738.

Covenant Breaches and the 2026 Tech Layoff Contagion

The immense pressure of servicing expensive venture debt and remaining compliant with strict financial covenants is a major, often unspoken, contributing factor to the rolling wave of technology layoffs witnessed throughout 2026 3940. When a startup is at imminent risk of breaching a minimum cash-on-hand covenant or a profitability threshold, the executive team's immediate, required recourse is to slash operating expenses to dramatically lower their cash burn rate 1741. The fastest, most effective way to cut operating expenses is to eliminate headcount.

Throughout the first half of 2026, major workforce reductions have rippled across the sector, impacting tens of thousands of workers. Intuit laid off 17% of its global workforce - roughly 3,000 employees - in an effort to streamline operations and aggressively fund new AI initiatives 3954. Website builder Wix cut 1,000 roles (20% of its staff) to adapt to the soaring computing costs of the AI era and improve lagging profitability metrics 3942. Hardware giant Dell shed roughly 11,000 employees (10% of its workforce) in a structural shift toward its AI server business 54. Financial technology firms were hit equally hard; Block laid off 40% of its workforce (4,000 employees), and Coinbase cut 14% of its global staff, with both CEOs citing the need to operate more efficiently utilizing AI tools 5442. Cisco eliminated 4,000 jobs to pivot toward high-growth security sectors 54.

While "AI pivoting" and "efficiency" serve as the publicly stated rationales for the vast majority of these deep cuts, the underlying financial reality is much more pragmatic. Preserving capital to maintain clean balance sheets, appease lenders, and avoid catastrophic debt defaults is a paramount, existential concern for CFOs navigating a high-interest-rate environment where emergency equity is no longer freely available 453954.

Bottom line

In 2026, venture debt has firmly cemented itself as a core, indispensable component of the startup capital stack. It offers high-growth companies a vital mechanism to extend their cash runway and avoid the brutal, permanent cost of equity dilution in a constrained market. Propelled primarily by highly capital-intensive AI infrastructure build-outs and the highly predictable, recurring revenues of vertical SaaS platforms, the debt market is deploying massive, record-breaking checks despite overall transaction volumes shrinking. However, the sharp rise in private credit defaults, lender-forced liquidations, and sweeping tech layoffs serves as a stark reminder that this capital is absolutely not risk-free. Founders must carefully navigate elevated interest rates and stringently enforced financial covenants, recognizing that while venture debt expertly preserves upside equity, it fundamentally and permanently lowers a startup's margin for operational error.