What a $20M Post-Money SAFE Means for Founders

Raising capital on a $20 million post-money SAFE means an investor is mathematically guaranteed a fixed percentage of a startup's equity prior to a priced round, regardless of how many subsequent SAFEs the company issues. Because this financial structure shifts the entire dilution burden of future convertible rounds and employee option pools onto the founders, it requires meticulous cap table modeling. While it offers rapid, high-resolution fundraising for early-stage companies, founders must balance execution speed against the severe risk of arriving at their Series A with a depleted ownership stake.

The Macro Venture Capital Landscape in 2026

To understand why a $20 million post-money valuation cap is a critical benchmark today, it is necessary to examine the broader macroeconomic realities of venture capital in 2026. After several years of market resets, liquidity crunches, and shifting interest rate paradigms, the venture capital ecosystem has returned to record-breaking top-line numbers 12. However, that capital is distributed more unevenly than at any point in the modern era of startup financing.

In the first quarter of 2026, United States venture deal value reached $267.2 billion, a figure that exceeded nearly every full-year total in history with the exception of the 2021 and 2025 mega-cycles 234. While this top-line number suggests a booming market, a deeper dive into the data reveals a profoundly bifurcated ecosystem. A staggering 73.2% of that first-quarter deal value was concentrated in just five massive transactions, which included unprecedented funding rounds for artificial intelligence laboratories like OpenAI and Anthropic, alongside aerospace giants like SpaceX 23. When those top five deals are removed from the equation, the remaining venture market continues to look remarkably constrained, highly selective, and fundamentally similar to the tightened liquidity environment of 2024 and 2025 24.

Artificial intelligence commands an absolute premium across all stages of venture capital. AI startups accounted for roughly 40% of the entire venture market's deal count and an astonishing 65.4% of total annual deal value by the end of 2025 56. The AI premium is quantified explicitly in early-stage valuations. At the Series A level, the median AI startup valuation was recently recorded at 38% higher than non-AI counterparts, a gap that widens to an enormous 193% premium by Series E and beyond 1. For founders building outside of the AI ecosystem, capital is available but significantly more expensive in terms of equity given up.

As a result, median deal sizes and valuation metrics show a widening divergence between the "haves" and "have-nots." By the fourth quarter of 2025, the median post-money valuation for seed rounds hit an all-time high of $24 million, a sharp increase from $18 million a year prior 7. However, this median is heavily skewed by premium deals. For standard pre-seed and seed companies raising on Simple Agreements for Future Equity (SAFEs), valuation caps traditionally hover between $10 million and $15 million 8. Therefore, successfully negotiating a $20 million post-money valuation cap on a SAFE signals that a startup possesses exceptional early traction, a highly legible and pedigreed founding team, or operates in a heavily favored sector like foundational artificial intelligence 89.

| Venture Stage Metric (Q1 2026 vs. Recent History) | AI Startups | Non-AI Startups | Market Average / Median |

|---|---|---|---|

| Median Seed Post-Money Valuation | ~$28.8M (Estimated Premium) | ~$10M - $15M | $24M (Q4 2025 High) |

| Median Series A Pre-Money Valuation | Premium +38% | Baseline | $62M |

| Median Series A Deal Size | Heavily Skewed Upward | Baseline | $19.6M |

| Average Series A Deal Size | Heavily Skewed Upward | Baseline | $39.6M |

Data aggregated from 2025 and 2026 venture market reports published by Carta, PitchBook, and Fenwick & West 1478. The massive gap between median and average Series A deal sizes illustrates the extreme market concentration at the top.

Decoding the SAFE: Pre-Money Versus Post-Money Mechanics

The Simple Agreement for Future Equity (SAFE) was introduced by the startup accelerator Y Combinator in late 2013 to streamline early-stage fundraising 1011. Prior to the SAFE, early-stage startups primarily relied on convertible debt notes, which required negotiating interest rates, maturity dates, and complex repayment terms 1112. The SAFE stripped away these debt-like features, creating a simple, fast, and highly standardized contract where an investor provides capital in exchange for the right to receive equity during a future qualifying financing event, typically a Series A priced round 1213.

Today, the SAFE is the undisputed king of early-stage financing. In the first quarter of 2025, SAFEs comprised a record high of 90% of all pre-seed rounds on the Carta equity management platform, with traditional convertible notes shrinking to single-digit market share 1215. However, one of the most critical and frequently misunderstood aspects of modern startup finance is the mathematical distinction between a "pre-money" SAFE and a "post-money" SAFE.

The Legacy of the Pre-Money SAFE

When the SAFE was first introduced, it operated on a pre-money basis. In a pre-money SAFE, the valuation cap applied to the company's capitalization before accounting for the shares issued to the SAFE investors themselves 1516.

The primary consequence of this structure was that dilution was a shared burden. If a founder raised money from Angel Investor A, and six months later raised more money from Angel Investor B, the issuance of Investor B's shares would proportionally dilute the founders, the employee option pool, and Investor A 1217. Because every new pre-money SAFE diluted all prior SAFE holders, no one - neither the founders nor the investors - could calculate exactly what percentage of the company they actually owned until the Series A priced round formally closed and all the math was tabulated simultaneously 1516. This lack of clarity created immense friction, leading to surprised and frustrated investors who found their ownership stakes lower than anticipated.

The Rise of the Post-Money Standard

To solve this transparency problem, Y Combinator released a completely overhauled version of the document in 2018: the post-money SAFE 10. By 2024, more than 83% of all SAFEs utilized this post-money structure, establishing it as the absolute default for early-stage capital 16.

The post-money SAFE fundamentally rewrote the economics of early-stage dilution. In this structure, the valuation cap explicitly includes the capital raised in the SAFE itself. This means that the investor's ownership percentage is locked in the moment the document is signed 1718. The mathematical formula is simple and absolute: the investor's guaranteed ownership percentage equals their investment amount divided by the post-money valuation cap 1719.

If an investor writes a $1 million check on a $20 million post-money valuation cap, they are mathematically guaranteed 5% of the company's fully diluted capitalization at the time of conversion. That 5% is a floor. If the startup goes on to raise another $4 million in subsequent SAFEs, that original investor still owns their 5% 1217.

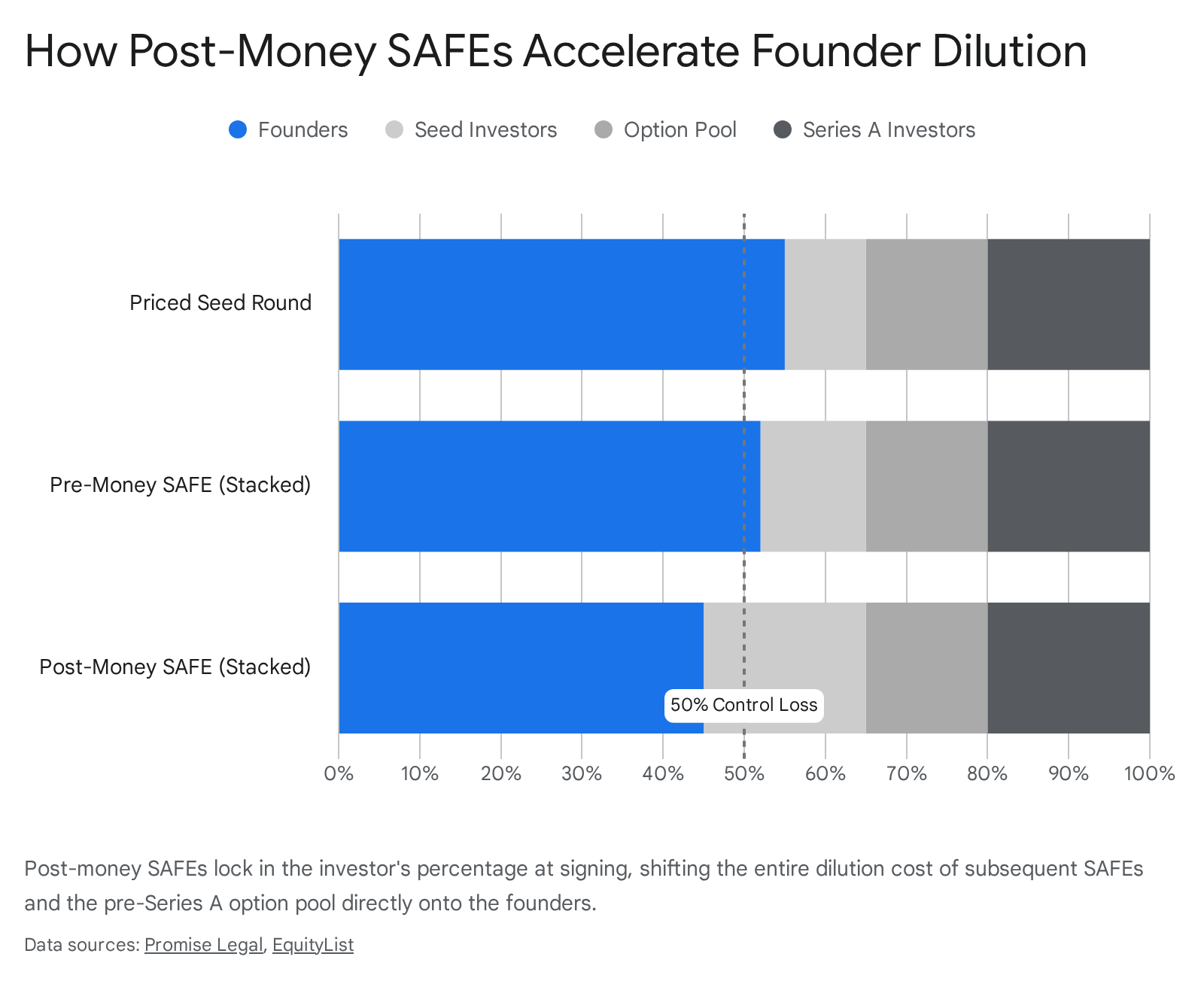

Because the investors are structurally protected from diluting each other, the entirety of the dilution burden from subsequent SAFEs falls directly and exclusively on the founders 1718. This subtle architectural change transformed the SAFE from a founder-friendly instrument of shared risk into an investor-friendly instrument of absolute certainty.

The SAFE Stacking Trap and the Post-Money Illusion

The certainty of the post-money SAFE creates a dangerous dynamic for founders who raise capital piecemeal over extended periods, a phenomenon widely known as the "SAFE stacking trap" 1913.

Because SAFEs do not require a lead investor to price the round, do not require a board seat allocation, and incur virtually zero legal fees, founders are often tempted to accept capital on a rolling basis whenever investor interest arises 212223. A founder might raise an initial $1 million on a $10 million post-money cap to get the business off the ground. A year later, having achieved some product-market fit, they might raise another $2 million on a $20 million post-money cap.

To the founder, the doubling of the valuation cap from $10 million to $20 million feels like a massive victory, signaling that the company is appreciating in value. This is the "post-money illusion" 19. In reality, the rising cap does not erase or mitigate the ownership promises already made. The promises simply stack on top of each other.

In the scenario above, the first tranche sold 10% of the company ($1M / $10M). The second tranche sold another 10% of the company ($2M / $20M). Before any institutional venture capital firm has even looked at the company for a Series A, the founders have quietly given away 20% of their equity 1719.

Founders frequently fail to model this cumulative dilution because the SAFE capital does not physically convert into shares of stock on the company's cap table until the priced round is triggered 1314. The dilution remains hidden in contractual promises, allowing founders to operate under the assumption that they still own 90% to 100% of their startup. It is only when the lead Series A investor's legal counsel builds the fully diluted pro forma cap table that the founders realize the sheer volume of equity they have irrevocably sold 1913.

The Hidden Tax of the Option Pool Refresh

The dilution from stacked SAFEs is severely compounded by the mechanics of the employee stock option pool. To attract top talent, technology startups must grant equity. Institutional investors require a robust pool of unallocated options to be available for future hires to ensure the company can scale without returning to the investors for more equity 2526.

During a Series A priced round, lead investors will almost universally demand that the company establish or refresh an option pool equal to 10% to 20% of the fully diluted, post-money capitalization 2627. Crucially, investors demand that this pool be created in the pre-money capitalization of the Series A 2627.

This means that the new Series A investors do not suffer any dilution from the creation of the option pool. Because post-money SAFE investors have their percentages mathematically locked prior to the new money entering, they also do not suffer dilution from the option pool creation 17. The entire 10% to 20% chunk of equity required to fund the employee option pool is carved directly out of the founders' remaining equity 2226.

When combining stacked post-money SAFEs with a pre-money option pool refresh, the math becomes highly punitive. It is increasingly common in 2026 for founders to enter their Series A negotiations thinking they own a majority of their business, only to sign the final documents and realize their ownership has been compressed to between 35% and 40% before the business has even reached its growth stage 1415.

The Y Combinator Ecosystem and the 2026 Standard Deal

The dynamics of SAFE dilution cannot be fully understood without examining the role of Y Combinator, the world's premier startup accelerator and the original architect of the SAFE. For over a decade, Y Combinator has dictated the market standards for early-stage financing, and their deal terms serve as the baseline against which almost all other pre-seed and seed investments are measured 1016.

As of 2026, Y Combinator provides a standard, non-negotiable deal to every company accepted into its cohorts. The accelerator invests a total of $500,000, but the capital is strategically bifurcated into two distinct SAFE instruments issued simultaneously 17.

- The Fixed Equity SAFE: Y Combinator invests $125,000 on a standard post-money SAFE in return for a fixed 7% equity stake in the company 17. Mathematically, this implies a post-money valuation of roughly $1.78 million for the very earliest stage of the business. This straightforward equity component is designed to minimize negotiation overhead, granting the accelerator its baseline ownership 16.

- The Uncapped MFN SAFE: The remaining $375,000 is invested via a SAFE that features no valuation cap and no discount rate, but includes a powerful Most Favored Nation (MFN) provision 17.

The Uncapped MFN SAFE is where the mechanics of a $20 million valuation cap come into sharp focus. An MFN clause stipulates that whenever the startup raises its next round of SAFE financing, the terms of Y Combinator's $375,000 investment will automatically adopt the most favorable terms given to any new incoming investor 1617. This mechanism ensures that Y Combinator is perpetually protected from being diluted by overly founder-friendly terms negotiated later in the company's lifecycle.

For example, if a Y Combinator founder graduates from the program and successfully raises a seed round entirely on a $20 million post-money valuation cap, the MFN provision activates. Y Combinator's $375,000 SAFE automatically converts as if it were invested at that $20 million cap, granting the accelerator an additional 1.875% of the company ($375,000 divided by $20,000,000) 17. When combined with their initial 7% stake, Y Combinator will own 8.875% of the fully diluted cap table going into the Series A, entirely insulated from the dilution that the founders will absorb from other investors 17.

Jurisdictional Gatekeeping and Corporate Structure

In January 2026, Y Combinator introduced a significant change to its standard deal terms that sent ripples through the global startup ecosystem. The accelerator updated its policy to restrict eligible investment jurisdictions exclusively to the United States, the Cayman Islands, and Singapore 18.

For international founders, particularly those operating in robust tech hubs like Canada or the United Kingdom, the practical impact is immediate and structurally profound. While international teams can still apply and participate in the accelerator, any startup incorporated in an unapproved jurisdiction must establish a parent holding company in the US, Cayman Islands, or Singapore before Y Combinator will deploy the $500,000 investment 18.

This policy shift moves complex corporate incorporation decisions, often involving expensive tax structuring and intellectual property transfers, to the very beginning of the startup lifecycle, long before product-market fit is established 18. Y Combinator's decision highlights how early-stage capital increasingly demands standardized legal structures optimized for speed, repeatability, and predictable SAFE conversions under established corporate law frameworks like the Delaware General Corporation Law 18.

Insights from the Y Combinator Winter 2026 Batch

The companies navigating these terms reflect a rapidly evolving founder demographic. Analysis of the 196 to 199 companies in the Y Combinator Winter 2026 batch reveals a sharp pivot toward deep-tech and highly technical artificial intelligence research 1933.

Under its current leadership, the accelerator has moved away from traditional B2B SaaS models and consumer apps. The 2026 cohort features 20 hardware startups - building robotics, space hardware, and biotechnology - and three dedicated Artificial General Intelligence (AGI) laboratories 33. The founder profile has also shifted; the average founder in the W26 batch has 5.8 years of professional experience, a significant drop from the historical average of roughly nine years 33. AI agent founders are even younger, with a median of 4.8 years of experience, suggesting a massive influx of technical talent moving directly from universities or brief stints at leading aerospace and tech firms directly into entrepreneurship 33.

Furthermore, 11% of the W26 batch is comprised of solo founders, highlighting how the barrier to entry for building complex software has been lowered by AI coding assistants, allowing single individuals to achieve traction that previously required teams 33. Traction among these top-tier startups is staggering; one batch company, Pocket, achieved $27 million in annualized recurring revenue (ARR) while still technically at the seed stage, illustrating the massive financial velocity driving the demand for high valuation caps 19.

When to Transition from SAFEs to Priced Equity Rounds

Given the immense dilution risks associated with stacking post-money SAFEs, founders must carefully evaluate when to abandon convertible instruments in favor of a traditional priced equity round. While SAFEs dominate the pre-seed ecosystem, industry data clearly delineates a breakpoint where priced rounds become the standard.

According to 2025 and 2026 cap table data from Carta, the majority of early-stage funding rounds under $3 million are executed via SAFEs 922. Between $3 million and $4 million, the market is roughly split evenly between SAFEs and priced equity. However, once a startup raises more than $4 million in a single financing event, priced rounds decisively dominate the landscape 914.

This transition is driven by the mechanical realities of venture capital. When a lead investor writes a check of $2 million or more, they are no longer willing to take dilution risk on future option pool creations or the unpredictable math of stacked SAFEs 922. Institutional investors writing large checks demand absolute clarity on their ownership percentage, alongside formal governance rights, board seats, and protective provisions that a SAFE legally cannot provide 1415.

| Round Size Benchmark | Dominant Instrument | Rationale for Structure |

|---|---|---|

| Under $1 Million | Post-Money SAFE | Maximizes speed; minimizes legal fees ($0 to $5k); delays valuation debates 20. |

| $1 Million to $3 Million | Mixed (SAFE preferred) | Still efficient, but dilution tracking becomes critical. Founders must rigorously model caps 20. |

| $3 Million to $4 Million | Transitional Zone | Lead investors begin demanding priced rounds for governance, though highly competitive deals may still use SAFEs 9. |

| Over $4 Million | Priced Preferred Equity | Lead investors demand board seats, protective provisions, and absolute cap table clarity. Option pool is formally established 922. |

For founders, a priced round is generally more advantageous once they have a committed lead investor willing to set fair terms. While a priced round incurs significant legal costs - typically ranging from $10,000 to $30,000 at the seed stage - it provides a crucial reset for the company 2122. A priced round consolidates all outstanding SAFEs, converts them into defined shares of preferred stock, formally creates the employee option pool, and cleans up the capitalization table, providing a stable foundation for future growth 2214. Relying on SAFEs when a lead investor is willing to price the round is a strategic error that trades long-term equity control for short-term convenience 15.

Legal and Bankruptcy Recharacterization: The Rhodium Precedent

The assumption that SAFEs are merely "equity in waiting" was severely challenged by the legal system in 2025. Because SAFEs lack maturity dates, interest rates, and regular repayment schedules, founders and many investors historically treated them as effectively identical to common stock in worst-case scenarios 21. If a startup failed, the conventional wisdom held that SAFE investors would lose their money right alongside the founders.

However, a landmark decision by a Delaware bankruptcy court in August 2025 fundamentally altered the legal interpretation of these instruments in distressed scenarios. In the Chapter 11 bankruptcy case of In re Rhodium Encore LLC, the court addressed an issue of first impression regarding the liquidation priority of SAFE holders 2122.

The debtors in the case argued that SAFEs were contingent equity instruments, meaning the investors had no claim to the company's remaining assets 22. The SAFE investors countered that the specific contractual language inside the standard SAFE agreement obligated the company to repay their original investment upon certain triggering events, such as a dissolution or a liquidity event 22.

Applying Delaware contract law, the bankruptcy court sided entirely with the investors. The court ruled that the cash-out provisions contained within the SAFE created an enforceable "contingent claim" under the US Bankruptcy Code 22. Crucially, the court established that this claim placed SAFE investors senior to common stockholders in the liquidation hierarchy, though still junior to general unsecured creditors and traditional debt 2122.

For founders, the Rhodium Encore precedent carries profound implications. It establishes that in a distressed asset sale, merger, or wind-down, SAFE investors are legally entitled to claw back their original investment capital from whatever assets remain before the founders receive a single dollar 22. This judicial interpretation underscores that while SAFEs behave like equity during periods of hyper-growth, they bare sharp teeth resembling debt during periods of failure.

Tax Complexities and IRS Scrutiny of the SAFE

The hybrid nature of the SAFE also creates intense friction with global tax authorities, particularly the United States Internal Revenue Service (IRS). From a corporate tax perspective, companies often prefer instruments to be classified as debt so they can deduct interest payments, while tax authorities seek to recharacterize artificial debt as equity to prevent aggressive earnings stripping 2324.

Under IRS Section 385, the determination of whether a financial instrument is debt or equity relies on a multifactor common-law analysis 2526. The courts and the IRS look for the presence of a fixed maturity date, an arm's-length commercial interest rate, an unconditional obligation to repay a sum certain, and creditor rights upon default 2527.

Because the standard SAFE intentionally lacks a maturity date, accrues no interest, and offers no absolute guarantee of repayment unless a specific trigger event occurs, it spectacularly fails the common law test for debt 1327. Consequently, the IRS and major tax advisory firms generally agree that a SAFE cannot be treated as a debt instrument for federal tax purposes 2742.

Instead, SAFEs are typically characterized by tax professionals as either variable prepaid forward contracts or equity derivatives 4243. Under this classification, the investor has not actually purchased stock; they have purchased a contractual right to receive stock in the future.

The QSBS Timing Problem

This tax characterization creates a massive potential pitfall for angel investors and venture capitalists regarding the Qualified Small Business Stock (QSBS) exemption. Under US Section 1202, investors who hold qualified startup stock for at least five years can exclude up to 100% of their capital gains from federal taxation, a benefit that can save millions of dollars upon a successful exit 43.

However, because a SAFE is considered a derivative contract rather than actual stock, the critical five-year QSBS holding period clock generally does not begin ticking on the day the investor signs the SAFE and wires the money. The clock only begins when the SAFE officially converts into priced equity during a Series A or similar qualifying event 4243. If a founder relies on SAFEs for three years before finally pricing a round, their earliest backers will be forced to wait an agonizing eight years from their initial investment before their equity qualifies for tax-free treatment.

Global Variations: How International Markets Adapt the SAFE

While the Y Combinator SAFE was drafted specifically against Delaware corporate law, its immense popularity has forced international startup ecosystems to adapt the instrument to fit distinct local regulatory and tax environments. Founders operating outside the United States must navigate these localized variations carefully.

The UK Advance Subscription Agreement (ASA)

In the United Kingdom, classic US-style SAFEs are highly problematic for early-stage investors because they generally do not qualify for the Seed Enterprise Investment Scheme (SEIS) or the Enterprise Investment Scheme (EIS) 44. These government schemes provide massive tax reliefs to angel investors, and their absence can kill a fundraising round. To comply with His Majesty's Revenue and Customs (HMRC) regulations, UK startups use an Advance Subscription Agreement (ASA) 44. Unlike a SAFE, which is a contingent right, an ASA is legally treated as a genuine prepayment for shares. To maintain SEIS/EIS eligibility, an ASA must convert to equity within a strict timeframe (typically six months) and cannot feature any investor-friendly debt-like protections 44.

The Indian iSAFE and CCPS

In India, the regulatory environment strictly prohibits companies from issuing open-ended contingent equity instruments. Under the Companies Act and foreign exchange regulations, private placements must be made through defined, recognized securities 45. To replicate the commercial logic of the SAFE, the Indian ecosystem developed the "iSAFE," which mathematically mimics a SAFE but is legally structured as Compulsorily Convertible Preference Shares (CCPS) 45. Crucially, because CCPS can only be issued by incorporated companies, Indian startups operating as Limited Liability Partnerships (LLPs) cannot use the iSAFE and must convert to a private limited company before raising capital 45.

The Irish Preference for Convertible Loan Notes (CLNs)

In Ireland, while the SAFE has gained traction among angel investors, traditional convertible loan notes (CLNs) remain deeply entrenched, particularly when dealing with state-backed enterprise boards or traditional lenders 1346. Irish CLNs operate as true debt, carrying 4% to 8% interest rates and strict 18-to-36-month maturity dates 46. While Irish SAFEs exist - drafted specifically against the Companies Act 2014 to include mandatory pre-emption and board approval clauses - founders must often negotiate heavily to convince risk-averse local investors to abandon the downside protection of a maturity-dated CLN in favor of the open-ended SAFE 46.

The Liquidity Squeeze and 2026 M&A Outlook

The fierce negotiation over a $20 million valuation cap is ultimately meaningless if the startup cannot eventually provide a liquidity event for its investors. Despite the top-line deal value numbers in Q1 2026, the reality of the exit market remains grim for the vast majority of venture-backed companies.

Exit value hit $347.3 billion in the first quarter, representing the highest quarter on record, but this metric is a statistical mirage 24. The total was almost entirely driven by preparations for historic mega-IPOs from SpaceX, OpenAI, and Anthropic, which combined could generate nearly $2.5 trillion in exit value - more than all venture-backed IPOs in this century combined 23. For the remaining 60,000 private venture-backed companies, liquidity is agonizingly tight 25.

The median venture capital Internal Rate of Return (IRR) for North American fund vintages since 2019 remains mired in the single digits, and the median distribution to paid-in (DPI) multiple for the past decade's vintages is still below 1x 23. This means that limited partners (LPs) - the endowments and pension funds that back the venture capitalists - are not getting their money back, making them increasingly hesitant to fund new venture vehicles 46.

As the IPO window remains selectively narrow due to geopolitical volatility and high interest rates, the venture secondaries market has emerged as a critical relief valve. Dry powder for VC secondaries has more than doubled since 2022, reaching near $10 billion, as institutional buyers step in to purchase preferred stock from early investors and employees seeking liquidity 2829. However, this secondary market is ruthlessly quality-driven, concentrating almost exclusively on top-tier breakout companies and offering steep discounts for mid-tier performers 2930.

Bottom line

A $20 million post-money SAFE provides founders with rapid access to capital at a premium valuation, but it demands an acute understanding of how cumulative dilution functions in modern venture finance. Because post-money structures guarantee investor ownership percentages, founders absorb the entirety of the dilution from subsequent funding rounds and employee option pools, frequently resulting in a loss of majority control before reaching a Series A. While the SAFE avoids the legal complexities of traditional debt, emerging bankruptcy precedents and global tax frameworks ensure that founders bear significant structural risks if they delay transitioning to a priced equity round.