What the Data Says About Full-Time Swing Trading

Trading full-time is an exceptionally challenging endeavor that is statistically unlikely to replace a steady salary for the vast majority of individuals. While swing trading offers slightly better survival rates and lower transaction friction than intraday day trading, the combination of aggressive tax drag, institutional competition, and the loss of employer-subsidized benefits makes consistent profitability a rarity. Prospective traders must evaluate this path as a highly competitive, capital-intensive small business rather than a guaranteed route to geographical or financial independence.

The Allure Versus the Statistical Reality

The internet is saturated with the promise of geographical and financial freedom unlocked by a laptop and a brokerage account. However, when stripping away the stylized social media imagery and analyzing peer-reviewed academic research alongside mandated regulatory disclosures, the reality of retail trading is sobering. The financial markets function as a highly efficient mechanism for transferring wealth from inexperienced retail participants to heavily capitalized institutional entities, and the barrier to long-term survival for an individual trader is incredibly high.

Regardless of the financial instrument - whether equities, foreign exchange (forex), contracts for difference (CFDs), or derivatives - retail trader failure rates are remarkably consistent globally. Multiple independent regulatory bodies and academic institutions place the failure rate of active retail traders between 70% and 97% 12. To understand whether a retail investor can successfully quit their primary career to trade, one must first understand the structural forces arrayed against them.

Regulatory Evidence of Retail Wealth Destruction

A comprehensive study published in 2024 by the Securities and Exchange Board of India (SEBI) provided an unprecedented, multi-year look at retail outcomes in the equity derivatives market, offering some of the most granular data available on modern trading success rates. Analyzing actual brokerage data from over 1.13 crore (11.3 million) unique individual traders between the 2022 and 2024 financial years, SEBI found that 93% of retail traders incurred net losses 123.

The absolute scale of this wealth destruction was staggering. Over the three-year period, retail individuals collectively lost ₹1.81 lakh crore (approximately $21.6 billion USD) 14. In the 2024 financial year alone, 91.1% of retail traders posted a net loss, wiping out ₹75,000 crore 14.

Furthermore, the SEBI report highlighted a disturbing demographic trend regarding who is attempting to trade for a living. The proportion of young traders under the age of 30 surged to 43% of the market in 2024, yet 93% of these younger participants lost money 34. Compounding the issue, over 75% of the individuals trading had a declared annual income of less than ₹5 lakh (roughly $6,000 USD) 13. This indicates that those with the least disposable income and the highest need for a stable salary are disproportionately participating in, and losing from, highly leveraged short-term trading.

The data demonstrates a direct transfer of wealth from retail participants to institutional players. While retail individuals were losing billions, proprietary trading desks and foreign portfolio investors (FPIs) were generating massive, consistent returns.

| Trader Classification | FY24 Aggregate Profit / Loss | Primary Execution Method |

|---|---|---|

| Individual Retail Traders | Net Loss: ₹75,000 crore (~$9.0 Billion USD) | Manual / Discretionary |

| Proprietary Trading Firms | Gross Profit: ₹33,000 crore (~$3.9 Billion USD) | 96% Algorithmic |

| Foreign Portfolio Investors (FPIs) | Gross Profit: ₹28,000 crore (~$3.3 Billion USD) | 97% Algorithmic |

Data sourced from the SEBI 2024 analysis of the Indian equity derivatives market. Retail losses are net of transaction costs, while institutional profits are gross 12.

As the data clearly demonstrates, institutional gains are driven almost entirely by algorithmic trading. Retail traders operating manually from home are fundamentally providing the liquidity that these institutional algorithms harvest 1.

Long-Term Academic Studies on Speculator Skill

The findings from modern regulatory reports align perfectly with decades of Western academic data. A landmark, peer-reviewed academic study titled "The Cross-Section of Speculator Skill: Evidence from Day Trading" analyzed Taiwanese stock traders over a 15-year period (1992 to 2006). Tracking over 450,000 individuals, the researchers found that less than 1% of the day trader population could predictably and reliably earn positive abnormal returns net of fees 569. While the study proved that genuine trading skill does exist, it noted that such skill is exceptionally rare and largely confined to the top 500 traders in the dataset, who utilized highly contrarian limit-order strategies 59.

Similar outcomes are observed in other markets. A study of committed Brazilian futures traders found that 97% lost money after persisting for over 300 days, demonstrating that simply spending more time in the market does not automatically translate to profitability 12. Across European markets, mandatory broker risk disclosures enforced by the European Securities and Markets Authority (ESMA) and the US Commodity Futures Trading Commission (CFTC) routinely show that 74% to 89% of retail accounts lose money trading CFDs and forex every quarter 1.

The Survival Gap: Swing Trading Versus Day Trading

When analyzing the viability of trading full-time, it is crucial to distinguish between day trading and swing trading, as the strategies carry vastly different survival rates, time commitments, and capital requirements.

Day trading involves opening and closing positions within the exact same trading session, never holding an asset overnight 10117. The strategy relies on capturing minor intraday price fluctuations. It requires full-time attention, constant screen monitoring (often four to eight hours a day), specialized low-latency software, and large position sizing to make small percentage moves financially meaningful 107.

Conversely, swing trading aims to capture larger, sustained market trends over a period of days to weeks. Because the targeted price movements are larger, swing traders can utilize wider stop-losses and smaller position sizes. Crucially, this style requires far less daily screen monitoring - often just 30 minutes to two hours for pre-market or post-market analysis - making it generally more forgiving to those who execute it while maintaining a traditional job 1011.

Comparative Performance Outcomes

Academic research from Cambridge University, published in September 2023, tracked 5,472 UK retail traders over a three-year period to compare these specific strategies. The researchers discovered a distinct performance gap based on strategy duration: day traders averaged annual returns of -3.8% after transaction costs, while swing traders achieved a positive +2.1% average return 8. It is important to note that these figures excluded the bottom quintile of traders who suffered total account depletion and ceased trading entirely within their first six months 8.

The higher attrition rate among day traders is widely documented across the brokerage industry. Approximately 40% of day traders quit within their first month, and 80% abandon the practice within two years 21415. Short-term swing traders fare slightly better in terms of longevity, with roughly 25% to 30% surviving past the three-year mark, compared to just 13% of day traders 159.

This survival disparity is largely driven by three underlying factors: the sheer volume of transaction costs incurred by overtrading, the psychological pressure of constant rapid-fire decision-making, and the random, noisy nature of intraday volatility 1089.

| Operational Feature | Intraday Day Trading | Active Swing Trading | Passive Index Investing |

|---|---|---|---|

| Typical Holding Period | Minutes to hours (no overnight risk) | Days to weeks (carries overnight risk) | Years to decades |

| Daily Time Commitment | 4 - 8 hours (constant monitoring) | 30 mins to 2 hours | Near-zero (set and forget) |

| Transaction Frictions | Extremely high (heavy drag on net returns) | Moderate | Minimal |

| Tax Treatment (U.S.) | Short-term capital gains (ordinary income) | Short-term capital gains (ordinary income) | Long-term capital gains |

| Historical 3-Year Survival | Extremely low (~13%) | Low to Moderate (~25-30%) | Extremely high |

Data summarized from academic research and brokerage industry attrition metrics 108159.

The Profitability Paradox: Why Winning Trades Don't Equal Wealth

A common misconception among aspiring full-time traders is that developing a strategy with a win rate above 50% guarantees long-term profitability. In reality, the mechanics of market friction and human behavioral psychology frequently push traders with winning track records into negative portfolio balances.

In April 2026, the FinTech analytics platform Followme released its Annual Trading Report, which analyzed nearly 30,000 active retail accounts throughout the 2025 trading year. The data revealed a stark profitability paradox: the community-wide average win rate was a highly respectable 63.8% 1718. On the surface, winning nearly two-thirds of all trades appears to be a formula for immense wealth. However, the overall profit-to-loss ratio for the entire community was a dismal 0.5 1718.

This ratio meant that for every dollar a trader gained on a winning position, they lost two dollars on a losing one. The average profitable trade netted just $37.29, which was entirely wiped out by an average loss of $74.03 on bad trades 1718.

A separate 2023 study analyzing over 4 million trades across 25,000 retail accounts found identical, highly destructive behavior. While 65% of the traders maintained win rates above 50%, a staggering 82% of those same traders lost money overall 1.

The Psychology of Asymmetric Trade Sizing

The root cause of this paradox is asymmetric trade sizing driven by human emotion. Traders instinctively close winning positions far too early out of a fear of losing their unrealized gains, while simultaneously holding onto losing positions far too long in the hope that the market will reverse 119. The 2023 study found that the average winning trade gained about 1.2%, while the average losing trade cost the portfolio 2.8% 1.

Over hundreds of executions, this imbalance mathematically destroys returns, regardless of how often the trader predicts the correct market direction. A trader operating with a 1:2 risk-to-reward deficit needs an unsustainably high win rate just to break even, leaving zero margin for error when factoring in the cost of doing business.

The Hidden Frictions Eroding Trader Alpha

Even if a trader masters their psychology and perfectly executes a strategy with a positive statistical expectancy, they must overcome the mathematical reality of transaction friction. Every time a trader enters and exits the market, they pay a toll. This toll comes in the form of direct broker commissions, bid-ask spreads (the difference between the buying and selling price dictated by institutional market makers), and slippage (the difference between the expected price of a trade and the price at which it actually executes) 152021.

Because swing traders operate on wider timeframes and target larger percentage moves, they can absorb slightly more friction than day traders. However, an active swing trader attempting to replace a full-time income is still subject to heavy institutional tolls. A trader executing 100 round-trip trades a month at an average cost of $8 per trade faces $9,600 in annual friction before even accounting for the hidden costs of spreads and slippage 8.

As one market analyst notes, if you risk $1 to make $1, the mathematical certainty of the bid-ask spread will slowly bankrupt the portfolio over 1,000 trades 22. Active trading introduces significant friction through these overheads, quietly chipping away at the principal before compounding can even take root 20.

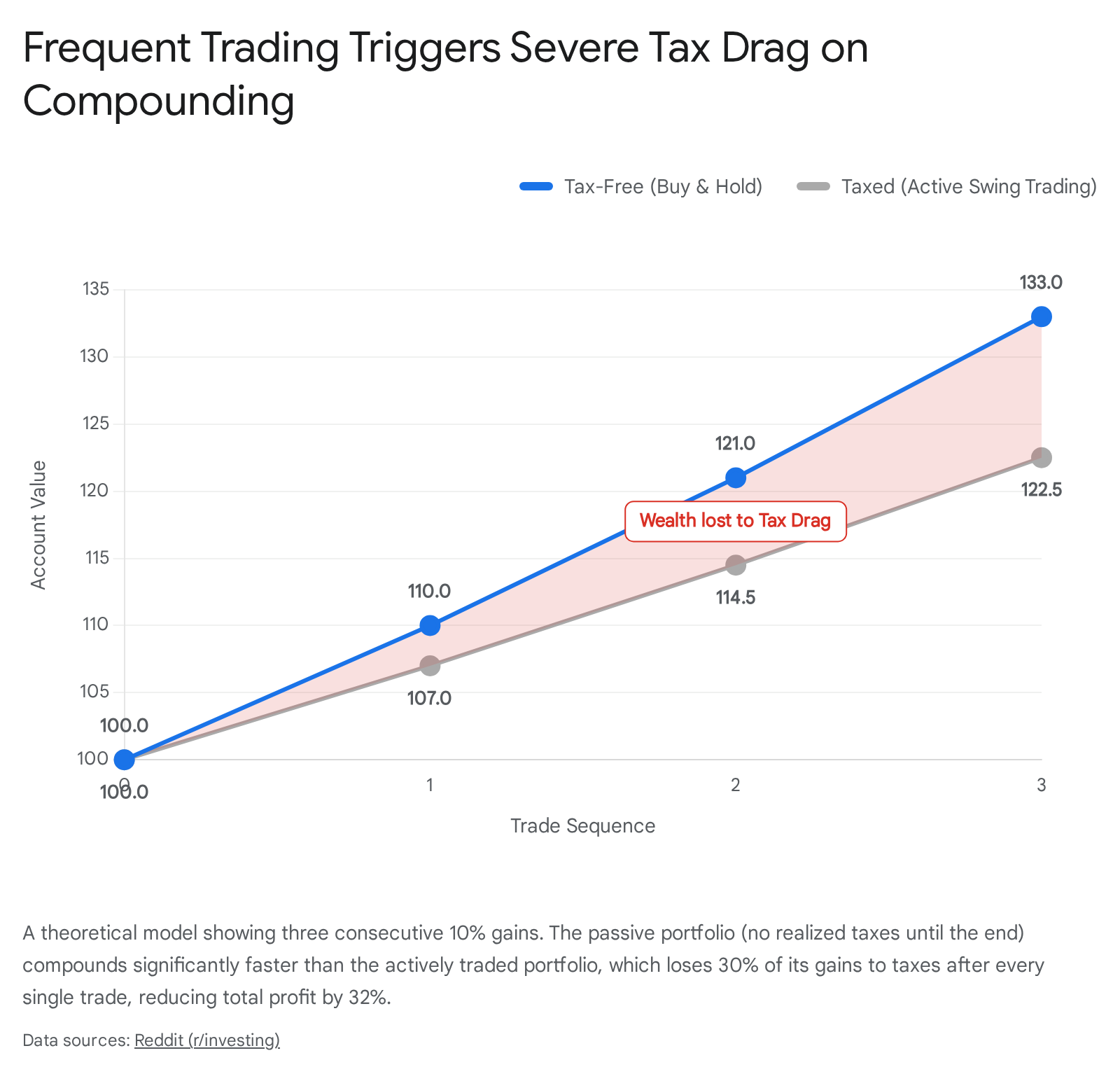

The Severe Impact of "Tax Drag" on Active Portfolios

Perhaps the most underestimated headwind for full-time swing traders is "tax drag." When an individual transitions from a passive, buy-and-hold investing strategy to an active trading approach, the tax efficiency of their portfolio plummets 202324.

In the United States and many other jurisdictions, positions held for less than a year are subject to short-term capital gains taxes, which are typically taxed at the individual's higher ordinary income tax rate. Conversely, long-term investments benefit from preferential, much lower tax brackets 25261011.

When a trader actively realizes gains throughout the year, the capital paid out in taxes is no longer available to compound in future trades. Over time, this repeated disruption of compounding causes massive underperformance compared to passive strategies.

Consider a simplified quantitative example over multiple periods: If an investor achieves three 10% sequential gains in a tax-free or tax-deferred account, a $100 starting balance grows to $110, then $121, and finally $133 23. However, if those same trades are realized actively and subjected to a 30% tax rate upon each exit, the post-tax growth path is severely stunted: $100 grows to $107, then $114.50, and finally $122.50. In this scenario, the total tax drag reduced the overall profit margin by 32% 23.

Extended over a 20-to-25-year career, tax drag and transaction friction can reduce total cumulative profits by 50% or more when compared to a disciplined buy-and-hold index approach 2324.

Trading as a Small Business: The True Cost of Going Full-Time

One of the most dangerous traps for prospective full-time traders is treating gross market returns as pure salary. When you quit a W-2 or traditional salaried job to trade, you are fundamentally starting a capital-intensive small business 2129. Your trading capital acts as your business inventory, and you must cover your own operational overhead, self-employment taxes, and medical benefits before realizing a true personal profit.

Capital Requirements and Operational Overhead

Like any enterprise, an independent trading business requires operating expenses to function. Professional-grade charting software, real-time exchange data feeds, high-speed internet redundancy, and news terminal subscriptions add up quickly 1030. For a small account, these fixed overhead costs can easily consume a large percentage of gross profits, pushing an otherwise profitable strategy into the red 10.

While standard brick-and-mortar small businesses generally target an overhead expense ratio of 20% to 35% of total revenue, retail traders must operate much leaner, as their profit margins are heavily beholden to unpredictable market regimes and volatility cycles 31323334.

The Self-Employment Tax Burden

In the United States, traditional employees only pay half of their payroll taxes, as their employer subsidizes the other half. When you trade full-time as an independent entity, you become responsible for the entire burden.

For the 2025 tax year, self-employed individuals must pay a 15.3% self-employment tax (covering Social Security and Medicare) on 92.35% of their net business earnings, up to an income limit of $176,100 for the Social Security portion 1237. This 15.3% levy is applied in addition to standard federal and state income taxes determined by your tax bracket 2513.

Without careful entity structuring - such as electing S-Corporation status to split revenue into distributions and a reasonable W-2 salary - or utilizing specialized retirement accounts like a Solo 401(k) or SEP-IRA, full-time traders can lose a devastating percentage of their hard-won gross profits to the IRS 2513.

Replacing the Corporate Safety Net: Health Insurance in 2026

When a worker leaves corporate employment, they lose access to subsidized group health insurance. For self-employed individuals, health care is often one of the largest, most volatile, and most stressful annual expenses 39.

With the expiration of expanded Affordable Care Act (ACA) subsidies, self-employed medical insurance costs are adjusting upward. For the 2026 coverage year, industry projections place standard individual health insurance premiums between $575 and $789 per month 39404114. For a family of four, the burden is substantially higher, ranging from $1,200 to over $2,800 per month depending on the state of residence, ages of the insured, and the tier of the plan chosen 3914.

Furthermore, the monthly premium is merely the entry fee. Traders must also factor in annual deductibles, which dictate how much must be paid out-of-pocket before the insurance actually covers major medical costs.

| 2026 ACA Plan Tier | Est. Monthly Premium (Individual) | Est. Monthly Premium (Family of Four) | Typical Deductible Range |

|---|---|---|---|

| Bronze (High Deductible) | $405 - $450 | $1,200 - $1,500 | $3,000 - $7,000 |

| Silver / HMO / EPO | $540 - $676 | $1,600 - $2,000 | $1,500 - $4,000 |

| Gold / PPO (Broad Network) | $789+ | $2,000 - $2,800+ | $500 - $2,000 |

Cost estimates for self-employed private health insurance in 2026, prior to any applicable income-based tax credits 39404114.

If a full-time swing trader requires $4,000 a month just to cover their baseline mortgage, food, and utilities, they must now generate an additional $1,000 to $2,000 a month just to pay for health coverage and self-employment taxes. This drastically raises the required monthly return on their trading capital, forcing them to take larger, riskier positions to meet their monthly cash flow needs.

The Institutional Benchmark: What Professional Traders Actually Make

A major driver of retail trader failure is a fundamental misunderstanding of realistic market returns. Novice traders often enter the market believing they can consistently double their money or generate 5% to 10% returns every single month. To put these expectations into perspective, one must look at the highest echelons of professional finance.

Hedge funds command trillions of dollars in assets, employ teams of PhD quantitative analysts, and utilize cutting-edge infrastructure. Despite these immense advantages, they rarely generate the astronomical returns that social media influencers claim to achieve.

In 2024, hedge funds had their strongest year since before the Global Financial Crisis, delivering average net returns of 10.1% 43. In 2025, they posted another banner year, returning an average of 12.6% 1516.

However, even in their best years, the average hedge fund frequently underperforms a standard, low-cost S&P 500 index fund 16. In 2025, the S&P 500 yielded a 17.9% return - beating the elite hedge fund average by over 5 percentage points 16. In fact, in all but three of the last 16 years (2015, 2018, and 2022 - which were all down-markets where hedge funds simply lost less), hedge funds have failed to outperform the broader market index 16. Over a 16-year horizon, the average annual return of the S&P 500 was 12.86%, more than double the 6.22% average annual return of hedge funds 16.

If the most well-capitalized institutional investors in the world struggle to consistently beat 12% a year, the expectation that an independent retail trader will generate 50% to 100% annual returns without taking on catastrophic levels of ruinous risk is mathematically unfounded.

The Psychological Toll of Drawdowns

Even if a trader develops a strategy with a slight statistical edge, executing it perfectly in a live environment is exceptionally difficult. Behavioral finance research widely asserts that cognitive biases and emotional instability sabotage far more trading accounts than flawed technical strategies.

Loss Aversion and Cognitive Biases in Live Markets

Humans are biologically ill-equipped to handle the probabilistic nature of the financial markets. Dr. Daniel Kahneman and Amos Tversky's foundational Nobel-winning research, Prospect Theory, demonstrates that humans experience the psychological pain of losing money 2.5 times more intensely than the joy of an equivalent financial gain 4647.

This hardwired "loss aversion" causes traders to act irrationally. In controlled clinical simulations and live market environments, the stress of a sudden drawdown elevates cortisol levels, triggering a physiological fight-or-flight response 47. This often manifests as "revenge trading" - where an individual aggressively doubles down on a losing position to quickly recover their capital - or "tilt," a poker term describing an emotionally reactive state of decision-making that ignores all established risk parameters 1947.

A trader who is relying on their portfolio for their next mortgage payment operates under immense psychological pressure. A 10% portfolio drawdown that might be viewed as a minor, temporary inconvenience to a passive long-term investor becomes an existential threat to a full-time trader, frequently leading to impulsive, account-destroying overcorrections 4648. Some trading psychologists suggest that success in the markets is comprised of 60% trading psychology, 30% position sizing and risk management, and only 10% the actual trading system itself 47.

The Finfluencer Illusion and Unrealistic Expectations

The psychological challenge of trading is severely exacerbated by a toxic ecosystem of social media "finfluencers" who sell the illusion of easy money. A recent analysis of TikTok forex content revealed that 50% of videos consisted solely of influencers flaunting lavish lifestyles with absolutely no relevant trading context 17. Furthermore, less than 23% of the analyzed content contained actual actionable financial information 17.

Industry insiders point out that the majority of trading creators do not make their money from trading; they monetize attention. They generate revenue by selling educational courses, charging for access to private chat groups, and collecting affiliate marketing kickbacks from the very brokerages where their retail followers routinely lose money 5018. Regulatory bodies like the Financial Conduct Authority (FCA) and the Ontario Securities Commission (OSC) have increasingly warned that this ecosystem skews retail expectations, encouraging novices to quit their jobs and attempt to replicate a lifestyle that is largely fabricated 501819.

The Changing Landscape: The 2026 PDT Rule Shift

Historically, one of the primary reasons retail participants chose to swing trade instead of day trade was the U.S. regulatory barrier known as the Pattern Day Trader (PDT) rule.

Enacted in 2001 following the massive retail losses of the dot-com bubble crash, the FINRA rule stated that any margin account executing four or more day trades within five business days was classified as a pattern day trader. These accounts were strictly required to maintain a minimum equity balance of $25,000. If an account dipped below that threshold, the broker was forced to freeze the trader's intraday capabilities for 90 days 205421.

For 25 years, this $25,000 threshold forced undercapitalized retail participants into swing trading, where they had to hold positions overnight - taking on overnight gap risk - simply to avoid triggering the PDT classification 205422.

How the SEC's Margin Update Impacts Retail Traders

On April 14, 2026, the SEC approved sweeping amendments to FINRA Rule 4210, officially eliminating the $25,000 minimum equity requirement and stripping away the pattern day trader designation entirely 205423. Effective June 4, 2026, retail traders with accounts as small as $2,000 can execute unlimited intraday trades in a margin account, provided they meet standard, real-time intraday margin exposure limits 202122.

Broker-dealers will now monitor risk dynamically throughout the trading day rather than relying on a rigid, end-of-day trade-counting mechanism 2023.

While this regulatory shift is a massive victory for market accessibility - allowing smaller swing traders to freely cut losing positions intraday without fear of a 90-day account freeze - it also removes the regulatory "velvet rope" that kept casual investors out of the fastest, most aggressive segment of the market 542122. Given the abysmal 13% long-term survival rate of day traders, the removal of the PDT rule is likely to accelerate the rate at which undercapitalized retail traders churn through their savings, as the line between swing trading and day trading is entirely erased.

Bottom line

The data is unequivocal: attempting to replace a full-time salary with swing trading or day trading is a highly improbable endeavor, with 70% to 97% of retail participants losing money. While a small fraction of individuals do achieve long-term, consistent profitability, they succeed by treating their trading as a disciplined, well-capitalized business, rather than a casual pursuit. For anyone considering quitting their job, it is vital to account for the heavy burdens of self-employment taxes, health insurance costs, transaction friction, and tax drag, as these silent expenses will relentlessly erode even a winning strategy over time.