Integrated and modular architectures in competitive markets

System architecture - the fundamental arrangement of functional elements into physical or digital building blocks and the interfaces connecting them - dictates not only how a product operates but also how industries are structured and where profit accumulates. In competitive markets, the choice between an integrated, interdependent architecture and a modular, distributed architecture is rarely arbitrary. It is governed by the technological maturity of the product category, the specific performance bottlenecks of the era, and the evolving demands of the end consumer.

The cyclical transition between integrated and modular architectures provides a foundational framework for understanding contemporary market disruptions. From the consolidation of the artificial intelligence hardware stack to the restructuring of the global automotive supply chain, the principles of system architecture explain why certain firms achieve dominant market positions while others are relegated to low-margin commoditization.

Foundational Principles of System Architecture

To analyze when a specific architectural strategy will succeed, it is necessary to examine the underlying economic and technological conditions that dictate market demands. Two foundational theories explain this dynamic: the theory of interdependence and modularity, and the law of conservation of attractive profits.

The Theory of Interdependence and Modularity

The theory of interdependence and modularity, prominently developed by Clayton Christensen, posits that the optimal product architecture is dictated entirely by the market circumstances surrounding product performance 1. The theory divides market conditions into two distinct states: the "not good enough" phase and the "good enough" phase.

When the performance of a product or service is "not good enough" to meet the baseline demands of the market, an integrated, interdependent approach reliably establishes market dominance 1. In this state, achieving the required performance necessitates pushing the physical, mathematical, or technological limits of the system. Engineers cannot rely on standardized interfaces or third-party components because doing so introduces inefficiencies, physical latency, or unnecessary computational overhead 1. Instead, the system must be vertically integrated. By controlling the entire stack, a single firm can optimize across component boundaries, co-designing hardware and software to maximize output. A historical example of this occurred in the mid-1990s when the existing optical fiber network transitioned from being "good enough" for basic voice telephony to "not good enough" for high-speed internet access 1. The sudden performance deficit required heavily integrated telecommunications infrastructure to push bandwidth limits, causing modular Competitive Local Exchange Carriers (CLECs) to fail against deeply integrated incumbent phone companies 1.

Conversely, when product performance overshoots what the target market can utilize or is willing to pay for, it reaches the "good enough" state. At this inflection point, customers are no longer willing to pay a premium for marginal improvements in raw performance 1. The basis of competition fundamentally shifts away from absolute performance and toward speed to market, customization, convenience, and unit cost. In this environment, a modular architecture dominates. Modularity involves decomposing a system into separate, independent components that interact through well-defined, standardized interfaces 22. Because the interfaces are standard, firms can outsource the development of specific modules to specialized third-party suppliers. This distributed approach allows suppliers to specialize in specific niches, achieve economies of scale, optimize their manufacturing processes, and drive down overall costs 1.

For a modular ecosystem to function effectively, three strict conditions must be met regarding the interfaces between components 4. The interfaces must be: 1. Specified: Having explicitly defined inputs and outputs without ambiguity. 2. Measurable: Quantifiable in terms of data transfer, speed, rate limits, or physical tolerances. 3. Reliable: Exhibiting stable dependencies that do not require constant system rewrites or adjustments when one module is upgraded 4.

When these conditions are met, independent parties can innovate asynchronously on their respective modules without breaking the broader system, dramatically increasing the overall speed of industry innovation 4.

The Law of Conservation of Attractive Profits

The corollary to the theory of interdependence and modularity is the "law of conservation of attractive profits," an economic principle detailing profit migration. This principle states that when modularity and commoditization cause attractive profit margins to disappear at one stage of the value chain, the opportunity to earn attractive profits with proprietary products will reliably emerge at an adjacent, interdependent stage 5634.

In any complex value chain, there is a requisite juxtaposition of modular and integrated architectures. Profit reliably migrates to the layer of the stack that solves the hardest, most complex integration problems 5. If a previously integrated layer standardizes and becomes modular, the barriers to entry drop, competition floods in, and prices fall toward marginal cost 56. However, the systemic performance constraints do not vanish; they simply shift to a different bottleneck in the system hierarchy. The firms that position themselves to provide deeply integrated, proprietary solutions at this new bottleneck will capture the disproportionate share of industry profits 69.

This dynamic is referred to as "integration arbitrage" 6. It provides a predictive mechanism for evaluating technology markets, suggesting that highly profitable monopolies or oligopolies are continuously threatened by the standardization of their core offerings, forcing them to integrate adjacent layers to remain economically viable 65. This framework is heavily utilized not only in commercial strategy but also in military defense planning to ensure resource allocation anticipates the next innovative leap as standard capabilities commoditize 4.

Comparative Characteristics of System Architectures

The strategic implications of choosing either architecture extend to organizational structure, supply chain resilience, and financial risk profiles. The table below summarizes the fundamental differences between the two paradigms based on current systems engineering data.

| Architectural Characteristic | Integrated (Interdependent) Architecture | Modular (Distributed) Architecture |

|---|---|---|

| Market Condition Trigger | Product performance is "not good enough" to meet market demands 1. | Product performance is "good enough" to satisfy baseline market needs 1. |

| Component Coupling | Tightly coupled; components form a unified whole with shared resources and complex interdependencies 22. | Loosely coupled; components interact strictly through well-defined, standardized interfaces 22. |

| Development Speed | Slower initial development due to systemic complexity and the requirement for simultaneous, centralized engineering 12. | Rapid speed to market (often 5x to 10x faster); enables parallel development and incremental module upgrades 1112. |

| Primary Competitive Advantage | Maximum absolute performance, system efficiency, power optimization, and tight quality control 26. | Maintainability, high reusability, cost efficiency, and flexibility in supply chain sourcing 211. |

| Innovation Vector | Pushing absolute technological boundaries through sweeping, systemic architectural overhauls 1. | Continuous innovation via rapid iteration of individual modules; specialized niche optimization 114. |

Historical Cycles in the Computing Industry

The history of the computing industry illustrates a continuous oscillation between integration and modularity as technological constraints shift over sequential computing eras.

The Era of Mainframes and Vertical Integration

In the 1960s and 1970s, the computing industry was dominated by mainframes - massive, highly integrated systems engineered primarily by IBM 78. Because computational power, memory, and networking were severely constrained, mainframes required a monolithic software architecture and tightly coupled hardware to function effectively 79. Applications were programmed in languages like COBOL within a unified codebase that contained the data schema, application logic, and presentation logic without modularization 7. IBM's approach to the mainframe was a classic interdependent strategy, capturing high margins by solving the extreme integration challenges of early digital computing.

The Rise of Personal Computing and Standardization

As microprocessors and memory densities improved, baseline computing power eventually overshot the basic needs of business users, triggering a transition to the modular personal computer (PC) era 18. To accelerate time-to-market and lower costs, IBM shifted its strategy to a modular architecture for its PC line. Rather than maintaining full control over hardware and software, IBM outsourced the development of its operating system to Microsoft and the production of its microprocessors to Intel 1.

This modular approach allowed each supplier to specialize and drive costs down, establishing a sprawling ecosystem of PC clone manufacturers. Following the law of conservation of attractive profits, as the hardware assembly layer commoditized and hardware profit margins evaporated, value migrated up the stack 59. Microsoft and Intel, which provided proprietary, highly integrated solutions at the new bottlenecks (the OS and the processor), captured the vast majority of industry profits 19.

Software Development Life Cycles and Composable Architecture

As physical networking bandwidth reached a "good enough" state globally, the computing industry shifted from local application hosting to cloud computing and Software-as-a-Service (SaaS) 78. This shift fundamentally altered the Software Development Life Cycle (SDLC) 1819. The traditional SDLC consists of distinct phases - inception/planning, elaboration/analysis, construction/coding, and transition/deployment 1819. Historically, monolithic architectures required sequential progression through these phases (the Waterfall model), severely limiting agility 10.

To increase development velocity, the industry adopted Agile methodologies combined with modular, composable architectures 1410. Modern cloud-native integration relies on microservices, containerization (e.g., Docker, Kubernetes), and API-led connectivity 1421. By breaking complex systems into functional components that operate independently, companies report massive increases in agility, with development speeds accelerating by 5x to 10x compared to monolithic architectures 12.

Currently, organizations using composable IT architectures reduce technical debt and accelerate time-to-market, with projections suggesting modular systems will enable companies to achieve up to 30% higher revenue growth by 2025 due to rapid innovation capabilities 14. This hyper-modular software ecosystem has resulted in widespread enterprise adoption; the average company now relies on over 112 distinct SaaS applications, reflecting a preference for loosely coupled, best-of-breed point solutions 11.

Generative Artificial Intelligence and Architectural Re-Integration

The advent of large-scale generative artificial intelligence (GenAI) and foundation models in the 2020s has fundamentally reset the computing paradigm. The mathematical and computational requirements for training and inferencing models with hundreds of billions of parameters are vastly higher than traditional enterprise workloads. This has pushed existing cloud infrastructure back into a "not good enough" state, triggering a severe structural re-integration of the AI value chain 2312.

Profit Margin Dynamics and the "SaaSpocalypse"

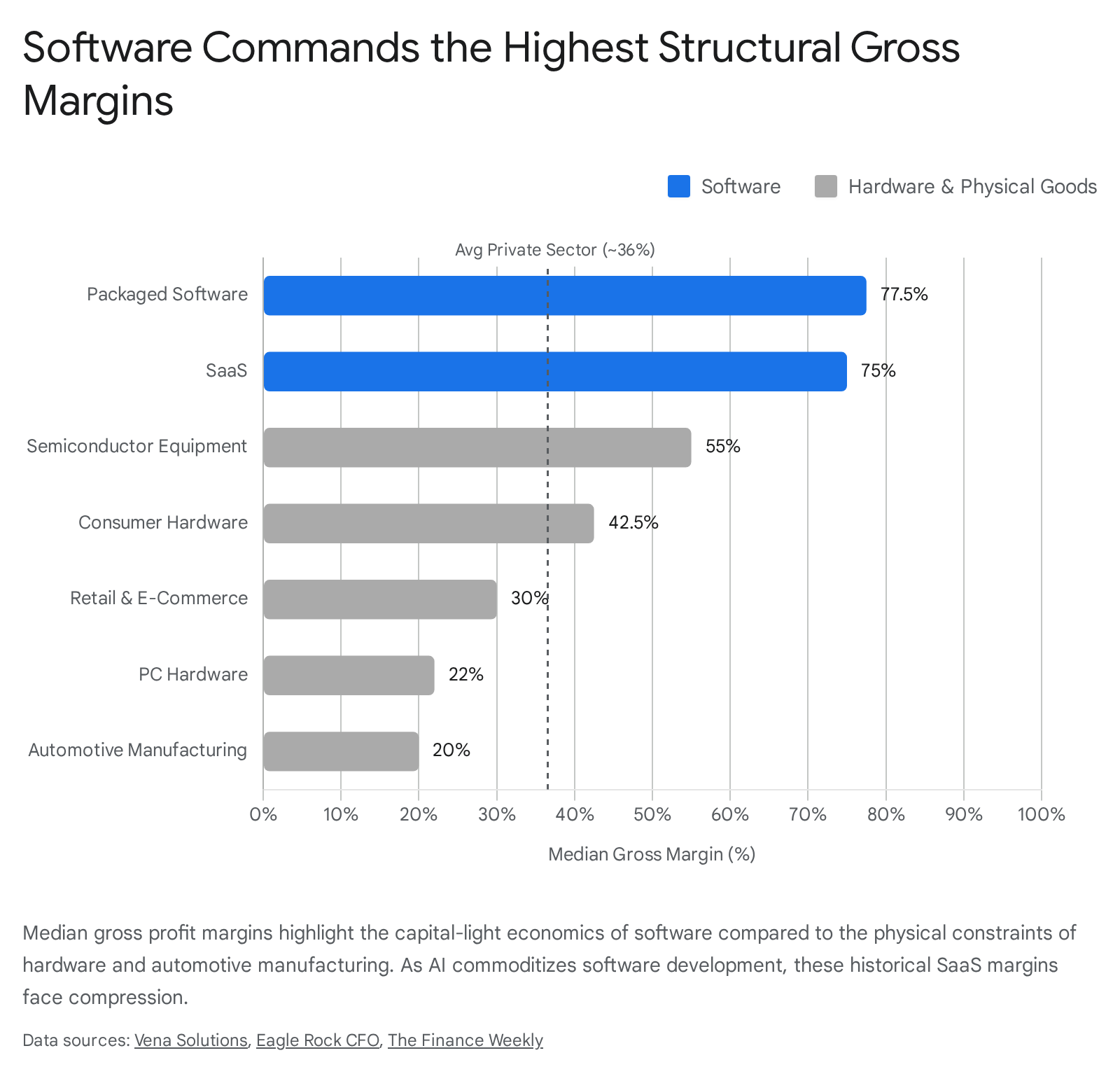

For the past decade, the modular application software layer captured immense value. IRS corporate tax data and industry benchmarks reveal that packaged software and SaaS companies enjoyed structural gross margins of 70% to 85%, significantly higher than the 36.5% overall private sector average or the 12% to 25% margins typical of physical hardware and automotive manufacturing 1326271415.

These margins were sustained by the near-zero marginal cost of digital distribution and strong customer switching costs 2616.

However, AI models are rapidly automating code generation, data processing, and user interfaces, threatening to commoditize the enterprise software layer 61617. Because modern GenAI tools can orchestrate complex workflows and generate custom software integrations on demand, the standardized SaaS application is losing its proprietary edge 617. Financial markets have reacted sharply to this dynamic; in early 2026, ETFs for public software companies experienced drawdowns of up to 30%, a phenomenon analysts dubbed the "SaaSpocalypse" 17.

Following the law of conservation of attractive profits, as software integration becomes trivial, profit pools are migrating downward into the infrastructure and model layers where physical and mathematical integration remains extremely difficult 632. By early 2026, nearly all value creation in the tech sector was captured by semiconductor manufacturers, cloud utilities, and energy providers 32. The gap in AI capabilities remains highly concentrated; private investment in generative AI reached $33.9 billion in 2024, with U.S. investment exceeding the combined totals of China, the European Union, and the U.K. 18.

Hardware Integration and Rack-Scale Computing

For most of the last four decades, the technology hardware sector organized itself around specialization: chip designers handed blueprints to foundries, foundries shipped silicon to hardware OEMs, and cloud providers rented the assembled capacity 23.

AI model training and inference are no longer bottlenecked by any single modular component. They are strictly constrained by the simultaneous coordination of silicon, high-bandwidth memory, optical networking, liquid cooling, and power delivery 23. Optimizing one layer in isolation yields marginal benefits, while optimizing all of them interdependently produces step-change performance gains 23.

This economic logic is driving massive vertical integration. Nvidia has evolved from a discrete graphics processor vendor into a fully integrated systems company 23. Modern AI data center deployments, such as the Nvidia GB200 NVL72, are shipped as pre-integrated, liquid-cooled rack-scale systems linking 36 CPUs and 72 GPUs via a proprietary NVLink interconnect fabric 23. By removing modular bottlenecks (like standard x86 CPU interfaces) and controlling the networking and cooling architecture, Nvidia achieves a 30x increase in real-time inference speed for trillion-parameter models 23.

Similarly, hyperscale cloud providers - Alphabet, Amazon, and Microsoft - are integrating upward by designing and deploying custom Application-Specific Integrated Circuits (ASICs) 2319. Driven by the need to avoid premium markups from third-party chipmakers and manage the severe physical limits of data center power delivery, hyperscalers treat infrastructure as a deeply integrated utility 23. Google's Tensor Processing Units (TPUs), closely integrated with its TensorFlow software, execute inference workloads at significantly higher cost-efficiency than modular hardware setups 23.

In the consumer edge computing sector, Apple executes a profound vertical integration strategy through its custom Apple Silicon 620. By controlling the entire technology stack from the ARM-based System-on-a-Chip (SoC) to the operating system, Apple achieves unparalleled optimization in performance-per-watt 620. Integrating the CPU, GPU, unified memory, and a specialized Neural Engine onto a single package bypasses the latency of modular motherboards, enabling advanced on-device AI inference with minimal power consumption 620.

Emergent Modularity in Compound AI Systems

While the physical hardware layer requires aggressive integration, the software architectures governing AI models are evolving toward internal modularity. Early large language models were essentially monolithic architectures; scaling their capabilities required exponentially increasing the total parameter count, which led to unsustainable compute costs, high latency, and issues with hallucination 2122.

To bypass the "curse of dimensionality" - where shallow architectures require exponentially growing parameter counts to process complex inputs - the AI research community is transitioning to Compound AI Systems (CAIS) 2122. Rather than relying on a single monolithic model, CAIS architectures decouple sub-task responsibilities into specialized modules 22. These architectures integrate core LLMs with external components such as high-recall information retrievers (RAG), tool-using agents, symbolic planners, and multimodal encoders 22.

According to AI architectural research, these modular systems operate using three formal mathematical component functions: 1. Routing Functions ($r_\rho$): Algorithms that direct an input query to the most appropriate specialized expert model or module, minimizing the computational cost of running the entire neural network (e.g., Sparse Mixture of Experts) 21. 2. Aggregation Functions ($g_\gamma$): Operations that synthesize the outputs from various independent modules into a cohesive final response, ranging from simple weighted summations to complex attention mechanisms 21. 3. Modifier Functions ($d_\delta$): Functions utilized in transfer learning that modify a base network's layer without requiring a full system retrain 21.

This modular approach within the AI stack confers massive computational advantages. It mitigates "catastrophic interference" (where a neural network forgets prior knowledge when trained on new data), enhances compositional reasoning, and allows for massive expansions in system capacity with only modest increases in inference costs 21. Currently, 62% of surveyed enterprise organizations report experimenting with modular, agentic AI systems, though less than a third have successfully scaled them across multiple business functions .

The Automotive Transition to Software-Defined Vehicles

The global automotive industry is undergoing a structural disruption that mirrors the computing sector, transitioning from Internal Combustion Engine (ICE) vehicles to Battery Electric Vehicles (BEVs) and Software-Defined Vehicles (SDVs) 2324. This shift has completely upended traditional system architectures and supply chain dynamics, altering how physical assets and digital interfaces interact.

Limitations of Legacy Domain-Based Architectures

For decades, legacy automakers operated as highly efficient system integrators managing fragmented, domain-based architectures 2526. A modern ICE vehicle might contain up to 150 independent Electronic Control Units (ECUs) scattered throughout the chassis, with each ECU controlling a specific modular function (e.g., braking, infotainment, powertrain) provided by diverse Tier 1 suppliers 2526.

While this modularity served the mechanical era well, it is incompatible with the demands of modern electric and autonomous mobility 2526. The SDV paradigm demands continuous over-the-air (OTA) updates, autonomous driving data processing, and highly efficient thermal management. Legacy ECU sprawl increases communication latency, bloats cabling weight (which critically reduces EV range), and creates severe integration bottlenecks during manufacturing 2526. The existing modular architecture has become structurally "not good enough."

As a result, automotive architectures are shifting toward centralized or zonal computing. This involves consolidating processing power into a few high-performance central computing platforms, deeply integrating hardware and software to enable real-time agility and continuous evolution decoupled from hardware production timelines 252643.

The Comprehensive Vertical Integration Model

To navigate this transition, automotive firms have adopted starkly different strategies regarding vertical integration, primarily dividing into comprehensive and distributed models 27.

The Chinese automaker BYD exemplifies the comprehensive, vertically integrated model. Entering the market initially as a battery manufacturer, BYD controls nearly its entire supply chain 2728. It heavily integrates the extraction of raw materials, battery cell manufacturing, the fabrication of power semiconductors (IGBTs), and the assembly of electric drive systems 272846. By treating the EV architecture as a deeply interdependent system, BYD achieves profound technological synergies. Its "eight-in-one" electric drive module heavily integrates the motor, controller, and battery management system, vastly improving power density and reducing costs 27.

Because the underlying battery efficiency and thermal management technologies of EVs were "not good enough" during the early years of the transition, BYD's tight integration allowed it to push performance boundaries rapidly 2729. By 2024, BYD overtook major legacy automakers in global EV sales volume, boasting gross profit margins exceeding 18%, outperforming less integrated competitors 27. The Chinese domestic supply chain enables this rapid scaling; for instance, the city of Changzhou houses 31 of the 32 stages of power battery production, creating hyper-localized integration 30.

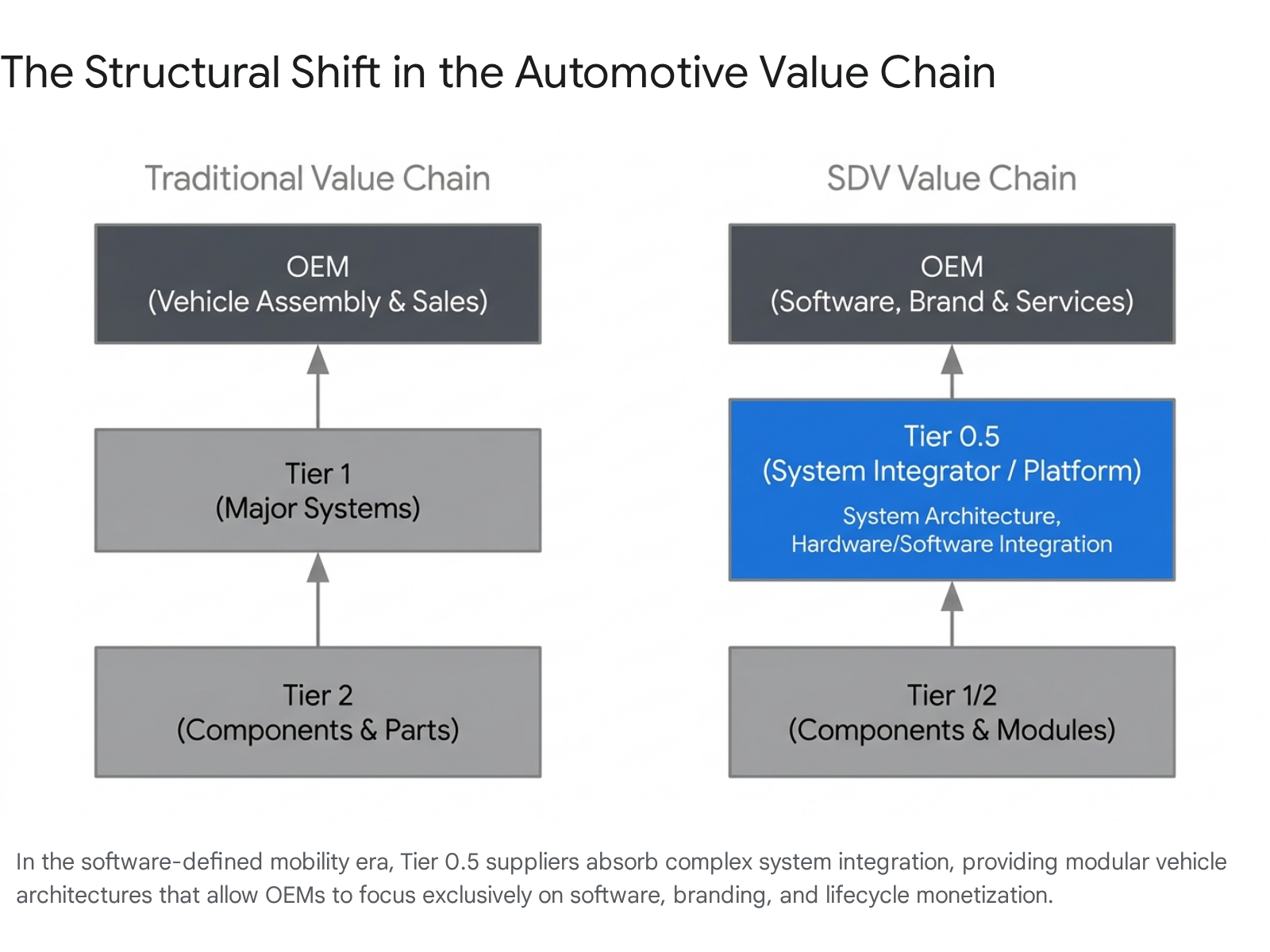

The Distributed Model and the Rise of Tier 0.5 Suppliers

As foundational EV components (such as lithium-ion batteries and standard electric motors) approach a "good enough" state for general consumer use, the basis of competition is shifting toward digital experience, AI integration, and speed to market 49. This is paving the way for a highly modular distributed approach.

Traditional automakers are burdened by development lifecycles that historically required four to seven years from concept to assembly line 305031. In contrast, new entrants in the Chinese market are deploying updated vehicle models in as little as 1.3 to 1.5 years, iterating mobility hardware at a pace resembling consumer electronics 4630. They achieve this through reliance on a newly emerged layer in the value chain: the Tier 0.5 supplier 2449.

Unlike traditional Tier 1 suppliers that provide isolated, discrete components (like a brake caliper or a single ECU), Tier 0.5 suppliers offer comprehensive, integrated, and modular vehicle platforms - often referred to as "skateboards" 2449.

Companies such as Magna, Bosch, Huawei, and LG are transitioning into this space 2449. These Tier 0.5 platforms come pre-integrated with by-wire steering systems, battery pack integration, centralized computing nodes, and advanced driver-assistance systems (ADAS) 24.

By sourcing a modular Tier 0.5 platform, automakers (including technology firms entering the automotive space, like Xiaomi) bypass the massive capital expenditure and time required to engineer core automotive hardware 2732. They can instead focus purely on the differentiating, high-margin interdependent layer of the future: the software stack, brand experience, and digital ecosystem 2449.

Strategic Implications of Tier 0.5 Dominance

The shift to Tier 0.5 modularity represents a critical power struggle within the automotive value chain. As noted by industry analysts, the Tier 0.5 layer defines the electrical architecture, controls the APIs, and manages the continuous over-the-air updates 49. If an OEM entirely outsources this layer, it risks becoming a mere brand shell, submitting control of the vehicle's ecosystem and downstream lifecycle monetization to the platform provider 49.

This dynamic directly reflects the law of conservation of attractive profits: if the physical manufacturing of the car becomes a modular, outsourced commodity via Tier 0.5 platforms, the profits will migrate to the interdependent layer that dictates the software architecture and user data orchestration 649. To maintain sovereignty, traditional OEMs must carefully decide whether to build, partner, or submit to these emerging platform orchestrators 49.

Modularity in Physical Infrastructure and Advanced Manufacturing

The principles of interdependence and modularity extend beyond software and silicon into physical infrastructure and advanced manufacturing systems.

Sustainable Modular Construction

In the physical construction sector, modularity is increasingly utilized to solve performance bottlenecks related to sustainability and speed 3334. Traditional construction is highly integrated on-site, leading to significant material waste and long project timelines 33. Modular construction (MC) involves manufacturing standardized volumetric units or panels offsite in controlled factory environments, which are then rapidly assembled on location 3334.

This modular approach significantly reduces environmental impact and waste. When aligned with Circular Economy (CE) principles - specifically Design for Disassembly (DfD) - modular building components can be reused across multiple lifecycles 3435. Life cycle assessment (LCA) studies indicate that reusing modular building components can offset greenhouse gas (GHG) emissions by up to 88% compared to traditional demolition and recycling, provided the interfaces between modules remain standardized and reliable across generations 3435.

Advanced Manufacturing and Lights-Out Production

In global manufacturing, the traditional mass-production model relied on high volumes of integrated, inflexible assembly lines paired with large human workforces 9. Today, advanced manufacturing competes on the ability to integrate software, AI, and robotics into physical production at scale 9.

This has led to the rise of "lights-out" factories - highly automated, low-headcount facilities operated by multi-agent AI systems and robotics 9. By combining the highly modular elements of industrial robotics with deeply integrated AI orchestration software, manufacturers achieve unparalleled flexibility, allowing them to dynamically switch production lines between different product modules without extensive physical retooling 936.

Conclusion

The theory of interdependence and modularity serves as a highly reliable heuristic for predicting technological and economic shifts across diverse industries. When markets demand performance breakthroughs - whether minimizing latency in large language model inference, maximizing energy density in electric vehicle powertrains, or pushing the bandwidth of early internet infrastructure - integrated architectures inevitably dominate. They bypass the overhead of standardized interfaces, allowing firms to optimize comprehensively across the entire system boundary.

However, once a technology matures to a state where baseline performance is "good enough" for the target market, the economic incentives irreversibly flip. Modularity takes hold, driving rapid innovation, supply chain resilience, and fierce price competition among specialized component providers.

Crucially, the commoditization caused by modularity does not destroy industry value; it displaces it. As dictated by the law of conservation of attractive profits, whether observing the migration of margins from SaaS applications down to AI infrastructure, or from physical automotive hardware up to software-defined vehicle platforms, attractive financial returns reliably flow to the adjacent layers of the stack where complex, interdependent integration is still required. Recognizing these architectural inflection points is essential for firms seeking to defend their economic moats, structure their supply chains, or capture new value in rapidly transitioning markets.