How International Wire Transfers Work Step-by-Step

When you wire money internationally, your bank does not send physical cash; rather, it transmits a highly secure digital message instructing a chain of intermediary banks to pass the funds along to the final destination. Because financial institutions in different nations operate on disconnected domestic systems, these intermediaries bridge the gap, deducting service fees and applying exchange rate markups along the way. This complex, multi-hop relay system dictates the cost, speed, and traceability of every cross-border payment.

The Core Mechanism: Bridging Disconnected Financial Islands

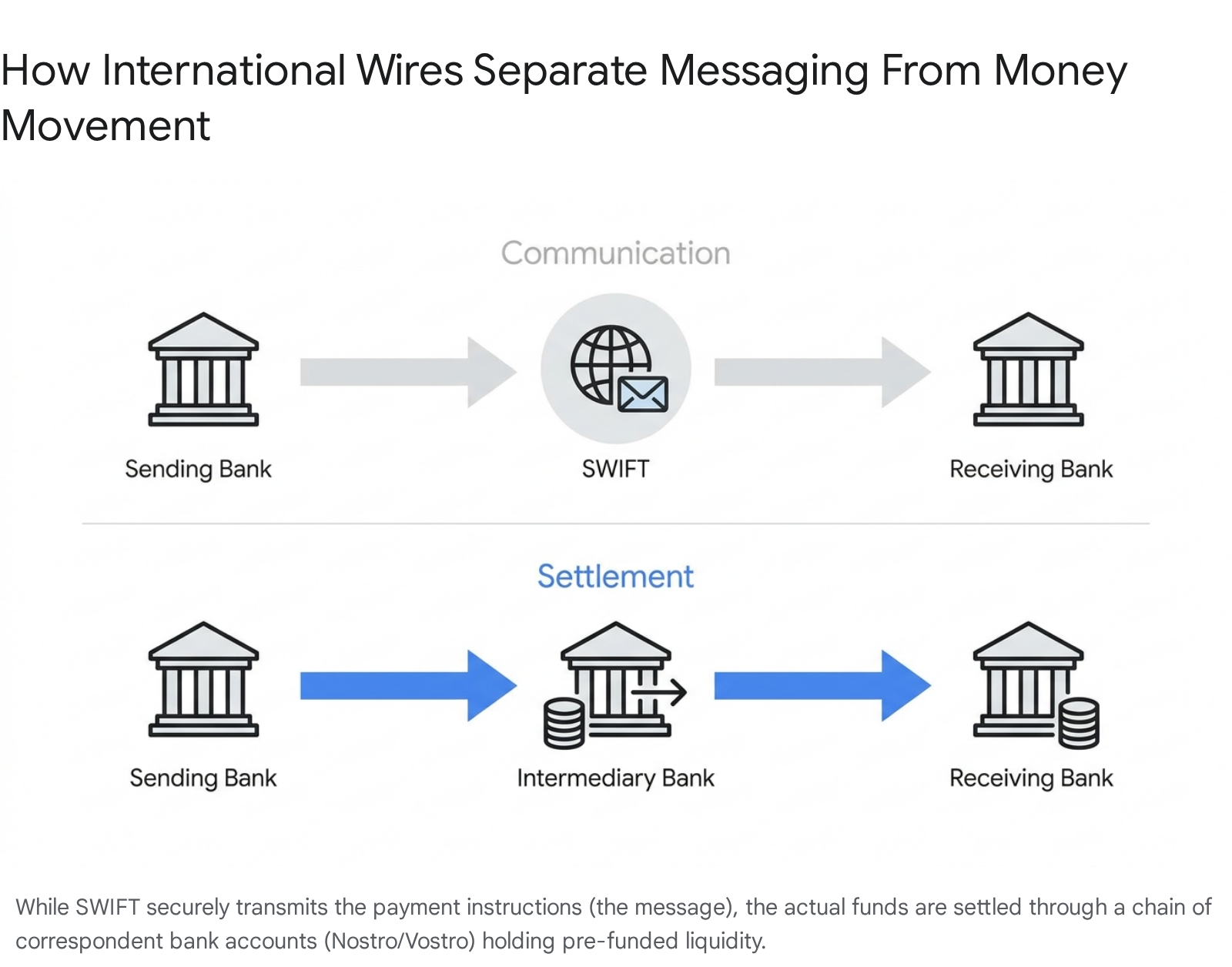

To understand what happens after you click "send" on an international wire transfer, it is necessary to examine the underlying architecture of global finance. Contrary to popular belief, there is no centralized global bank that holds all the world's money, nor is there a universal ledger that automatically connects a sender in New York to a recipient in Tokyo. Instead, the global financial system is a patchwork of thousands of domestic banking networks that do not naturally communicate with one another 12. Moving money between them requires two distinct layers operating in tandem: a communication layer to send the instructions, and a settlement layer to physically move the liquidity 32.

The process begins at the initiation stage. When a sender submits a transfer request, they must provide the sending institution with accurate recipient information, including the full legal name, physical address, and an international bank routing code such as a SWIFT Bank Identifier Code (BIC) or an International Bank Account Number (IBAN) 15. This initiation phase is not merely a formality. Under global regulatory frameworks, including guidelines set by the Financial Action Task Force (FATF), the sending bank is legally required to verify the sender's identity and perform strict Anti-Money Laundering (AML) checks 67.

The bank screens the transaction details against international sanctions lists, such as those maintained by the U.S. Office of Foreign Assets Control (OFAC) or the United Nations, to ensure the funds are not supporting terrorism, organized crime, or sanctioned entities 78. Once the transaction clears these initial domestic compliance hurdles, the sending bank prepares to transmit the payment instruction overseas.

The Role of Correspondent Banking and Nostro/Vostro Accounts

While a digital message carries the instructions, the actual movement of money relies on a centuries-old system known as correspondent banking 39. If a local credit union in the United States wants to send money to a regional bank in the Philippines, it is highly unlikely that these two institutions possess a direct financial relationship. To move the money, they must rely on intermediary banks - massive global financial institutions that hold accounts for both the sending and receiving banks 19.

These correspondent banking relationships are built entirely on a system of Nostro and Vostro accounts 39. "Nostro" is derived from the Latin for "ours," representing an account a domestic bank holds at a foreign bank, denominated in the foreign currency. Conversely, "Vostro" comes from the Latin for "yours," which is how the foreign correspondent bank refers to that exact same account 9. For example, a U.S. bank may hold a Euro-denominated Nostro account at a major correspondent bank in Germany. The German bank views this exact same ledger as a Vostro account holding the U.S. bank's funds.

When the domestic bank needs to send funds abroad, it essentially transfers the payment to its own Nostro account at the correspondent bank. The correspondent bank deducts its service fee from the principal, performs any necessary currency conversions, and then routes the payment to the recipient's bank for final settlement through local clearing channels 29. In instances where the banks operate in highly distinct or emerging markets, the funds may have to pass through two or three separate correspondent banks before reaching their final destination 1011.

Decoding the SWIFT Messaging Network

If correspondent banking is the physical highway over which the money travels, the SWIFT network is the secure radio system used to coordinate the fleet. SWIFT, or the Society for Worldwide Interbank Financial Telecommunication, was established in 1973 to replace the slow and insecure Telex system 3. Today, it connects more than 11,000 financial institutions across over 200 countries and territories, transmitting an average of roughly 42 million messages every single day 313.

A critical distinction that both consumers and financial professionals frequently misunderstand is that SWIFT does not perform any type of settlement. It does not hold funds, nor does it move money 2313. It is exclusively a highly standardized, encrypted messaging protocol. When a bank utilizes SWIFT, it is essentially sending a structured directive to another institution outlining exactly who is getting paid, how much, and through which intermediary accounts the funds should flow 1114.

Understanding Message Types: MT103 and MT202 COV

To ensure that funds are routed accurately across multiple borders without violating international compliance laws, banks rely on distinct categories of SWIFT messages. These are historically known as Message Types (MT). The two most critical messages involved in a standard international wire transfer are the MT103 and the MT202 COV 416.

The MT103 is the Single Customer Credit Transfer. This is the primary payment instruction generated when a sender initiates a wire. It contains comprehensive details regarding the sender, the final beneficiary, the currency, the amount, the date, and the specific purpose of the transaction 41617. For the end consumer or corporate treasurer, the MT103 serves as the ultimate proof of payment, as it represents the finalized instruction to credit the recipient's account.

However, because the sending bank and the receiving bank rarely have a direct relationship, the MT103 alone cannot physically move the money. This is where the MT202 COV - the General Financial Institution Transfer - comes into play 418. While the MT103 carries the customer details and tells the final bank who should receive the money, the MT202 COV is used exclusively for bank-to-bank settlement 1618. It is the message that commands the intermediary correspondent banks to actually shift the underlying liquidity from one Nostro account to another to "cover" the customer's payment 1617.

The Serial and Cover Methods of Routing

Banks generally utilize two distinct methodologies for transmitting these messages across the SWIFT network: the Serial method and the Cover method.

In the Serial method, the MT103 message physically hops from bank to bank in a sequential chain. The sending bank sends the MT103 to the first correspondent bank, which reviews it, processes the settlement, and then forwards a new MT103 to the next bank, continuing until it reaches the final destination 1618. While simple, this method exposes the full customer details to every single intermediary bank in the chain, requiring each one to perform its own time-consuming AML and compliance screening 18.

To expedite the process and maintain greater data privacy, banks frequently use the Cover method. Under this routing strategy, the sending bank transmits the MT103 directly to the final recipient's bank so that they have immediate visibility into the incoming payment 18. Simultaneously, the sending bank fires off an MT202 COV message through the chain of intermediary correspondent banks to execute the actual movement of funds 1618. The MT202 COV explicitly references the original MT103 to ensure the payment can be tracked for compliance purposes, but it strips out the granular customer details to speed up interbank processing 1617. The final receiving bank will only credit the beneficiary's account once both the direct MT103 instruction and the actual funds from the MT202 COV have arrived 18.

The True Cost of Cross-Border Transfers

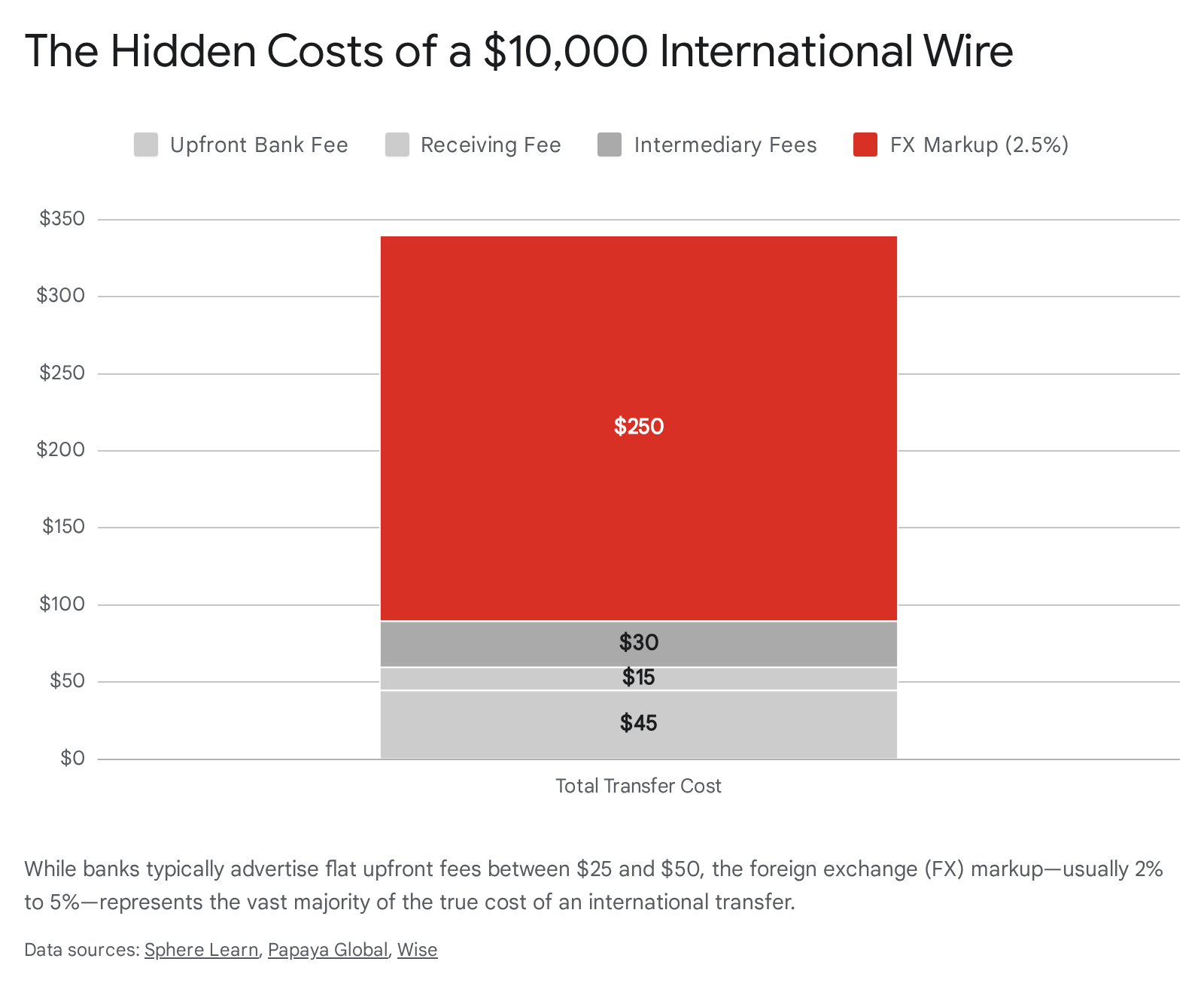

If you ask a corporate Chief Financial Officer or an average consumer what an international wire costs, they will typically quote a number between $25 and $50 19. This is the upfront fee their local bank charges to initiate the transfer. However, financial experts recognize that this sticker price represents only a fraction of the true economic burden. The actual cost of a cross-border wire is heavily fragmented, buried in intermediary deductions, and obscured by opaque currency exchange margins 1920.

According to the World Bank's Remittance Prices Worldwide database, the global average cost of sending remittances in the third quarter of 2025 stood at 6.36% of the principal amount sent 56. Traditional banks remain by far the most expensive service providers in the market, averaging a staggering 14.99% per transaction globally 5. The cost structure driving these massive percentages can be broken down into four distinct layers.

The Four Layers of Wire Fees

The first layer is the initiation fee. This is the transparent, flat rate charged by the sending bank to process the SWIFT message and initiate the compliance checks. In the United States, an outgoing international wire generally incurs a fee of $40 to $50, though some institutions offer lower rates for transfers initiated digitally rather than in a physical branch 1923.

The second layer involves correspondent bank fees. Every time an international wire passes through an intermediary bank on its journey, that institution acts as a tollbooth. Correspondents deduct fees to cover their own operational costs, SWIFT network access, and compliance overhead. These deductions typically range between $15 and $50 per intermediary 2024. Because an international wire might require two or three hops through the correspondent network, these fees aggregate rapidly.

The third, and often most punitive, layer is the foreign exchange (FX) markup. For any wire that involves a currency conversion, the exchange rate spread is almost always the single largest cost component, and the one least likely to be disclosed clearly 197. When a bank converts currencies - for instance, changing U.S. Dollars into Philippine Pesos or Euros - it rarely uses the true "mid-market rate," which is the wholesale rate utilized by large financial institutions trading among themselves. Instead, the bank applies a retail markup, essentially buying the currency at the wholesale price and selling it to the consumer at a premium. This markup typically ranges from 1.5% to 5%, depending on the currency pair and the bank's relationship with the client 19.

To put this economic reality into perspective, consider a concrete business transaction. If a U.S. company wires $100,000 to a supplier overseas, a seemingly small 2% FX markup strips $2,000 of value from the transfer. That hidden spread absolutely dwarfs the visible $45 upfront wire fee, yet it is rarely itemized on a receipt 19.

The final layer is the receiving bank fee. When the funds finally arrive, the recipient's bank may charge an incoming international wire fee simply for accepting the SWIFT message and crediting the final account, which usually ranges from $15 to $25 237.

Who Bears the Cost? The Role of OUR, SHA, and BEN

Because the involvement of correspondent banks makes the final cost of a wire transfer highly unpredictable, the SWIFT network allows the sender to dictate how these fees are allocated using standardized billing codes. The selection of these codes determines exactly how much money will arrive in the destination account 220.

When a sender selects the OUR instruction, they elect to pay all fees associated with the transfer, including their own bank's charges, the intermediary tolls, and the receiving bank's fees. The sender is billed an extra premium upfront, but this code guarantees that the recipient receives the exact, unreduced principal amount 220. This is critical for settling rigid corporate invoices or paying international payroll.

The BEN (Beneficiary) instruction places the entire financial burden on the recipient. Under this code, the sending bank, the intermediary banks, and the receiving bank simply deduct their respective fees from the principal amount as it travels. Consequently, the final amount deposited is noticeably less than the amount originally sent 220.

The SHA (Shared) instruction represents a middle ground and is the default option in many regulatory jurisdictions, including the European Economic Area. With SHA, the sender pays only their own bank's outgoing fee, while the recipient absorbs the incoming fees and any correspondent bank deductions taken mid-flight 220.

Why Do International Wires Take So Long?

In an era where domestic peer-to-peer payments settle in milliseconds, the fact that an international SWIFT wire routinely takes between one and five business days to clear remains a source of immense frustration 18. This delay is rarely a technological failure of the messaging network; rather, it is the byproduct of severe operational friction, regulatory compliance, and fragmented geographical infrastructure.

The Compliance Labyrinth and Anti-Money Laundering Holds

Financial institutions are legally mandated to act as the primary defense against the movement of illicit funds. Every time a wire crosses a sovereign border, it triggers an array of automated Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF) protocols 79.

Regulatory frameworks, such as FATF Recommendation 16, enforce the "Travel Rule." This rule dictates that comprehensive originator and beneficiary data must accompany the electronic transfer through the entire payment chain 78. If a correspondent bank's screening software detects a discrepancy - perhaps the recipient's name bears a phonetic resemblance to a sanctioned individual, or the source of funds appears unusual for the client's risk profile - the transaction is immediately frozen.

These automated holds require manual intervention by a human compliance officer, who must review the transaction, cross-reference documentation, and sometimes request additional invoices or contracts from the sending bank 110. Furthermore, vague descriptions in the payment reference field, such as typing "transfer," "friend," or "invoice," frequently trigger security algorithms, resulting in days of delay while the banks exchange formal inquiries 11. Even minor spelling errors in a beneficiary's name can cause a wire to be held in suspense until the discrepancy is formally resolved 1711.

Time Zones and Batch Processing

The physical routing of the payment also introduces inherent delays. An international wire is not a direct, point-to-point transmission; it is a relay race 11. If a bank in Los Angeles sends funds to a bank in rural Thailand, the payment may route through a New York clearinghouse, pass to a European correspondent bank, and finally land at an Asian intermediary before reaching its destination 19.

Because these institutions operate in vastly different time zones, they adhere to strict daily processing cut-offs. A payment approved in New York late on a Friday afternoon will sit dormant over the weekend and will not be processed by the European correspondent until their business day begins on Monday 11. If any bank in the chain happens to be observing a local national holiday, the entire settlement process halts.

The SWIFT gpi Upgrade: Tracking Money Like a Package

To combat these systemic delays and respond to the rising threat of agile fintech competitors, SWIFT introduced the Global Payments Innovation (gpi) initiative in 2017 330. SWIFT gpi does not replace the traditional correspondent banking model, but it dramatically modernizes its execution by enforcing strict service level agreements among participating banks.

The cornerstone of the gpi upgrade is the Unique End-to-End Transaction Reference (UETR). Much like a tracking number provided by a logistics company such as FedEx or Amazon, the UETR is a mandatory, immutable code attached to the SWIFT message 331. It allows banks, and by extension their corporate clients, to track the exact location of a payment in real time, see precisely which intermediary bank is currently processing it, and view the exact fees being deducted along the route 3.

This visibility has drastically improved processing speeds by holding intermediary banks accountable for delays. Today, major global banks process millions of these modernized messages daily. According to recent data, roughly 50% to 60% of all SWIFT gpi payments are now credited to the end beneficiary within 30 minutes, and nearly 100% complete their journey within 24 hours - a vast improvement over the historical multi-day waiting period 331. Furthermore, pre-validation tools integrated into the gpi framework allow banks to verify account details before the payment is sent, drastically reducing the number of wires that bounce back due to incorrect formatting 31.

Traditional Banks vs. Fintech Disruptors

The historical inefficiencies of the SWIFT network paved the way for a massive boom in financial technology (fintech) companies specializing in cross-border payments. Platforms such as Wise, Airwallex, Remitly, and various digital-first Money Transfer Operators (MTOs) have fundamentally re-engineered how capital moves, aggressively capturing market share from traditional banks 83334.

Rather than relying on the expensive, multi-hop correspondent banking network to move funds individually, these fintech innovators generally utilize a localized peer-to-peer netting model 1236.

When a user wants to send $1,000 from the United States to the United Kingdom via a platform like Wise, the underlying capital does not actually cross the Atlantic Ocean. Instead, the user deposits $1,000 via a domestic ACH transfer into the fintech's U.S.-based bank account. The fintech's software registers the deposit, locks in the live mid-market exchange rate, and instantly sends a digital command to its European subsidiary. The fintech's UK bank account then utilizes local domestic rails (such as the UK's Faster Payments system) to pay out the equivalent amount in British Pounds directly to the recipient 1236.

By maintaining vast, pre-funded pools of liquidity in local bank accounts across dozens of countries, these platforms completely bypass the SWIFT intermediary network. This eliminates unpredictable correspondent fees, allows the provider to offer the genuine mid-market exchange rate without a retail markup, and frequently settles transactions in a matter of seconds rather than days 81237.

The Rise of Stablecoins and Blockchain Rails

Beyond centralized fintech platforms, blockchain technology is rapidly emerging as an alternative infrastructure for global remittances. Operating outside the legacy banking system entirely, cryptocurrency exchanges and digital wallets allow users to transmit value using stablecoins - digital assets pegged to fiat currencies, such as USDC or USDT 13.

When executed on low-fee blockchain networks like Tron or Ethereum Layer-2 protocols, stablecoin transfers can settle globally in under a minute, with transaction costs frequently falling below $1.00 13. For remittance flows in emerging markets, this represents a monumental shift. However, the true cost of blockchain remittances must factor in the "on-ramp" and "off-ramp" fees required to convert fiat currency into crypto and back again, which can vary wildly depending on local regulatory environments and exchange liquidity 13. Furthermore, blockchain transfers require a degree of technological fluency and digital wallet infrastructure that many traditional remittance senders lack 39.

Comparing the Options

The decision between a traditional bank wire and a fintech platform ultimately depends on the size of the transaction, the specific geographic corridor, and the user's requirement for systemic certainty 40.

| Feature | Traditional Bank Wire (SWIFT) | Fintech Platforms (e.g., Wise, Airwallex) | Stablecoin/Blockchain |

|---|---|---|---|

| Average Transfer Speed | 1 to 5 business days 108 | Minutes to 2 business days 83613 | Seconds to minutes 13 |

| Upfront Fees | $25 - $50 flat fee 1923 | Varies (often percentage-based, ~0.5%) 836 | Network gas fees (<$1 to $10+) 13 |

| Exchange Rate | Retail rate (2% - 5% hidden markup) 19 | Mid-market rate (no markup) 1237 | Near 1:1 for pegged stablecoins 13 |

| Intermediary Bank Fees | Yes, deducted mid-flight 20 | No, bypassed via local accounts 12 | No |

| Best Use Case | Massive B2B invoices, property purchases, $100k+ wires 140 | Consumer remittances, SME payroll, sub-$50k wires 3340 | Tech-savvy users, high-frequency micro-remittances 13 |

Despite the obvious cost and speed advantages of fintechs for consumers and small businesses, traditional bank wires remain the gold standard for massive, complex B2B operations. Traditional banks offer irrevocable settlement finality, the ability to process multi-million dollar transactions without stringent daily caps, and the established regulatory compliance required for major corporate acquisitions or trade finance 13340.

Major Remittance Corridors and Regional Regulations

The mechanics of a wire transfer are heavily influenced by the specific countries involved. A transfer pathway between two nations is known as a "corridor," and each corridor is governed by distinct geopolitical and regulatory realities 14.

The US-Mexico Corridor

The flow of capital from the United States to Mexico represents the single largest bilateral remittance corridor in the world 4243. In 2024, Mexico received a record-breaking $64.7 billion in remittances, the vast majority originating from Mexican workers residing in the U.S. 144243. This massive influx of capital is critical to the Mexican economy, accounting for roughly 3.7% to 5% of the nation's GDP and supporting an estimated 1.8 million households 1443.

The infrastructure supporting this corridor is highly digitized. Nearly all formal remittance payouts in Mexico run through SPEI (the Interbank Electronic Payment System), a real-time gross settlement network operated by the Banco de México 42. Despite the immense volume and sophisticated infrastructure, the cost of sending money to Mexico remains sticky. The average fee for a $200 transfer hovers just below 5% of the total value 1442. This elevated cost is largely sustained by the heavy reliance on cash-pickup networks on the Mexican side, as well as the complex licensing requirements that insulate incumbent Money Transfer Operators (MTOs) from aggressive price competition 42.

European Union: PSD3 and Open Banking

In Europe, the regulatory landscape is shifting aggressively toward transparency and consumer protection. The European Commission is currently finalizing a major overhaul of its financial rules through the Third Payment Services Directive (PSD3) and the accompanying Payment Services Regulation (PSR), which are expected to be formally adopted by late 2025 and implemented by member states shortly thereafter 444546.

PSD3 aims to harmonize the European payment ecosystem and crack down on hidden fees. Under the new framework, Payment Service Providers (PSPs) will be legally required to present customers with clear, upfront information regarding all charges - including explicit disclosures of currency conversion markups and fixed ATM withdrawal fees - before a cross-border transfer is initiated 4415.

Furthermore, PSD3 radically strengthens anti-fraud measures. It mandates an EU-wide "Confirmation of Payee" system, requiring banks to verify that the name provided by the sender exactly matches the registered name on the recipient's IBAN 4445. Crucially, if a bank fails to deploy these robust authentication measures and a consumer falls victim to a spoofing scam, the financial institution will be held legally liable for reimbursing the full loss 4445. This directive runs parallel to the SEPA Instant mandate, which requires eurozone banks to process Euro-denominated transfers within 10 seconds, 24/7, fundamentally altering the speed of intra-European commerce 1315.

India: The Liberalised Remittance Scheme (LRS)

Governments also utilize wire transfer regulations defensively, restricting capital outflows to maintain macroeconomic stability. In India, the Reserve Bank of India (RBI) strictly regulates the outward flow of funds through the Liberalised Remittance Scheme (LRS) 164917.

Introduced in 2004 with a modest ceiling of $25,000, the LRS has evolved to permit resident Indian individuals to freely remit up to $250,000 USD per financial year for permissible current or capital account transactions 161751. This quota covers a broad spectrum of activities, including overseas education, medical treatment, tourism, purchasing foreign property, and investing in global equity markets 164952.

However, wiring money out of India has become increasingly complex due to aggressive taxation policies. Under recent Union Budget updates, the Indian government mandates Tax Collected at Source (TCS) on LRS transactions. As of 2025, remittances exceeding a threshold of ₹10 lakh in a financial year are subject to an upfront tax. While remittances funded by authorized education loans incur no TCS, and standard education or medical transfers incur a 2% tax, other outward transfers - such as investments or overseas tour packages - can attract significantly higher TCS rates up to 20%, depending on specific stipulations 5152. While TCS is an advance tax that can eventually be claimed as a credit against income tax liabilities, it requires senders to lock up significant additional capital upfront when executing an international wire 16.

The ISO 20022 Migration: Rewriting the Language of Money

The most profound structural change to international wire transfers in half a century is happening right now: the global migration to the ISO 20022 financial messaging standard. This transition is not merely a software update; it is a fundamental rewriting of the language banks use to communicate 5354.

For decades, the SWIFT network has relied on legacy MT formats. These older messages are built on rigid, free-text fields with severe character limits 5455. For example, if a sender inputs a recipient's address in an MT message, they might type "John Doe, 123 Cuba Street, London" into a single, unstructured text block. Because the legacy system cannot semantically distinguish between a street name and a sovereign nation, automated AML algorithms frequently flag the word "Cuba," freezing a perfectly legal payment to the UK on suspicion of sanctions evasion 56. This unstructured data is a primary driver of false-positive compliance alerts, which cost the banking industry billions in manual investigation hours and delayed liquidity 56.

ISO 20022 solves this by replacing the antiquated text blocks with an XML-based language (specifically, the pacs.008 message for customer credit transfers) that categorizes data into highly structured, machine-readable fields 545558. Under ISO 20022, the town name, the street name, the building number, and the country code all have their own distinct, mandatory data tags. A machine can instantly recognize that "Cuba" is a street in London, not the sanctioned country 56. By drastically enriching the payload - expanding the data capacity from roughly 100 characters to nearly 9,000 - ISO 20022 allows comprehensive invoice details, purpose codes, and compliance data to travel alongside the payment seamlessly 5455.

The Hard Deadlines: 2025 and 2026

This migration is a monumental undertaking, requiring global banks to overhaul legacy middleware, payment gateways, and back-office reconciliation systems 5318. Because the transition is so complex, SWIFT initiated a "coexistence period" in March 2023, allowing institutions to process both old MT messages and new ISO 20022 messages simultaneously 58.

However, this grace period is rapidly drawing to a close, driven by two non-negotiable regulatory deadlines 19:

- November 2025: The MT/ISO 20022 coexistence period officially ends for cross-border payment instructions. From this date forward, SWIFT will no longer support the legacy MT formats for these core transfers. Financial institutions must be capable of sending and receiving native ISO 20022 messages to ensure end-to-end interoperability and prevent critical data from being truncated or lost as it crosses borders 5458.

- November 2026: The unstructured address ban takes effect. Any cross-border payment instruction sent over the SWIFT network that relies on a fully unstructured postal address will be outright rejected by the system. Financial institutions and corporate treasuries must provide either a fully structured address or a hybrid address containing, at minimum, a designated town and country field 1819.

The adoption of this standard is accelerating rapidly. By early 2026, the SWIFT network aims to have the vast majority of its cross-border traffic running natively on ISO 20022, effectively standardizing the data flow for the global economy . Beyond merely streamlining compliance and reducing costly payment exceptions, ISO 20022 is viewed as the foundational infrastructure required to integrate traditional banking rails with next-generation technologies, including real-time domestic clearing networks, tokenized deposits, and Central Bank Digital Currencies (CBDCs) 5354.

Bottom line

Sending money to another country initiates a complex, multi-layered reaction across the global financial system. While the actual payment instructions traverse the secure SWIFT messaging network, the physical funds must navigate a labyrinth of correspondent banking accounts, triggering opaque intermediary fees, significant foreign exchange markups, and stringent anti-money laundering holds. However, the landscape is modernizing rapidly. The rise of SWIFT gpi and localized fintech platforms has drastically reduced transfer times and costs, while the ongoing global migration to the structured ISO 20022 data standard promises to eliminate the operational friction that has plagued international wires for decades.