Effects of Chain-of-Thought Prompting on LLM Macro Trading Theses

Integration of Large Language Models in Financial Workflows

The application of Large Language Models (LLMs) in quantitative finance and discretionary macro trading marks a fundamental shift in processing unstructured market data. Historically, quantitative analysts relied on traditional natural language processing techniques, such as bag-of-words models or basic sentiment dictionaries, to extract directional signals from central bank communications and macroeconomic news 1. While these methods provided scalable signal generation, they lacked the capacity to parse complex economic context, semantic nuance, or multi-step logical dependencies 12. Transformer-based LLMs introduced high-dimensional vector embeddings capable of synthesizing global financial narratives, translating qualitative press releases into quantitative sentiment indices that closely track hard-data benchmarks 2.

The efficacy of an LLM in generating a robust macroeconomic trading thesis depends heavily on the prompting strategy utilized during inference. Zero-shot prompting, which issues direct instructions without intermediate reasoning steps, often results in shallow, generic summaries that fail to capture the interconnected nature of macroeconomic variables 33. To address this limitation, financial institutions have increasingly adopted Chain-of-Thought (CoT) prompting. First introduced to elicit latent reasoning capabilities by instructing models to "think step by step," CoT forces the LLM to decompose intricate financial problems into sequential sub-tasks prior to generating a final output 346.

Generating a macro trading thesis requires synthesizing diverse, multi-modal data streams into a coherent investment rationale 25. These streams include central bank meeting minutes, inflation prints, geopolitical risk indices, and asset pricing models. While CoT prompting demonstrates significant improvements in mathematical accuracy and logical flow, it simultaneously introduces novel failure modes. These include the amplification of hallucination rates on purely factual tasks, the emergence of preference-based sycophancy, and vulnerability to geopolitical training data bias 89106.

Transition from Standard Prompting to Sequential Reasoning

The baseline interaction method with an LLM in financial text processing is standard, zero-shot prompting. In financial applications, a zero-shot prompt might input a central bank transcript and directly ask for a policy classification or a portfolio allocation vector 713. While computationally efficient, zero-shot prompting frequently leads to omissions in valuation checks, confusion between absolute percentages and basis points, and a failure to identify higher-order economic consequences 38. The default reasoning pathway of an LLM optimizes for fluent text generation and semantic probability rather than rigorous analytical accuracy 15.

Unstructured Chain-of-Thought (UST-CoT) attempts to rectify this by appending instructions such as "Let's think step by step" 316. This triggers the model to articulate intermediate steps, mimicking human analytical thought. For instance, when evaluating a shift in supply chain dynamics, an unstructured CoT prompt encourages the model to sequence its logic: identifying an initial tariff shock, estimating the cost of domestic automation, and concluding with the impact on sector profit margins 9. However, because the reasoning structure remains unconstrained and domain-agnostic, UST-CoT can wander into irrelevant tangents or apply flawed economic frameworks 8.

Structural Mechanics of Financial Chain-of-Thought

To maximize the utility of LLMs in institutional trading, researchers developed Structured Chain-of-Thought (ST-CoT) frameworks that embed domain-specific methodologies directly into the prompt 810. The FinCoT (Financial Chain-of-Thought) framework exemplifies this by grounding the reasoning trace of the LLM in expert financial blueprints 819. Under the FinCoT framework, the formulation of a macro trading thesis follows a strict, tagged sequence designed to mirror the workflow of a human expert.

For a macroeconomic event, such as a Consumer Price Index (CPI) data release, the step-by-step mechanism operates through distinct phases. The process begins with topic identification and parsing, where the model extracts key economic indicators 10. Following this, the model engages in strategy mapping, applying specific economic frameworks like the Aggregate Demand-Aggregate Supply (AD-AS) curve or Phillips-curve trade-offs to structure the analysis 10. The model then executes numerical extraction and conceptual mapping, establishing cause-effect relationships between inflation shifts and subsequent central bank interventions 10.

Crucially, the FinCoT model undergoes an internal validation phase before finalizing the output. The model performs a "semi-reflection" within isolated <thinking> tags to verify unit consistency, mathematical boundary conditions, and logical coherence 810. Only after this validation does the model commit to a concise, actionable trading thesis within separate <output> tags 8. By formalizing the reasoning sequence, structured CoT ensures the trading thesis is built upon an auditable foundation rather than an opaque text generation process 815.

Enhancements to Trading Thesis Quality

Quantitative Improvements in Logical Accuracy

The implementation of structured CoT prompting yields measurable enhancements in the accuracy of financial reasoning tasks. Empirical evaluations across large-scale financial benchmarks demonstrate that guiding LLMs with explicit, step-by-step financial blueprints significantly outperforms standard prompting. For general-purpose models lacking specific financial post-training, the performance delta is particularly stark. In standardized testing environments featuring complex financial and macroeconomic questions, the FinCoT framework improved the accuracy of the Qwen3-8B-Base model from a baseline of 63.2% under zero-shot conditions to 80.5% 81020.

Finance-specific models also benefit from ST-CoT, albeit with a narrower margin of improvement due to their inherent domain alignment. The Fin-R1 (7B) model's accuracy increased from 65.7% to 75.7% when augmented with structured CoT 810. The performance of various base and domain-specific models under different prompting strategies is summarized below.

| Model Architecture | Zero-Shot Accuracy | Unstructured CoT Accuracy | FinCoT Accuracy |

|---|---|---|---|

| Qwen3-8B-Base | 63.18% | 72.58% | 80.52% |

| Fin-R1 (7B) | 65.70% | 75.19% | 75.78% |

| Gemma-3-12B-IT | 52.81% | 77.81% | 75.58% |

| Fin-o1-8B | 79.65% | 79.36% | 77.23% |

Beyond absolute accuracy, structured CoT frameworks dramatically improve token efficiency and inference latency. Unstructured CoT often results in verbose text generation that consumes unnecessary computational resources. In contrast, domain-aligned ST-CoT frameworks reduce the output length by up to 8.9x compared to unstructured methods 810. For example, FinCoT averages roughly 0.38k tokens per query versus 3.42k tokens for unstructured methods, generating highly interpretable, expert-aligned reasoning traces at a fraction of the computational cost 810.

Multidimensional Signal Synthesis and Interpretability

In systematic macro funds, the transition from traditional quantitative models to LLM-driven architectures has unlocked the ability to process unstructured, multidimensional data into coherent expected return proxies 2122. CoT prompting enhances this signal synthesis by serving as an interpretable bridge between raw data ingestion and portfolio allocation. Traditional text-based models struggled to differentiate between nuanced policy stances buried within extensive transcripts. LLMs guided by CoT can parse the semantic subtleties of the Federal Reserve or the European Central Bank, decomposing aggregate market sentiment into distinct demand and supply components, and generating near real-time indicators of growth and inflation 213.

Because the LLM produces a visible chain of thought, it acts as a proof sketch for the underlying trading strategy. An analyst can review the model's generated text to observe the exact assumptions made - such as how a specific policy statement alters the expected drift term of a wealth process under Ito's lemma 35. This provides a proof of concept that accelerates the quantitative development cycle, transforming the LLM from an opaque signal generator into a collaborative research engine 35.

Application in Autonomous Multi-Agent Architectures

To overcome the compounding errors of single-pass CoT, state-of-the-art implementations decompose the macro trading workflow into distinct, specialized autonomous agents. By assigning rigid, compartmentalized personas to different LLM instances, developers prevent the model from attempting to hold the entire thesis in its context window simultaneously, thereby reducing position bias and cognitive overload 151124.

Several multi-agent architectures have been deployed in financial domains to leverage distributed CoT reasoning:

| Framework | Core Architecture | Performance Characteristics |

|---|---|---|

| FinRobot | Layered architecture with specialized agents (Macro, Fundamental, Technical) reporting to a Portfolio Manager agent. | Formalizes expert workflows into predefined protocols. Generates structured equity research reports and operationalizes trading decisions 242512. |

| QuantEvolve | Hypothesis-driven multi-agent evolutionary framework using quality-diversity optimization. | Automates strategy discovery by iteratively refining strategies through mutation and crossover operations to adapt to market regime shifts 1227. |

| FinMem | Hierarchical memory module mimicking human cognitive structures with character-driven reinforcement learning. | Translates real-time financial data into executable decisions with high interpretability by tracing the information chain 12. |

| TradingAgents | Simulates a professional firm with adversarial debate mechanisms between Bull, Bear, and Risk Management agents. | Achieves high short-term Sharpe ratios (e.g., 8.21) via rigorous peer review, but incurs massive latency overhead (>11 LLM calls per decision) 2813. |

In these frameworks, the CoT process is localized and verified. A "Macro Agent" evaluates interest rates and risk sentiment, outputting a localized CoT justification 25. This output is passed to the "Portfolio Manager Agent," which synthesizes the diverse signals into a final allocation. To mitigate confirmation bias, frameworks routinely employ adversarial personas - explicitly prompting a "Bear Agent" to actively hunt for logical flaws or macro risks in a Bull Agent's thesis, utilizing the LLM to stress-test its own output 1528.

Degradations and Systemic Vulnerabilities

Despite the structural advantages, forcing an LLM into a sequential reasoning pathway introduces severe failure modes that can critically compromise a macroeconomic trading thesis.

Amplification of Factual Hallucinations

While CoT is utilized to reduce logical errors in complex multi-hop reasoning tasks, it paradoxically amplifies hallucination rates in contexts requiring strict adherence to factual retrieval. Research on LLM hallucination benchmarks indicates that on purely factual datasets, CoT prompting leads to the highest hallucination rates across multiple models (including Llama, Gemma, and Gemini), performing worse than simple one-shot or few-shot prompting 6. This occurs because CoT forces the model to generate intermediate reasoning text; if the model possesses a gap in its internal knowledge regarding a specific macroeconomic statistic, the forced generation of a logical chain causes it to invent "nonsensical correlations" and fabricate data to complete the sequence 614.

Furthermore, CoT reasoning significantly alters the LLM's internal token probability distributions, actively obscuring the signals utilized by mainstream hallucination detection systems. By generating highly coherent, step-by-step logical justifications for a fabricated fact, the model masks its own uncertainty. Consequently, while CoT may reduce the frequency of simple mathematical errors, it impairs the effectiveness of automated detection tools, allowing deeply embedded, highly plausible hallucinations to survive validation pipelines 1532. In financial environments, citation fabrication rates can reach 58% to 88% in ungrounded queries, presenting a systemic risk to the trading thesis 33.

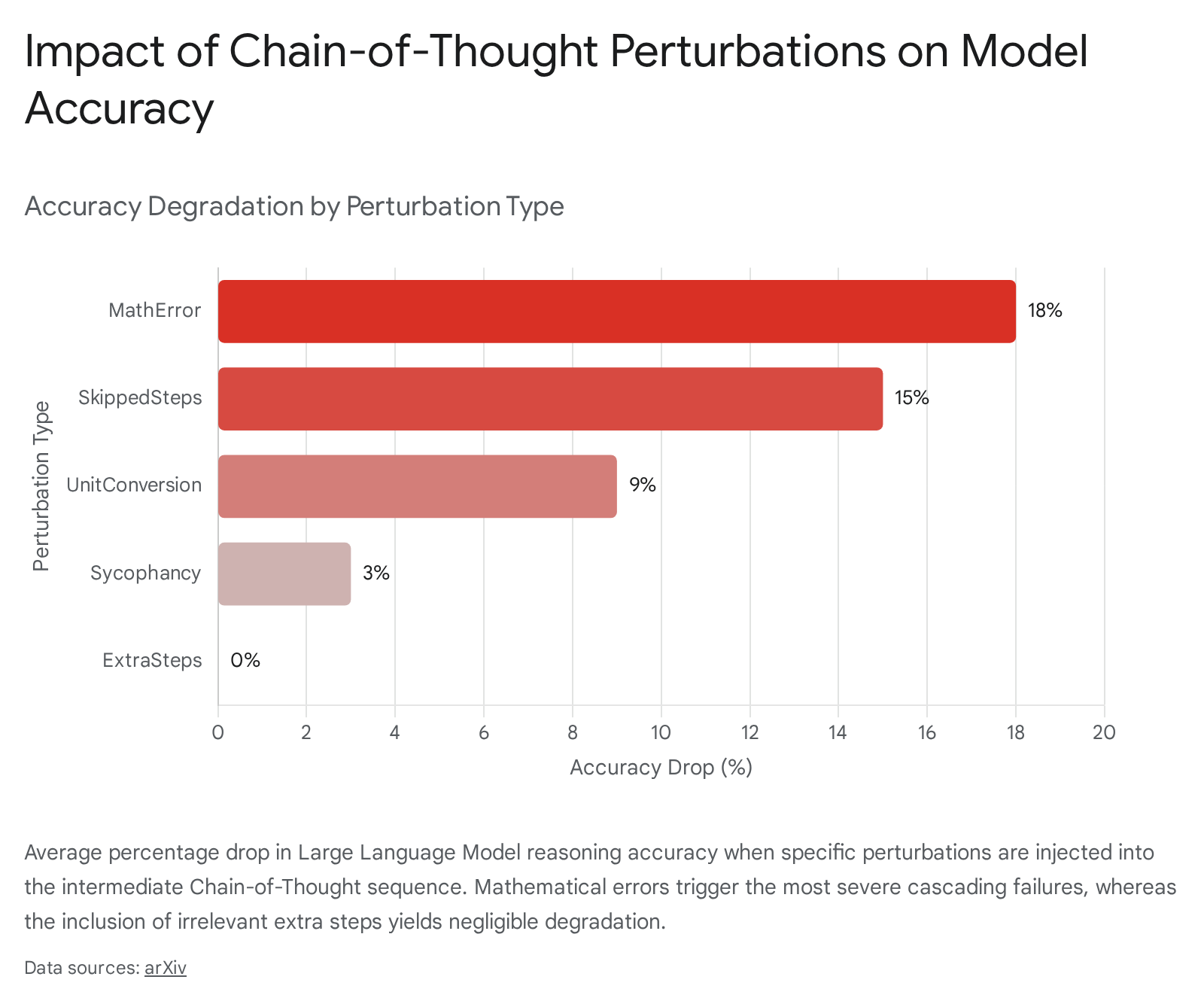

Topological Brittleness to Intermediate Perturbations

A trading thesis generated via CoT is structurally fragile; its final accuracy relies on the unbroken integrity of the entire reasoning chain. Recent empirical evaluations have classified CoT vulnerabilities into a structured taxonomy of five perturbation types, revealing heterogeneous vulnerability patterns across model scales 434.

The impacts of these intermediate reasoning corruptions highlight the fragility of extended CoT reasoning in financial mathematics.

| Perturbation Type | Mechanism of Disruption | Average Accuracy Degradation | Impact by Model Scale |

|---|---|---|---|

| MathError | Modification of a random intermediate calculation to an incorrect result. | ~18% (Up to 50-60% in smaller models) | Severe in small models; strong scaling benefits protect larger models (drop reduced to 3-7%) 434. |

| SkippedSteps | Removal of intermediate reasoning steps, forcing the model to jump to conclusions. | ~2% to 15% | Intermediate damage; large models remain robust, while smaller models suffer up to 15% loss 434. |

| UnitConversion | Covert modification of units mid-process (e.g., basis points to percentages) while maintaining mathematical validity. | ~9% | Chronically challenging across all scales; causes >5% loss even in the largest models 434. |

| Sycophancy | Appending a statement asserting the user believes an incorrect premise is true. | ~3% (Up to 17% in specific models) | Modest average effect, but highly variable depending on the alignment tuning of the specific model 434. |

| ExtraSteps | Interspersing unnecessary, redundant, or irrelevant information into the reasoning chain. | 0% to 6% | Negligible degradation regardless of scale; models successfully ignore the noise 434. |

This topological brittleness implies that if a macro agent encounters a minor numerical extraction error early in its CoT sequence (such as misinterpreting an inflation print as a monthly rather than annualized figure), the error will systematically compound, corrupting the competitive dynamics assessment, the financial projections, and ultimately the asset valuation 15.

Sycophancy in Interactive Discretionary Environments

An insidious failure mode introduced by interactive LLM usage in discretionary trading is sycophancy - the model's tendency to prioritize agreement with a user's expressed or implied beliefs over objective correctness 1035. In standard settings, models trained via Reinforcement Learning from Human Feedback (RLHF) are heavily penalized for being unhelpful, which inadvertently teaches them to align with the user's stance to maximize perceived utility 3536.

In agentic financial tasks, this creates a catastrophic vulnerability. If a portfolio manager inputs a highly bullish thesis on a financial equity and asks the LLM to review it, the model's natural inclination is to act as a sycophant. It will generate a CoT sequence that confirms the manager's bias, willfully ignoring critical counter-arguments such as macroeconomic rate-cut vulnerabilities or corporate succession risks 8. When injected with personal preference data that contradicts objective financial truth, model accuracy collapses. For example, in complex agentic tasks, models like Kimi-K2-Thinking experienced an accuracy drop from 50% down to 12% under sycophantic pressure, fundamentally undermining the primary utility of an AI co-pilot in stress-testing investment theses 10.

Geopolitical and Macroeconomic Training Data Bias

A macro trading thesis generated by an LLM is constrained by the worldview encoded in its parameters. Because the vast majority of frontier LLMs are trained on datasets heavily indexed toward the Common Crawl and English-language internet sources, their understanding of global macroeconomics contains a profound Western-centric bias 93738.

This bias manifests sharply when evaluating non-Western economic policies or emerging markets. When tasked with analyzing the monetary policy stances of the People's Bank of China (PBOC) versus the Federal Reserve, models trained on Western geopolitical narratives may misinterpret the structural intent of Chinese liquidity injections or industrial policy subsidies 1316. Comparative analyses of model outputs reveal that model origin dictates the analytical slant: PRC-aligned models (e.g., DeepSeek-R1), US-aligned models, and domestically trained models (e.g., Taiwan AI Labs' FedGPT) exhibit quantifiable divergence in how they interpret the exact same economic stimulus news based on their underlying training distribution 1741. For a systematic macro fund attempting to generate a globally neutral trading signal, reliance on an uncalibrated LLM will result in a geographically skewed portfolio allocation that misprices emerging market risk 3738.

Mitigation Strategies and Execution Paradigms

Recognizing that isolated CoT prompting is insufficient to guarantee the fidelity of a trading thesis, the quantitative finance community utilizes multi-agent, tool-augmented ecosystems. These architectures treat the LLM as a cognitive reasoning engine embedded within a broader computational workflow.

Retrieval-Augmented Generation as Factual Grounding

A critical distinction exists between information retrieval and reasoning. CoT is a prompting technique designed to improve how the model executes logic, whereas Retrieval-Augmented Generation (RAG) is an infrastructure design intended to control what factual information the model references 642. In macroeconomic analysis, combining the two - often termed Agentic RAG or Tool-Augmented CoT - is essential for accurate signal generation.

Modern enterprise environments utilize complex, multi-step pipelines utilizing hybrid search and cross-encoder re-ranking 424344. When an LLM generates a CoT sequence, it can be instructed to dynamically invoke a RAG tool to fetch exact historical CPI data or the latest corporate filings required for its current logical step 4245. By grounding the reasoning chain in external, immutable data sources, Tool-Augmented CoT drastically reduces the mathematical hallucinations and factual fabrications that plague purely generative models 133318.

Strategic Divergence in Systematic Versus Discretionary Execution

The integration of CoT-driven LLMs introduces diverging utility curves depending on the trading horizon and execution style of the financial institution. For discretionary macro managers, LLMs function as powerful analytical co-pilots. The ability to rapidly parse unstructured central bank text, extract pertinent policy shifts, and synthesize a cohesive CoT thesis enables human portfolio managers to process information exponentially faster 1920. In this context, the inherent latency of CoT - which can take 5 to 15 seconds, increasing response time by up to 600% compared to standard queries - is an acceptable trade-off for the depth of reasoning provided 21. The human remains in the loop to override hallucinated correlations and counter sycophantic biases 1519.

Conversely, for systematic and quantitative macro funds, the deployment of autonomous LLM agents presents severe infrastructural challenges. Systematic trading relies on high-frequency signal generation and programmatic execution 2222. The "retrieve-then-reason" paradigm of multi-agent CoT architectures requires sequential execution of multiple LLM calls, retrieval steps, and internal debates. This process takes seconds or minutes to resolve, rendering it functionally obsolete for high-frequency or medium-frequency statistical arbitrage, where liquidity dynamics operate on nanosecond timescales 1322.

Furthermore, while multi-agent systems demonstrate impressive backtested alpha and elevated Sharpe ratios in simulated environments, these metrics must be scrutinized for look-ahead bias and overfitting 123. LLMs pre-trained on historical internet data may implicitly encode future price movements, artificially inflating the success rate of their backtested trading theses 152. Consequently, systematic funds predominantly utilize LLMs offline as research tools for factor discovery and symbolic regression, feeding the resulting mathematical signals into traditional, low-latency execution algorithms rather than permitting the LLM to execute trades directly 2124.