The Relationship Between Income and Happiness

The relationship between financial wealth and subjective well-being constitutes a foundational inquiry spanning behavioral economics, psychological science, and public policy. Historically, empirical research has yielded seemingly contradictory findings regarding whether increased income corresponds to continuous, indefinite improvements in human happiness, or whether well-being reaches a point of satiation beyond which additional wealth yields marginal or zero psychological returns. Recent methodological advancements, the utilization of massive global datasets, and adversarial collaborations between leading scholars have largely resolved these longstanding contradictions.

The current scientific consensus outlines a highly nuanced relationship: the conversion of financial wealth into psychological well-being is fundamentally moderated by baseline emotional health, the logarithmic scaling of money, international economic development levels, and the precise psychological mechanisms governing how money is deployed in daily life. This report synthesizes the contemporary literature, detailing the divergence between evaluative and experienced well-being, resolving the income satiation debate, mapping global macroeconomic parameters, and outlining the cognitive mechanisms that dictate the emotional utility of income.

Foundations of Well-Being Measurement

To interpret the extensive literature on income and happiness accurately, it is necessary to decouple the broad umbrella term "happiness" into two distinct, rigorously defined psychological constructs. Research relies heavily on this bifurcation, as the two metrics exhibit entirely different sensitivities to income variations, life events, and socioeconomic status 123.

Evaluative Well-Being and Experienced Well-Being

The first construct is evaluative well-being, frequently referred to in the literature as life satisfaction or life evaluation. Evaluative well-being represents a cognitive, reflective assessment of one's life as a whole 12. It is most frequently measured using Cantril's Self-Anchoring Scale (the Cantril Ladder), wherein respondents imagine a ladder numbered from zero (representing the worst possible life for them) to ten (representing the best possible life) and identify their current standing 45. Across virtually all global literature, evaluative well-being demonstrates a robust, continuous correlation with income, rising steadily as income increases without any definitive global plateau 136.

The second construct is experienced well-being, also known as emotional or hedonic well-being. This metric captures the affective quality of an individual's everyday experience - the frequency and intensity of distinct positive emotions (e.g., joy, fascination, affection, amusement) and negative emotions (e.g., sadness, anger, anxiety, stress) 147. Experienced well-being is typically measured via self-reporting of emotions felt during the preceding day or, more recently, through real-time experience sampling via mobile applications 23. The extensive academic debate regarding an "income ceiling" on happiness is almost exclusively constrained to this affective dimension.

Logarithmic Income Scaling and Marginal Utility

Furthermore, economists and psychologists consistently analyze income through a logarithmic transformation ($\log(\text{income})$) rather than utilizing raw monetary units. A linear association between well-being and $\log(\text{income})$ dictates that equivalent proportional increases in income yield equivalent absolute increases in happiness 79.

For example, a 10 percent raise produces the same incremental gain in well-being for an individual earning $30,000 annually as it does for an individual earning $150,000 79. Consequently, the marginal utility of each additional dollar diminishes exponentially. While a linear association with log income implies that a true mathematical plateau is never reached, it requires exponentially vaster sums of raw capital to achieve the same incremental unit of happiness at the upper bounds of the income distribution 78.

Methodological Divergence in North American Data

The contemporary debate surrounding income satiation was anchored for over a decade by two landmark studies focusing on United States residents. These studies reached entirely conflicting conclusions regarding the limits of emotional well-being. The eventual resolution of this conflict required an unprecedented adversarial collaboration that redefined standard practices in behavioral science data analysis.

The 2010 Retrospective Analysis

In 2010, researchers analyzed over 450,000 responses from the Gallup-Healthways Well-Being Index. This study identified a clear, sharp divergence between the two well-being constructs. The findings demonstrated that while life evaluation rose continuously with log income across all measured brackets, experienced well-being ceased to improve beyond an annual household income of approximately $75,000 (in 2008 United States Dollars) 14.

The data revealed that low income severely exacerbated the emotional pain associated with routine negative life events and misfortunes, such as divorce, disease, asthma, and loneliness 1. Poverty acted as a powerful amplifier for everyday misery. Conversely, incomes above the $75,000 threshold did not correlate with any further increases in daily positive affect, nor did they provide any further reduction in daily negative affect 4. The conclusion drawn was that high income buys life satisfaction, but not daily emotional happiness; beyond a certain threshold of stable income, individuals' emotional well-being is constrained entirely by temperament and life circumstances rather than financial capital 4.

The 2021 Real-Time Experience Sampling

A decade later, a 2021 study fundamentally challenged the plateau hypothesis. Utilizing a custom smartphone application designed for experience sampling ("Track Your Happiness"), the methodology collected over 1.7 million real-time reports from 33,391 employed adults in the United States 27. Unlike the 2010 methodology, which relied on retrospective memory of the previous day, the 2021 study captured emotions in the exact moment they were felt on a continuous scale, minimizing memory bias 3.

The findings indicated a continuous linear-log relationship for both evaluative and experienced well-being, displaying an equally steep slope for high earners as for low earners 23. There was no statistical evidence of a plateau around $75,000. In fact, regression results showed that the slope of the association between log income and experienced well-being was virtually identical for incomes below $80,000 ($b = 0.109$) as it was for incomes above $80,000 ($b = 0.110$) 3. Larger incomes correlated robustly with both significantly higher levels of positive affect and significantly lower levels of negative affect across the entire measured income spectrum 39.

Resolution Through Adversarial Collaboration

To reconcile the fundamentally incompatible findings - a definitive flattening versus a continuous rise - the authors of the conflicting studies engaged in an adversarial collaboration. Published in the Proceedings of the National Academy of Sciences (PNAS) in 2023, this joint re-analysis identified the precise source of the discrepancy: standard analytical practices had incorrectly assumed that the effect of income on happiness was homogeneous across the entire population 1011.

The breakthrough emerged from the realization that the 2010 study's measurement of experienced well-being was constrained by a severe ceiling effect 1112. Because the original survey utilized dichotomous (Yes/No) questions regarding the previous day's emotions, a vast majority of respondents (approximately 85 percent) registered perfect or near-perfect scores for positive affect 412. Consequently, the 2010 instrument was not measuring the general trend of happiness; it was an instrument specifically calibrated to measure unhappiness 1012.

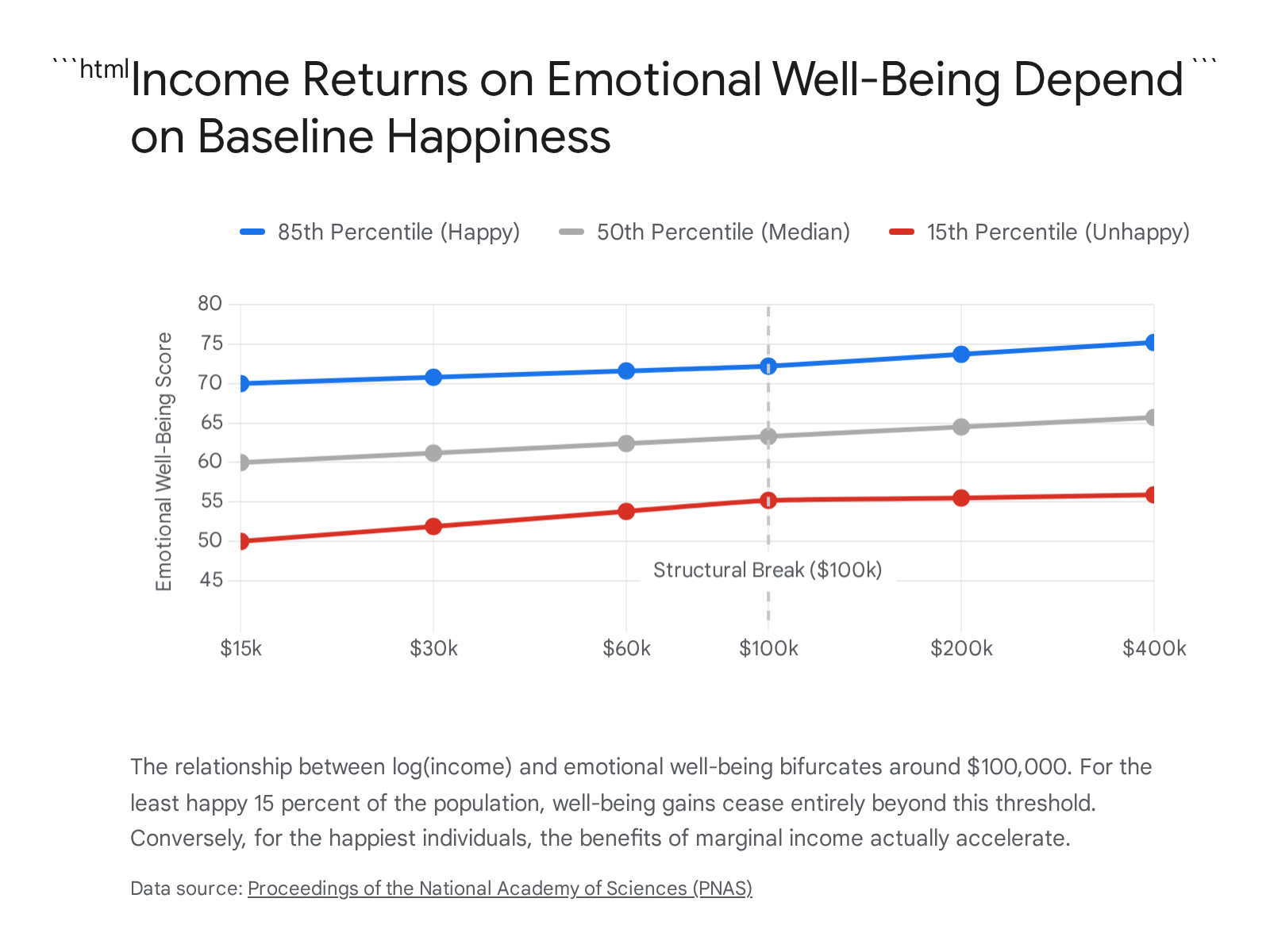

When applying piecewise quantile regression to the sensitive, continuous data from the 2021 study, the researchers discovered that both previous conclusions were partially correct, but applied to entirely different subgroups of the population 1113.

The Unhappy Minority

For the least happy 15 to 20 percent of the population, happiness rises sharply with income but flattens entirely and abruptly at approximately $100,000 (the inflation-adjusted equivalent of the 2010 study's threshold) 911. The quantile regression data reveals stark slope differences: for the 5th percentile, the slope is 2.34 up to $100,000, but drops to a statistically nonsignificant 0.25 above that mark 11. For this cohort, income reliably alleviates the miseries of poverty. However, beyond $100,000, residual miseries - such as clinical depression, bereavement, grief, or heartbreak - cannot be cured by further financial wealth 1011.

The Middle Majority

For the broad middle tier of the population (the 30th to 50th percentiles), happiness increases in a steady, linear fashion relative to log income, traversing high income brackets without a plateau 1112. For instance, the slope for the 30th percentile is 1.33 up to $100,000 and remains a significant 1.21 above $100,000, representing consistent psychological returns on capital 11.

The Happiest Cohort

A previously undocumented phenomenon was observed in the happiest 30 percent of the population (the 70th to 85th percentiles). For these individuals, the correlation between income and happiness actually accelerates and grows significantly steeper once income surpasses $100,000 1112. The data indicates that for the 85th percentile, the slope accelerates significantly above $100,000 (P = 0.023) 11. Thus, for individuals already possessing high emotional well-being, surplus income acts as an amplifier, unlocking higher echelons of life satisfaction and peak experiences 11.

| Study / Methodology | Evaluative Well-Being Findings | Experienced Well-Being Findings | Core Conclusion |

|---|---|---|---|

| Kahneman & Deaton (2010) Retrospective, dichotomous scales |

Continuous log-linear rise across all brackets. | Plateau at ~$75k (2008 USD). | High income buys life satisfaction, but not daily emotional happiness. |

| Killingsworth (2021) Real-time experience sampling, continuous scales |

Continuous log-linear rise across all brackets. | Continuous log-linear rise; no plateau found. | Higher incomes consistently reduce negative affect and increase positive affect globally. |

| Adversarial Re-Analysis (2023) Piecewise quantile regression |

N/A (Focused on emotional well-being) | Bifurcated: Plateau at $100k exists only for the bottom 15 - 20%. Accelerates for top 30%. | Baseline emotional health dictates the psychological rate of return on income growth. |

Global Satiation Thresholds and the Easterlin Paradox

While domestic analyses in the United States establish definitive thresholds, international data introduces complex macroeconomic variables. Research utilizing Gallup World Poll data across 1.7 million individuals worldwide supports the existence of global "satiation points," though they vary substantially by geographic region, cultural context, and economic development stage 614.

International Satiation Thresholds

Using spline regression models to analyze global data, researchers find that globally aggregated life evaluation exhibits satiation at an annual household income of approximately $95,000 (adjusted for Purchasing Power Parity, PPP), while emotional well-being plateaus earlier, between $60,000 and $75,000 615. Crucially, satiation occurs at significantly higher monetary thresholds in wealthier regions compared to developing nations 615.

In certain international cohorts, research notes a secondary "turning point" effect, where incomes extending far beyond the satiation threshold are paradoxically associated with lower life evaluations 615. This downturn is largely theorized to result from hedonic adaptation - where individuals quickly adjust to new income and return to baseline well-being - and the increased time demands, stress, and elevated material desires inherent to highly compensated occupations, which may outpace the psychological benefits of the absolute income gain 15.

The Easterlin Paradox Reexamined

First proposed by Richard Easterlin in 1974, the Easterlin Paradox states that at a fixed point in time, wealthier individuals are happier than poorer individuals within a society; however, as a nation's aggregate income (GDP per capita) grows over long-term time series, the population as a whole does not grow correspondingly happier 161718. The principal mechanism theorized to drive this paradox is social comparison. Because individuals evaluate their financial standing relative to their peers, broad-based national economic growth raises the comparison benchmark alongside individual income, effectively nullifying the psychological gains of the added wealth 1418.

Recent extensive analyses of Gallup World Poll data (2009 - 2019) across more than 150 nations provide a bifurcated update to the paradox based on a nation's baseline wealth and stage of economic development 1617.

| Economic Tier | Cross-Sectional Effect (Individuals within Nation) | Time-Series Effect (National GDP Growth over Time) | Status of the Easterlin Paradox |

|---|---|---|---|

| High-Income Nations | Richer individuals report significantly higher well-being than poorer individuals. | No significant correlation between national income growth and aggregate happiness growth. | Supported. Income only correlates with happiness via proxy improvements in social factors. |

| Middle-Income Nations | Mixed effects when social support variables are controlled. | Income growth strongly correlates with happiness growth over time. | Mixed. Growth aids happiness, but relative standing remains highly relevant. |

| Low-Income Nations | Richer individuals report significantly higher well-being than poorer individuals. | Absolute income growth directly and significantly raises aggregate happiness. | Not Supported. Economic growth directly translates to improvements in the human condition. |

For high-income nations, the paradox holds firm: economic growth does not inherently increase long-term population happiness. In affluent societies, increased GDP primarily improves the human condition indirectly by funding public goods, increasing healthy life expectancy, and bolstering social support networks 1719. In low-income nations, however, raw economic growth remains critical. Absolute increases in household income definitively raise average happiness levels by lifting citizens out of material deprivation, improving baseline survival metrics, and stabilizing social infrastructure 1617.

Psychological Mechanisms of Income Utility

The raw accumulation of monetary assets does not mechanically trigger neurological pleasure or life satisfaction. Rather, money acts as a generalized resource that permits individuals to modify their environments, behaviors, and social interactions. The efficacy of money in buying happiness is highly dependent on the psychological mechanisms governing how it is directed.

Alleviation of Negative Affect Versus Promotion of Positive Affect

The primary emotional benefit of crossing from poverty into middle-class stability is the mitigation of suffering. Compared to higher-income brackets, income gains below $80,000 are disproportionately associated with the reduction of negative feelings (such as stress, worry, and sadness) rather than the generation of positive feelings 320.

Low income serves as an amplifier for daily misery. The psychological burden of routine misfortunes - such as minor illnesses, automotive breakdowns, or relationship conflicts - is exponentially worse when compounded by financial scarcity 1. Moving from low to moderate income effectively purchases immunity from avoidable sources of suffering. Conversely, for higher earners, marginal income increases are more strongly associated with the promotion of positive feelings and peak life experiences, as the baseline causes of negative affect have already been resolved by financial security 320.

Time Scarcity and the Outsourcing of Labor

A profound unintended consequence of global wealth expansion is a rising sense of "time famine" - the psychological stress associated with having insufficient time to meet daily demands 21. Across diverse global samples, severe time pressure exerts a detrimental effect on life satisfaction 21.

Using discretionary income to "buy time" serves as a highly effective psychological buffer against this phenomenon. Studies encompassing 6,271 working adults across the United States, Canada, Denmark, and the Netherlands, alongside targeted samples of Dutch millionaires, demonstrate that outsourcing disliked tasks (e.g., paying for housecleaning, lawn care, or delivery services) is directly linked to greater life satisfaction 212223. Experimental field studies corroborate this causality: individuals randomly assigned to spend $40 on a time-saving purchase reported significantly higher end-of-day happiness and reduced time stress compared to those assigned to purchase a material good of equal value 212223.

Despite the robust empirical benefits of buying time, the strategy is vastly underutilized. Even among cohorts of millionaires, nearly half report spending no money to outsource disliked tasks 22. Psychological barriers often prevent individuals from maximizing this pathway to well-being. These barriers include guilt over perceived laziness, the cultural signaling of "busyness" as a modern status symbol, and a cognitive reluctance to trade concrete, measurable currency for the highly abstract and uncertain concept of free time 2224.

Savoring and Emotion Regulation

While money facilitates access to premium experiences, it simultaneously impairs an individual's psychological capacity to savor mundane pleasures. Savoring is defined as a form of emotion regulation utilized to prolong and enhance positive emotional experiences 28.

Experimental evidence indicates that wealthier individuals report lower baseline savoring abilities. Furthermore, simply exposing subjects to a subliminal or situational reminder of wealth significantly reduces their behavioral enjoyment of simple pleasures. In one study, participants exposed to a reminder of wealth spent significantly less time savoring a piece of chocolate and exhibited reduced visible enjoyment compared to a control group 28. The negative impact of wealth on the capacity to savor actively undermines and suppresses the positive emotional effects of having high income 28. When researchers statistically controlled for savoring ability, the relationship between wealth and happiness increased significantly, proving that wealth acts as a double-edged sword - expanding access to peak experiences while simultaneously eroding the hedonic value of everyday life 28.

Divergent Emotional Orientations

Wealth also dictates the types of emotions individuals are predisposed to experience. Research published by the American Psychological Association, utilizing a nationally representative sample of 1,519 individuals, assessed the propensity to experience seven distinct emotions constituting the core of happiness: amusement, awe, compassion, contentment, enthusiasm, love, and pride 25.

The findings revealed a stark divide based on socioeconomic status. Participants at the higher end of the income spectrum reported a significantly greater tendency to experience emotions focused on themselves, specifically pride and contentment 25. Conversely, individuals at the lower end of the income scale were more likely to experience emotions focused on other people, namely compassion and love, as well as experiencing more awe and beauty in the world around them 25. Psychologists theorize that these differences stem from the affluent desire for independence and self-sufficiency, whereas lower-income individuals develop other-oriented emotions to form interdependent social bonds necessary for coping with more threatening economic environments 25.

Status Anxiety and Social Comparison

Subjective Socioeconomic Status (SES) - an individual's perception of their own rank within the social hierarchy - frequently exerts a stronger influence on subjective well-being than objective, absolute income 2627. The psychological drive for relative status explains why absolute wealth increases often fail to yield expected happiness dividends.

When economic inequality is high within an environment, the social distance between classes expands, leading to widespread status anxiety. Status anxiety is defined as the chronic concern about maintaining one's socioeconomic position and achieving societal standards of success, fostering a highly competitive mindset 2728. Experimental manipulations confirm a causal pathway: residing in perceived high-inequality environments triggers acute status anxiety, making individuals feel trapped in a zero-sum hierarchy 27.

This anxiety manifests in altered consumer and social behaviors. For instance, empirical role-playing experiments (such as the "Bimboola" society simulation) reveal that in economically unequal environments, women allocate significantly more time, attention, and financial resources toward self-sexualization and beautification (e.g., intending to wear revealing clothing) 2930. These experimental frameworks trace this behavior not to an impulse to derogate same-sex competitors, but directly to status anxiety - using appearance enhancement as a psychological strategy for social climbing and aligning with economic partners to secure status 2930. Because relative rank is inherently zero-sum, utilizing wealth primarily to climb the social ladder initiates a hedonic treadmill that rarely results in sustained happiness. Interestingly, social comparison theory suggests that holding a middle-range societal position - allowing for simultaneous upward and downward comparisons - may be psychologically optimal for subjective well-being compared to occupying the extreme upper or lower bounds of an income distribution 31.

Macro-Level Socioeconomic Determinants

If money alone purchased happiness at the national level, global happiness rankings would strictly mirror GDP per capita rankings. They do not. The World Happiness Report, utilizing expansive Gallup World Poll data, consistently places Nordic nations (Finland, Denmark, Iceland, Sweden) at the absolute top of the global life evaluation rankings, despite these nations possessing lower raw GDP per capita than several lower-ranking Western nations 3632.

The translation of national wealth into collective happiness is heavily mediated by social capital. Societal trust - often measured by metrics such as the public's expectation that a lost wallet will be returned by a stranger - serves as a massive statistical multiplier for aggregate happiness 33. Data indicates that populations systematically underestimate the benevolence of their peers; wallet return rates are frequently far higher than expected, generating a baseline of social trust that insulates against economic shocks 33.

Furthermore, benevolence and prosocial spending demonstrate a tight correlation with high national well-being. Generosity yields physiological and emotional benefits for the giver, provided the act is voluntary and visibly impacts the beneficiary 3233. At the macro level, the happiest nations on Earth systematically allocate higher percentages of their gross national income (GNI) to Official Development Assistance (ODA) and international aid 32.

Conversely, nations that rely purely on individual income growth while neglecting the cultivation of interpersonal trust, communal activities, and equitable social infrastructure frequently suffer from high internal inequality of happiness and epidemic levels of loneliness 33. The American Time Use Survey, for instance, highlights a 53 percent increase in Americans eating meals alone over a twenty-year period, a behavioral shift that fundamentally undermines the positive affect associated with social dining 33.

The supremacy of social capital over raw GDP is particularly visible in Latin American nations. Despite possessing less than half the income of highly developed economies, nations like Costa Rica and Mexico consistently record life evaluation metrics that rival or exceed those of the United States and the United Kingdom 3632. In these contexts, exceptional social connectedness, family-centric cultural norms, and community support networks mathematically offset the happiness penalty of lower absolute GDP 32.

Conclusion

The scientific consensus integrating behavioral economics and psychological science concludes that money does indeed buy happiness, but the transaction is complex, non-linear, and bound by strict physiological and psychological parameters.

Income is highly effective at increasing life evaluation across all brackets globally. However, its impact on daily emotional experience depends heavily on the individual's baseline emotional health. For an unhappy minority, money acts strictly as an analgesic, alleviating the severe stress of material deprivation up to a defined threshold (approximately $100,000 in the US), beyond which emotional returns fall to zero. For the psychologically healthy majority, money continuously accelerates emotional well-being, scaling logarithmically without an apparent ceiling.

Ultimately, wealth is a potential energy. If squandered on zero-sum status competition, conspicuous consumption, or the pursuit of relative rank within highly unequal societies, its returns are rapidly negated by hedonic adaptation and status anxiety. Conversely, if deployed strategically to buy free time, alleviate daily frictions, fund prosocial giving, and foster community connectedness, financial wealth remains one of the most reliable catalysts for human flourishing.