Podcasting audience size and monetization models in 2026

The podcasting industry in 2026 represents a mature, multibillion-dollar global media ecosystem that has fundamentally transitioned from its origins as an audio-only, RSS-distributed format into a multi-platform, video-integrated broadcasting channel. Driven by widespread smartphone adoption, advanced in-car infotainment integrations, and shifting media consumption habits, the medium now commands a massive share of global attention. As digital advertising budgets pivot toward measurable, high-intent channels amid broader economic and tariff-related pressures, podcasting has proven exceptionally resilient 12. The current landscape is defined by the convergence of audio and video, the diversification of creator revenue streams beyond traditional host-read advertising, and the expansion of the addressable audience across emerging global markets and historically underpenetrated demographic cohorts.

Global Audience Size and Regional Penetration

The total addressable market for podcast consumption has expanded significantly, cementing the medium as a primary pillar of global digital entertainment and education. This growth is no longer confined to early-adopter Western markets but is increasingly driven by emerging digital economies.

Worldwide Listener Metrics

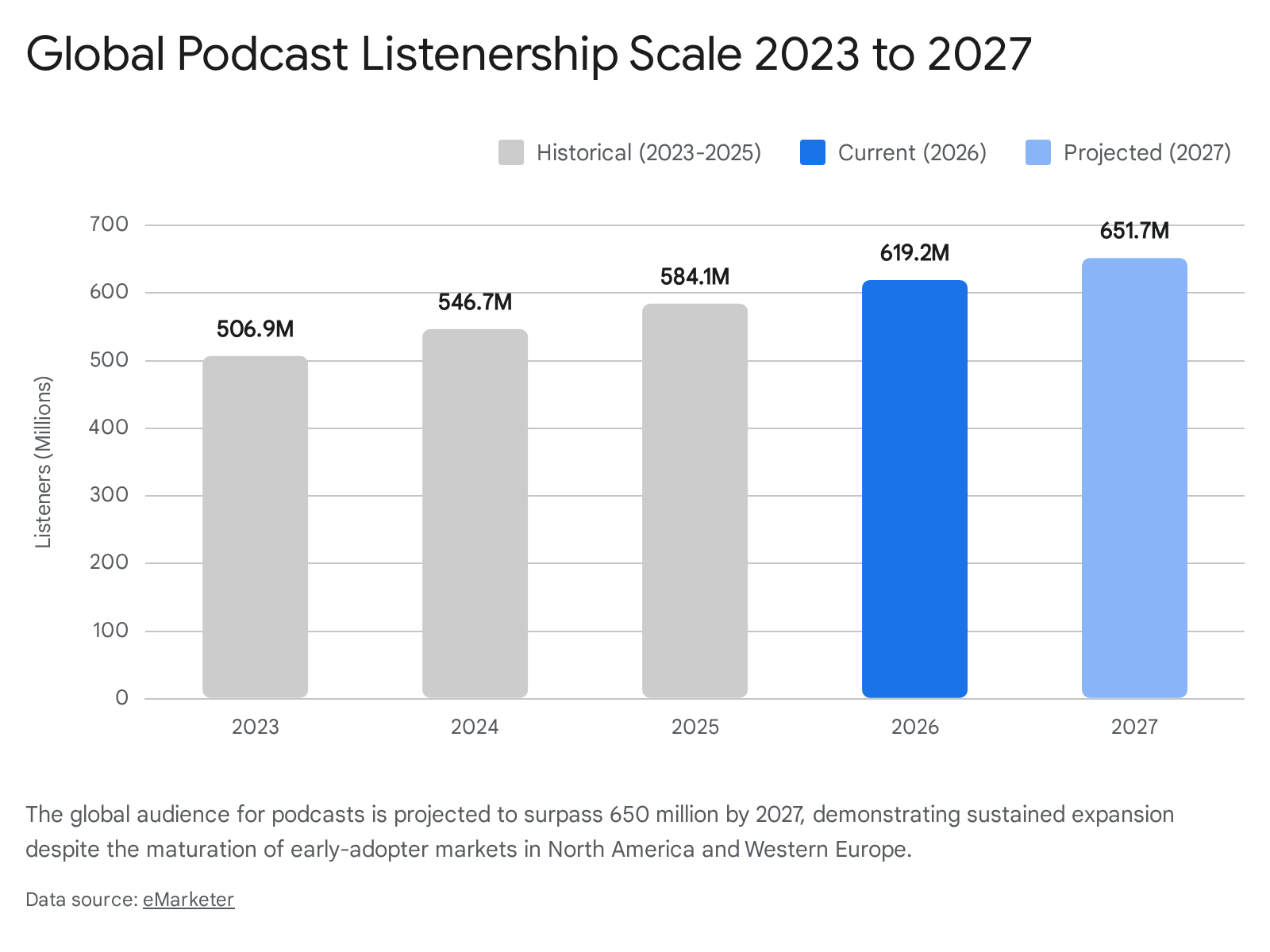

In 2026, the global podcast audience reached an estimated 619.2 million monthly listeners 345. This represents a 6.83% year-over-year increase from the 584.1 million listeners recorded in 2025, and a substantial surge from the 506.9 million baseline measured in 2023 56. Projections indicate that the global listenership will continue its upward trajectory, reaching approximately 651.7 million by 2027 4567.

While the volume of total indexed podcasts worldwide is roughly 4.69 million to 4.7 million, the active universe is considerably smaller 46. When filtering for inactive feeds and "podfade" - shows that have ceased production due to resource constraints or creator burnout - the number of actively publishing podcasts narrows to approximately 450,000 to 500,000 46. Only about 342,000 shows published an episode within a recent 30-day window 6. This stabilization in active show output suggests that while the barrier to entry remains low, the barrier to sustained production is high, leading to a consolidation of audience attention around established, professionally produced networks and dedicated independent creators.

Geographic Market Penetration

While North America birthed the modern podcast industry and maintains the highest overall penetration rate globally, the growth engine has firmly shifted toward emerging digital economies. In 2026, 46.3% of all internet users in North America are estimated to consume podcasts, reflecting a highly established culture of on-demand audio and deep smartphone integration 48.

Conversely, the highest rates of accelerated growth are observed in the Asia Pacific (APAC) and Latin America (LATAM) regions. The APAC region now accounts for 126 million monthly listeners, achieving a 16.8% year-over-year growth rate 9. This expansion is driven by a burgeoning digital content consumption culture, widespread mobile affordability, and local market platforms expanding localized content libraries 1011. In China, listenership has expanded rapidly, supported by government digital initiatives and the dominance of audio platforms like Ximalaya. The Chinese podcast consumer base is estimated at 117.1 million, with projections suggesting the addition of 60 million new listeners by 2027 5711. Other APAC nations demonstrate similarly strong adoption, with South Korea seeing 15.2% of its internet users tuning in, and Japan reaching a market size of $51.55 million driven by younger listeners and popular genres like anime and gaming 810.

Latin America leads the world in relative growth velocity. The region saw an 18.4% year-over-year increase, bringing its monthly audience to 58 million 9. Brazil stands out within this demographic, boasting an estimated 51.8 million listeners and a 44% penetration rate among its population 58. Western Europe lags slightly behind North America, indicating room for sustained, albeit slower, mature-market expansion. Notably, certain markets exhibit exceptional engagement; for example, 68% of adults in South Africa listen to podcasts for at least an hour a week, marking the highest weekly penetration rate globally 78.

| World Region | 2024 Internet User Penetration (%) | 2025 Internet User Penetration (%) | 2026 Internet User Penetration (%) |

|---|---|---|---|

| North America | 43.80% | 45.20% | 46.30% |

| Western Europe | 30.90% | 31.90% | 32.80% |

| Latin America | 30.30% | 31.40% | 32.40% |

| South Korea | 15.20% | 15.90% | 16.50% |

| Japan | 14.80% | 15.40% | 16.00% |

| China | 12.90% | 14.60% | 16.60% |

Data reflects the estimated percentage of regional internet users who actively listen to podcasts. Source: Statista projections 48.

United States Market Dynamics

The United States remains the commercial center of the global podcasting industry, accounting for approximately 67% of total global podcast revenue 12. In 2026, domestic consumption reached unprecedented levels, cementing podcasting not as alternative media, but as a primary broadcasting channel.

Baseline Consumption and Demographics

According to the Edison Research Infinite Dial 2026 study, 80% of all Americans aged 12 and older (roughly 230 million people) have listened to or watched a podcast at some point in their lives, establishing the medium's near-universal awareness 131415. Active engagement metrics are similarly robust. In 2026, 58% of the U.S. population aged 12 and older consumed a podcast on a monthly basis, representing an estimated 167 million active consumers 13141516. Weekly consumption achieved a new high, with 45% of the 12+ population (130 million people) engaging with podcast content every week 131415. The average weekly U.S. listener now consumes approximately 8.2 to 8.3 episodes per week, spending an average of 8 hours and 24 minutes engaged with the medium 916.

Demographic analysis reveals a medium that is highly educated and relatively affluent. According to Pew Research, Americans with a college degree are significantly more likely to turn to podcasts than those with a high school diploma or less 17. Interestingly, political affiliation does not heavily skew overall listenership, with Democrats and Republicans demonstrating roughly equal propensity to consume podcasts 1718. However, trust in the medium varies; 31% of Republicans and Republican-leaning independents trust news from podcasts more than other sources, compared to just 15% of Democrats 17.

Historically, podcasting was dominated by Millennials and Generation Z. While these cohorts remain the backbone of the medium, 2026 data reveals structural demographic shifts. The 35-to-54-year-old demographic has emerged as the most lucrative segment for media buyers. Among this group, 68% are now monthly podcast consumers 131415. More significantly, the most rapid acceleration in digital audio adoption is occurring among older Americans. Monthly online audio listening among Americans aged 55 and older jumped dramatically from 52% in 2024 to 70% in 2026 13141519.

In-Car Listening and the Erosion of Terrestrial Radio

The dashboard has historically been the final stronghold for traditional terrestrial radio. In 2026, AM/FM radio remains the most-used in-car audio source, reaching 73% of American drivers monthly 13. However, the digital migration in the vehicle is accelerating. Overall, 48% of Americans 18 and older report listening to online audio in the car monthly, driven significantly by the fact that 41% of vehicles now feature smartphone digital integration 1319.

The generational divide in automotive listening is stark. Among drivers aged 18 to 34, 73% consumed online audio in the car in the past month, and 55% explicitly listened to podcasts while driving 1319. The loyalty to AM/FM radio is heavily concentrated in the 55+ cohort, which sits at 81% in-car reach 13. As this older demographic increasingly adopts online audio outside the vehicle, the transition of their in-car habits from terrestrial to digital is the next anticipated frontier, posing a severe structural threat to legacy broadcasting business models 13.

The Platform Ecosystem and the Video Transition

The architecture of podcast distribution has been entirely rewritten. The industry has shifted from a decentralized ecosystem reliant on audio-only RSS feeds to a centralized, algorithmically driven, video-first paradigm.

Platform Consolidation

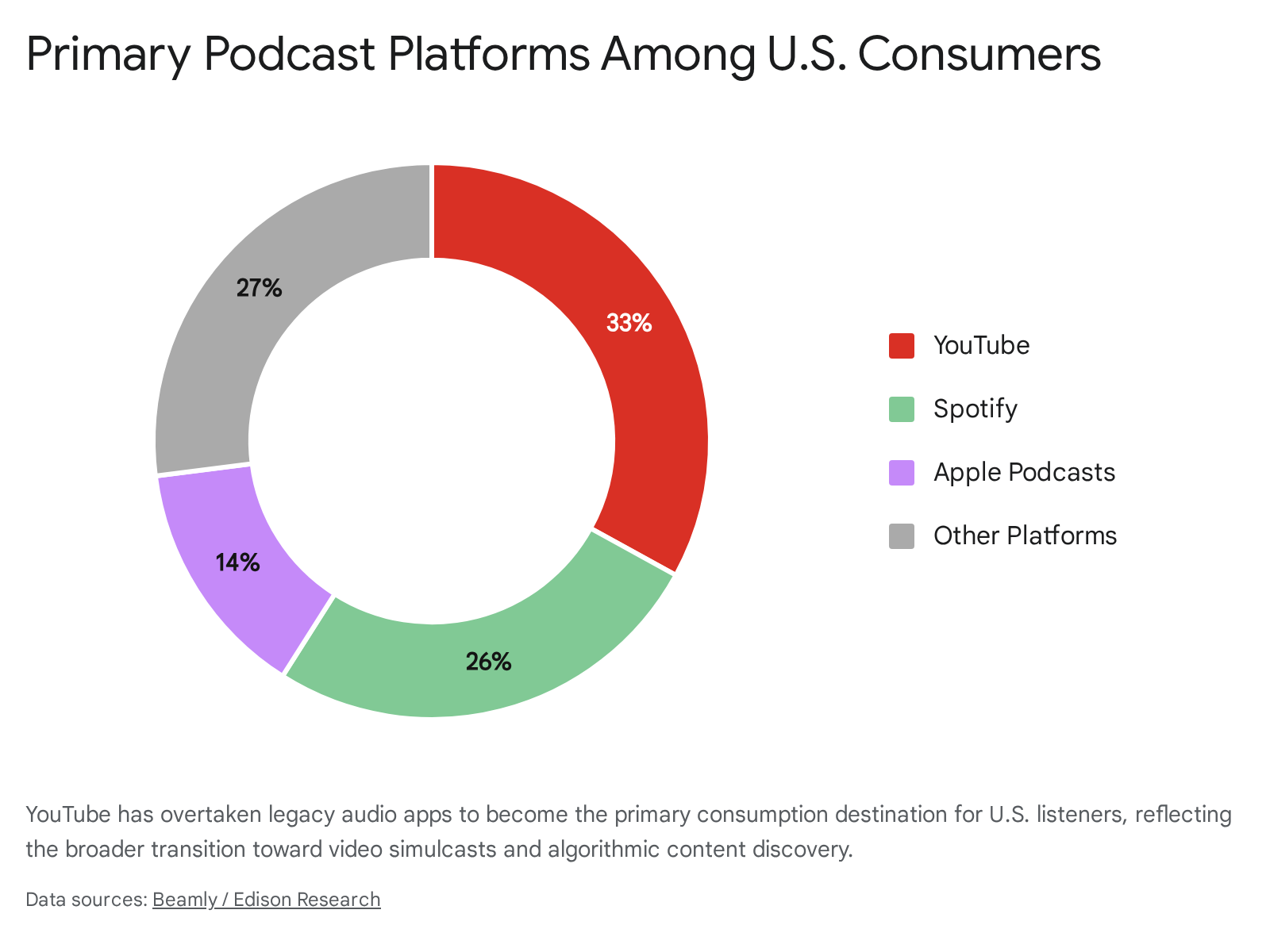

In 2026, the global podcast platform market is an oligopoly controlled by three major technology entities: YouTube, Spotify, and Apple. Together, these three platforms account for the vast majority of all consumption, representing 68% of weekly podcast use in the U.S. 520.

YouTube has fundamentally disrupted the podcasting space, establishing itself as the undisputed market leader. According to Edison Research, YouTube is the primary podcast platform for 33% to 39% of weekly U.S. podcast consumers 61420. Spotify follows with roughly 21% to 26% of primary users, hosting an expansive library of approximately 7 million titles 561420. Apple Podcasts holds between 8% and 14% of the primary usage share, with a catalog of 2.7 to 2.8 million valid shows 6141620.

However, looking purely at audio download volume, Apple Podcasts remains highly relevant, responsible for over 70% of raw traditional downloads due to its entrenched position on iOS devices and historical automatic download mechanisms 20. Yet, when measuring active engagement, time spent, and total reach, YouTube's video-first ecosystem has captured the broader cultural footprint.

The Rise of Simulcasts and Video Integration

The transition to video - often referred to as "vodcasting" or "simulcasting" - is the most significant structural change in the medium. By 2026, 57% of the U.S. population aged 12 and older has both listened to and watched a podcast, confirming that podcasting is now inherently a dual-format medium 1415. Over half of top-ranking U.S. podcasts now publish full-video episodes as their primary distribution method 16. Spotify alone hosts over 500,000 video simulcasts, up from 100,000 in 2023 521.

The strategic advantage of video podcasting lies in discoverability. Traditional audio RSS feeds rely heavily on word-of-mouth (which drives up to 55% of discovery) and external social media marketing 1618. YouTube, conversely, possesses a sophisticated recommendation algorithm that surfaces content to non-subscribers based on watch history and engagement signals 21. This creates a passive discovery loop that dramatically expands a show's reach. Furthermore, video deepens the parasocial relationship between host and audience through visual cues, which is particularly effective for interview formats, comedy, and B2B thought leadership 22. Interestingly, 44% of vodcast watchers report that they do not multitask while viewing, compared to just 29% of audio-only listeners, suggesting that video captures a more dedicated share of active attention 23.

Audience Segmentation: Audio Primes vs. Video Primes

As the medium fractures between audio and video, audience behavioral segmentation has become highly nuanced. Industry analysts identify a powerful cohort known as "Audio Primes" - consumers who consume at least 75% of their podcast content purely as audio 2425.

Audio Primes represent 22% of all podcast consumers but punch significantly above their weight in economic value 2526. Despite assumptions that audio-only listeners skew older, the Audio Prime cohort actually under-indexes in the 55+ age group and over-indexes in the 35-to-54 bracket 26. They are highly educated and represent the upper-income tiers of the market 26. Crucially, Audio Primes are fiercely loyal and function as the primary word-of-mouth discovery engine for the industry. They are significantly more likely to recommend shows to others, and 72% report using the same platform every time they listen 26.

Even when utilizing video-first platforms like YouTube, Audio Primes use the app as an audio player, consuming content while minimized or in the background 26. This bifurcation between active viewing (Video Primes) and passive, high-retention listening (Audio Primes) dictates how creators structure their content and how advertisers value impressions.

Advertising Economics and Monetization Models

The economics of podcasting have stabilized into a multi-tiered marketplace characterized by premium, high-cost host-read inventory and a rapidly scaling programmatic layer. Estimates for the total size of the global podcast market vary by methodology, ranging from $31.5 billion to nearly $40 billion in broad market valuation 48.

In terms of direct advertising, global podcast ad spend crossed the $5 billion threshold in 2026, achieving a 20% year-over-year growth trajectory 3923. In the United States, the Interactive Advertising Bureau (IAB) projects that traditional podcast ad revenue will reach between $2.6 billion and $3 billion+ by the end of 2026 927. Furthermore, independent financial analyses suggest traditional IAB metrics may undercount the true size of the domestic market. A recent analysis calculated the actual U.S. podcast economy at $4.7 billion by including programmatic ad tech, consumer-direct revenue, and video monetization via YouTube 12.

Host-Read Sponsorships vs. Programmatic Advertising

The advertising ecosystem is currently split between two distinct deployment models, each serving different marketing objectives: Host-Read ads and Programmatic/Dynamic Ad Insertion (DAI).

Host-Read Sponsorships: Host-read ads remain the gold standard for podcast monetization, accounting for approximately 58% of total ad spend 9. These endorsements are integrated into the show's narrative by the creator, relying on the parasocial trust established with the audience. Because they feel native and organic, host-read placements command the highest premiums in the industry. The average Cost Per Mille (CPM) for mid-tier host-read ads sits between $25 and $50, while premium placements on top-100 shows regularly reach $60 to $120 CPM 9282930.

The high cost is justified by exceptional performance metrics. Host-read ads generate aided ad recall rates of 60% to 70%, significantly outperforming traditional digital display formats 929. Placement within the episode also dictates efficacy; mid-roll ads generate the highest recall (63%), followed by pre-roll (48%) and post-roll (29%) 9. Furthermore, they drive strong purchase intent, with 54% of listeners stating they are more likely to buy from a brand after hearing a podcast ad 331.

Programmatic and Dynamic Ad Insertion (DAI): Programmatic advertising represents 29% of ad spend and is a fast-growing monetization segment 9. Utilizing DAI technology, pre-recorded ads are automatically inserted into audio streams based on the listener's geolocation, demographic profile, and listening context 3233. This allows publishers to monetize their entire back catalog of evergreen episodes 2234.

Programmatic CPMs are generally lower, ranging from $15 to $25 92835. The recall rates are correspondingly lower, sitting between 24% and 31% 9. However, programmatic buys offer advertisers massive scale, precise audience targeting, and immediate deployment, solving the inherent inventory bottlenecks of host-read sponsorships 2933. The 2026 market has seen a shift toward Programmatic Guaranteed (PG) deals, where premium brands purchase high-quality inventory via automated pipes, blending the transparency of digital tracking with the brand safety of direct publisher relationships 35.

| Advertising Model | Share of Ad Spend | Average CPM Range | Aided Ad Recall | Primary Use Case |

|---|---|---|---|---|

| Host-Read (Mid-Tier) | ~58% (combined) | $25 - $50 | 60% - 70% | High-trust brand building, direct-response conversion 929. |

| Host-Read (Top 100) | ~58% (combined) | $60 - $120 | 60% - 70%+ | Mass market awareness, major brand integrations 929. |

| Programmatic / DAI | ~29% | $15 - $25 | 24% - 31% | Scalable reach, precise demographic targeting, back-catalog monetization 92829. |

Creator Revenue Diversification

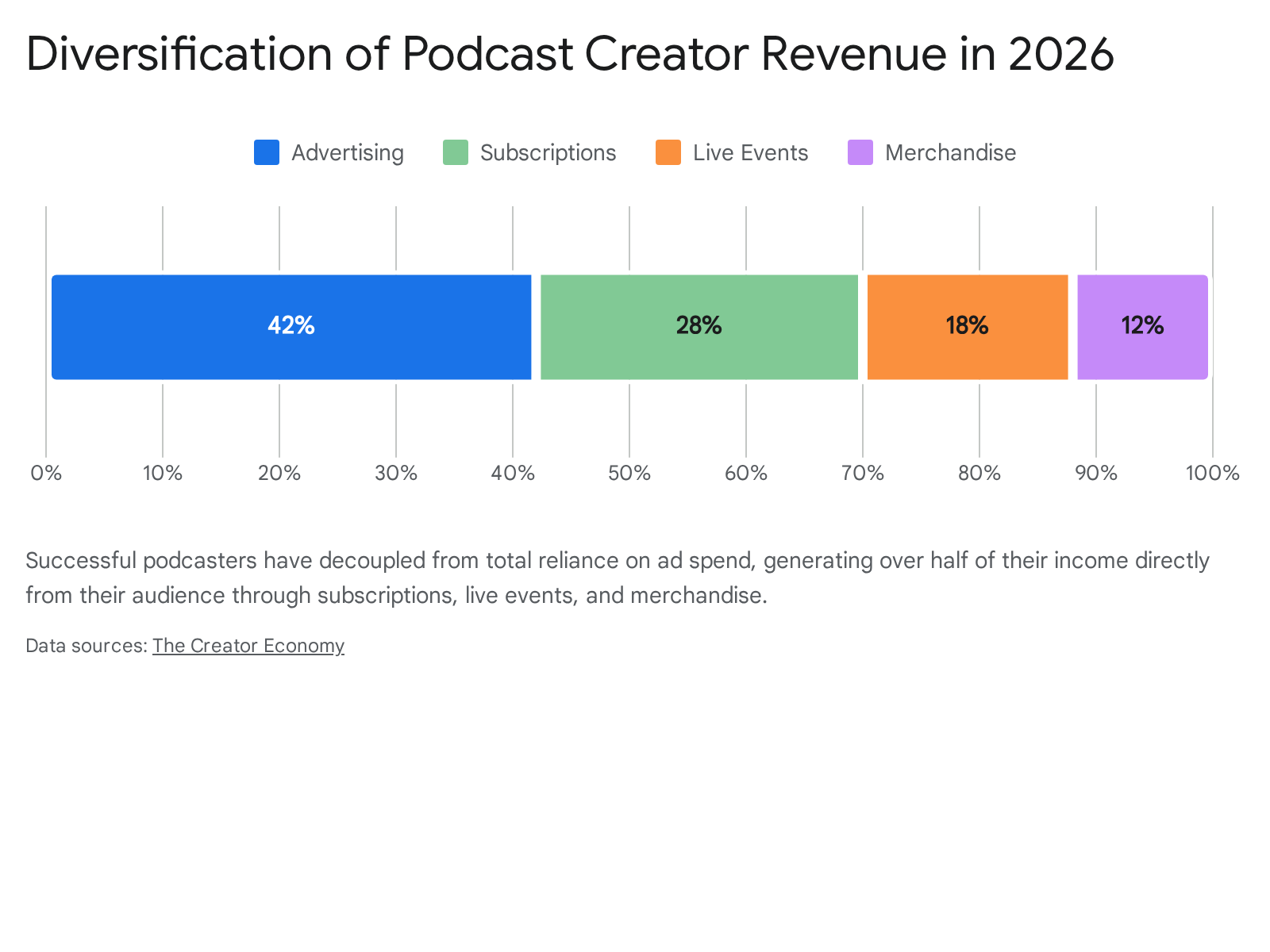

As programmatic CPMs face downward pressure due to inventory saturation, successful podcast creators and networks in 2026 have shifted away from a pure advertising model toward diversified revenue portfolios. Relying solely on a single revenue stream is increasingly viewed as a structural risk.

Industry data tracking top-performing creators reveals a balanced monetization matrix: 42% of revenue is derived from advertising, 28% from direct subscriptions, 18% from live events, and 12% from merchandise and product sales 36.

The growth of the subscription layer has been highly impactful. Platforms such as Apple Podcasts Subscriptions, Spotify, and independent solutions like Patreon allow creators to offer ad-free episodes, bonus content, and exclusive community access 123236. Typically, creators observe a 3% to 5% conversion rate of their free listener base into paid subscribers, with price points generally ranging from $5 to $15 monthly 36. This recurring revenue establishes a predictable financial baseline that insulates publishers from the volatility of the advertising market.

Sector Specificity: B2B vs. B2C Models

Monetization and growth strategies diverge sharply based on the podcast's core audience. Business-to-Consumer (B2C) podcasts - such as true crime, comedy, and society/culture shows - rely on massive scale to generate revenue through high-volume programmatic advertising, broad consumer sponsorships, and merchandise sales 37.

Conversely, Business-to-Business (B2B) podcasts operate on a model of "influence density" rather than raw scale 3032. A B2B show targeting enterprise software executives may only reach a few thousand listeners per episode. However, because those listeners represent concentrated purchasing power, the podcast can command exceptionally high CPMs for specialized host-read ads 22. More importantly, B2B podcasts are increasingly utilized as direct performance marketing and business development channels. The show acts as a networking asset, driving qualified pipeline, strategic partnerships, and thought leadership authority, yielding an indirect return on investment that far exceeds standard ad revenue 223037.

Content Formats, Engagement, and Artificial Intelligence

The structural composition of podcasts has optimized around listener habits. In 2026, the median episode length is 41 minutes, a slight decrease from previous years, fitting neatly into daily commutes and workout routines 9. Most podcasts (59%) run between 20 and 60 minutes 7. Engagement remains exceptionally high; 93% of listeners report finishing most or all of each episode they start 18. Specific genres command immense loyalty, with true crime and fiction podcasts boasting completion rates of 85% 4. Comedy remains the most beloved genre by total listening hours (30%), followed by society and culture (18%), and lifestyle (15%) 31. News consumption via podcasts is also significant; 32% of U.S. adults get news from podcasts, a figure that jumps to 39% among adults under 50 317.

Technological Catalysts and the Role of AI

The integration of Artificial Intelligence (AI) has significantly altered the operational economics of podcasting, though consumer acceptance remains bifurcated.

For creators and publishers, AI has delivered profound workflow optimizations. Tools that automate transcription, edit out filler words, generate show notes, and clip long-form episodes into short-form social media assets have drastically reduced post-production time and overhead costs 638. Furthermore, AI translation and synthetic dubbing have emerged as vital growth drivers, allowing publishers to instantly localize content to capture high-growth non-English markets in LATAM and APAC without incurring expensive voice-acting costs 9. In 2026, 61% of podcasters plan to integrate AI into their production workflows 4.

However, the application of generative AI for front-facing content - specifically synthetic voices and AI-hosted podcasts - faces significant audience resistance. Awareness of generative AI tools has reached 93% among the U.S. population, meaning audiences are highly attuned to synthetic media 141516. The most valuable demographic, Audio Primes, exhibit deep skepticism; 48% stated they would be less likely to continue listening if they discovered a show utilized AI-generated voices 2426. Video-first consumers are slightly more tolerant, viewing AI as a contextual tool rather than a replacement for human authenticity, but resistance remains a factor 2439.

For advertisers, AI-voiced host-read ads pose a performance risk. Current data indicates that AI-generated host endorsements perform closer to programmatic benchmarks (24% to 31% recall) than to authentic, human host-reads (60% to 70% recall) 9. Consequently, while AI drives massive backend efficiency, the fundamental currency of podcasting - parasocial trust and authentic human connection - cannot yet be synthesized without a measurable drop in audience engagement and advertising efficacy.

Conclusion

The state of podcasting in 2026 is characterized by robust global scale, exceeding 619 million listeners, and deep domestic penetration that has successfully captured the highly lucrative 35-to-54 and 55+ demographics. Growth is no longer driven purely by the organic discovery of audio files, but by the algorithmic distribution of video podcasts on YouTube and deliberate expansion into international markets, particularly within the APAC and LATAM regions.

Economically, the industry has matured beyond a single-channel advertising model. While global ad spend eclipses $5 billion - anchored by the high-value performance of host-read sponsorships and the scalable reach of programmatic insertion - publishers have insulated themselves by building diversified media businesses supported by subscriptions, live events, and merchandise. Ultimately, despite the rapid advancement of AI production tools and the industry-wide shift toward visual consumption, the core driver of podcasting's value remains unchanged: the deep, high-retention trust established between creators and their highly engaged audiences.