Mechanisms and Characteristics of Network Effects

Network effects constitute the most powerful source of defensibility and value creation in the modern digital economy. Extensive research examining technology companies founded since 1994 reveals that while only an estimated 35% of digital businesses possess core network effects, these specific companies are responsible for approximately 70% of the total value created in the sector over the past three decades 123. When properly harnessed, network effects deliver asymmetric upside, allowing nascent platforms to rapidly dismantle established incumbents and erect formidable economic moats 23.

Despite their outsized impact on corporate valuation and market survival, network effects remain widely misunderstood by both platform architects and financial markets. The terminology has been heavily diluted, frequently co-opted by corporate management and venture capital marketers to justify inflated valuation multiples for fundamentally linear businesses. Companies exhibiting rapid viral growth, immense economies of scale, high switching costs, or strong brand recognition routinely - and often incorrectly - claim to possess network effects 4. This conceptual conflation leads to flawed strategic decisions, misallocated capital, and eventual market corrections when the supposed "network" fails to protect profit margins against new entrants.

Understanding the actual mechanics of network effects requires dissecting the mathematical models that govern platform growth, separating the acquisition of new users from the accretion of intrinsic value, and analyzing the structural vulnerabilities that expose seemingly dominant platforms to regional and technological disruption. Furthermore, contemporary shifts in generative artificial intelligence and regulatory interventions are actively degrading traditional data flywheels, forcing a reevaluation of how digital defensibility will function in the coming decade.

Mathematical Models of Network Growth

At its core, a network effect exists when the value of a product or service to a single user increases as the number of other users utilizing the same product or service increases 56. However, not all networks accrue value at the same rate. The theoretical framework for understanding network defensibility relies on foundational mathematical laws that describe how utility scales with increasing node density.

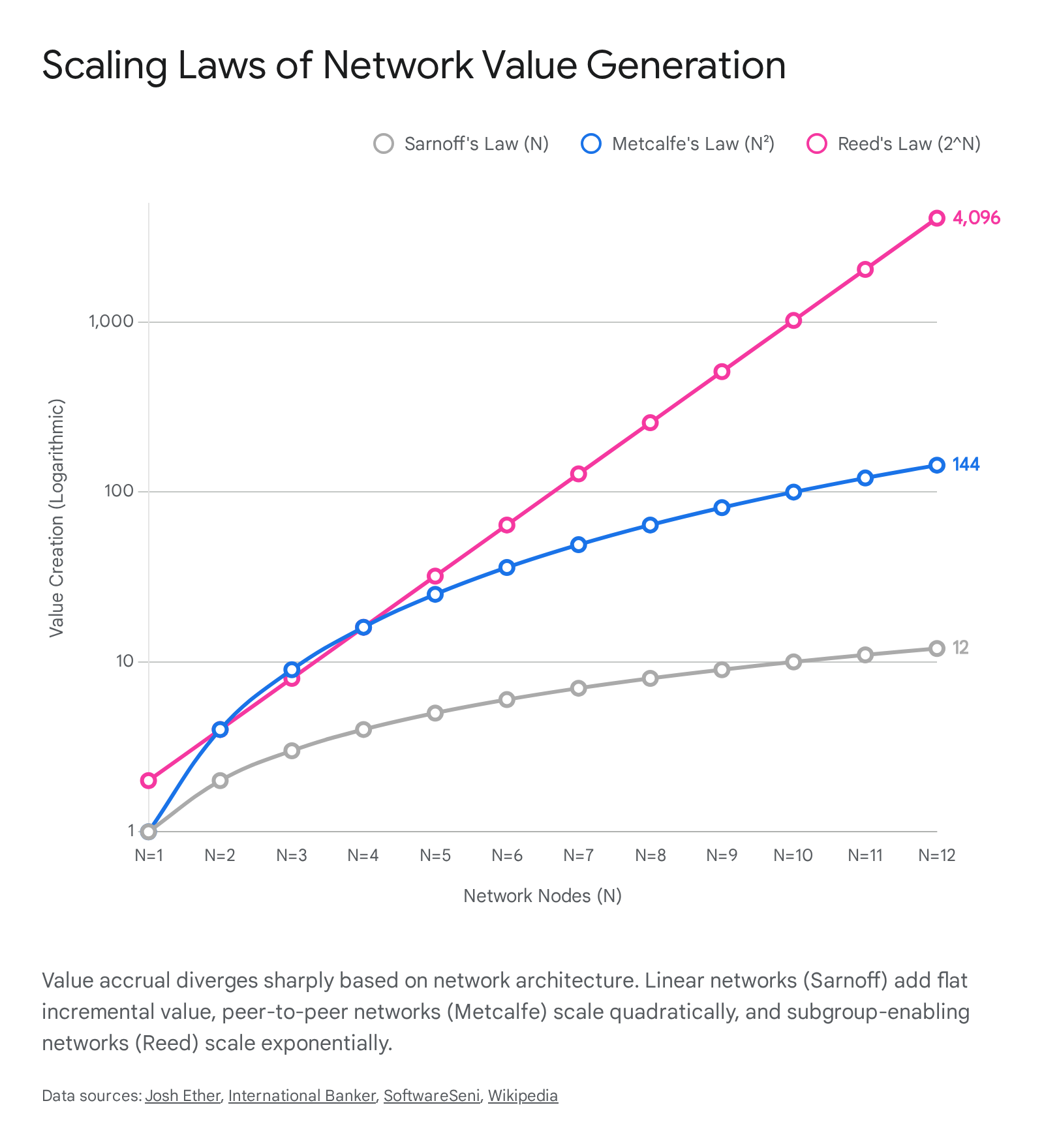

The baseline for network value is established by Sarnoff's Law, named after former Radio Corporation of America (RCA) executive David Sarnoff. It posits that the value of a broadcast network is directly proportional to the number of its viewers or listeners, scaling linearly ($V \propto N$) 87. Sarnoff's Law describes basic linear economics: a radio station adds one unit of value for every new listener it acquires. This represents a one-way, hub-and-spoke model. Platforms operating under Sarnoff's Law - such as traditional podcasting, linear streaming content platforms, and basic e-commerce storefronts - exhibit no meaningful user-to-user interaction 7. While these entities can generate substantial revenue, they do not possess genuine network effects because the millionth user derives no direct benefit from the presence of the million-and-first user.

The concept of the true network effect is governed by Metcalfe's Law, proposed by Ethernet co-inventor Robert Metcalfe. Metcalfe's Law states that the financial value or influence of a telecommunications network is proportional to the square of the number of connected users ($V \propto N^2$) 18. Because the number of unique possible connections in an $N$-node network is expressed mathematically as the triangular number $N(N-1)/2$, the utility grows quadratically 8. Two nodes create one connection; five create ten; twelve create sixty-six. Research analyzing a decade of data from Facebook and the Chinese conglomerate Tencent demonstrates that the growth trajectories and valuations of these social communication platforms track Metcalfe's Law exceptionally well, often following a "netoid" (S-shaped) adoption function 1. Alternative models, such as Odlyzko's Law, argue for a slightly tempered scaling of $V \propto N \log(N)$ to account for the diminishing returns of adding peripheral nodes, while financial applications of Metcalfe's Law to cryptocurrencies like Bitcoin have shown that network size explains over 70% of the variance in asset value 18.

A more extreme scaling paradigm is Reed's Law, formulated by David P. Reed. This law argues that for networks permitting the formation of distinct subgroups and clusters - such as advanced social networks, dynamic forums, and workplace communication tools - the value grows exponentially ($V \propto 2^N$) 87. Reed's Law implies that the utility of group-forming networks vastly outpaces pure communication networks once a critical user density is reached. For instance, while a standard SMS messaging application scales quadratically via point-to-point connections, a platform that allows intricate overlapping group identities scales exponentially due to the massive combinatorial explosion of potential sub-communities 7.

| Scaling Law | Mathematical Function | Network Architecture | Economic Mechanism | Example Platforms |

|---|---|---|---|---|

| Sarnoff's Law | $V \propto N$ | Hub-and-Spoke (Broadcast) | Linear addition of utility per marginal user. | Podcasting, Linear Streaming, Content Publishers. |

| Metcalfe's Law | $V \propto N^2$ | Peer-to-Peer (Communication) | Quadratic scaling based on total possible two-way connections. | Telecommunications, WhatsApp (1-to-1), Base Cryptocurrencies. |

| Reed's Law | $V \propto 2^N$ | Cluster-Based (Group Forming) | Exponential scaling driven by overlapping sub-communities. | Slack, Facebook Groups, Reddit, Discord. |

Bootstrapping Mechanisms and Atomic Networks

While mathematical models assume positive network effects from inception, early-stage platforms face a perilous bootstrapping phase. When a platform has zero or very few users, the utility is fundamentally negative; early adopters experience "anti-network effects" because the platform is devoid of interactions, causing them to churn before critical mass is achieved 910.

In ecology, the Allee effect describes a phenomenon where a population's growth rate becomes negative if the density falls below a critical threshold 11. Applied to network economics, a platform must surpass its specific Allee threshold to become self-sustaining 10. This dynamic represents the fundamental "Cold Start Problem" - a destructive force that drives new networks toward zero participation unless actively managed 912. Overcoming the Cold Start Problem requires abandoning aggregate user metrics and focusing on building an "atomic network" - the absolute smallest, densest possible cluster of users capable of supporting a stable, positive interaction loop 111215.

The scale of an atomic network varies drastically depending on product architecture. For a workplace communication tool like Zoom or Slack, an atomic network requires a micro-cluster of just two to three co-workers 10. For a complex, real-time liquidity marketplace like Uber, an atomic network requires a minimum of roughly 300 drivers and corresponding riders active simultaneously within a single, hyper-local geographic radius 910. Conversely, a localized accommodation platform like Airbnb historically required a minimum inventory of approximately 100 active listings in a specific destination city to reach sufficient liquidity to attract visiting travelers 10.

Product architects employ specific tactical mechanisms to force the creation of atomic networks. The "come for the tool, stay for the network" strategy involves offering a standalone software utility that solves a problem for a single user, organically assembling a user base that can later be connected 1213. Other mechanisms include strict invite-only access to manufacture artificial density (employed early by LinkedIn and Gmail), targeted saturation of dense local hubs (such as college campuses or specific corporate campuses), and "flinstoning" - the manual curation of supply and demand by the founders to simulate network liquidity 101112. Once a single atomic network achieves stabilization, the platform reaches a "Tipping Point," allowing it to replicate the network sequentially across adjacent demographics or geographies until reaching total market "Escape Velocity" 912.

Distinguishing Network Effects from Viral Growth

A primary source of analytical error among founders and venture investors is the conflation of network effects with viral marketing 45. While both phenomena rely on existing users to influence the behavior of new users, they serve entirely different strategic functions and operate under distinct economic mechanics.

Virality is fundamentally a user acquisition mechanism. A viral effect occurs when an existing customer acts as a distribution channel, bringing in new customers and consequently driving the blended Customer Acquisition Cost (CAC) toward zero 4. This relies on engineered positive feedback loops: a user actively invites a colleague to unlock a referral reward, or a product's usage inherently exposes non-users to the brand (e.g., sharing a file link or embedding a watermarked video) 413.

While viral growth is highly desirable for scaling, it does not inherently improve the underlying product utility. A company can possess explosive virality without any network effects. For example, a viral mobile game spreads rapidly through word-of-mouth and social media sharing. However, the game itself does not functionally improve for the original user simply because millions of others have downloaded it. Consequently, highly viral products without network effects often suffer from catastrophic churn once the initial novelty fades, as there is no structural mechanism keeping users locked into the ecosystem 417. The "Golden Age of Virality" (roughly 2000 to 2012) saw many digital products explode in size using aggressive contact-list scraping and referral incentives, only to collapse rapidly because they lacked genuine increasing returns on value 4.

Where virality drives low-cost acquisition, network effects drive high-margin retention and defensibility 4. Network effects add intrinsic value to the product itself over time, structurally increasing Customer Lifetime Value (LTV) and making it increasingly irrational for a user to switch to a competitor 1317.

The divergence between the two concepts is clearly illustrated by the trajectories of Zoom and Slack during the 2020 transition to remote work 5. Zoom achieved unprecedented virality, growing its daily active users from 10 million in late 2019 to 200 million by the first quarter of 2020 5. The platform's frictionless onboarding allowed users to host calls with external parties seamlessly. However, Zoom inherently lacks strong network effects. Its core value proposition - stable, low-friction video communication - remains identical regardless of whether a participant uses the software every day or is clicking a meeting link for the very first time 5. The presence of millions of other global Zoom users does not make an isolated call between two individuals any better. Because it lacked a robust network effect, Zoom's defensibility remained structurally weak, exposing it to intense commoditized competition from Microsoft Teams and Google Meet.

By contrast, Slack combines both viral acquisition and intra-organizational network effects 59. As more team members join a Slack workspace, the archival message history, channel structure, and integrated third-party workflows become significantly more valuable to the organization. While Slack's network effect is ultimately bounded - it ceases to compound new value once 100% of the employees in a specific company are onboarded - the resulting lock-in prevents organizational churn much more effectively than a pure viral acquisition model 5.

| Characteristic | Viral Growth Mechanics | Network Effect Mechanics |

|---|---|---|

| Primary Business Function | Accelerates user acquisition. | Enhances user retention and defensibility. |

| Mechanism of Action | Existing users expose the product to non-users. | Existing users create value for other existing users. |

| Impact on Unit Economics | Lowers Customer Acquisition Cost (CAC). | Increases Customer Lifetime Value (LTV) and pricing power. |

| Product Utility | Product value remains static as the user base grows. | Product value intrinsically improves as the user base grows. |

| Prominent Examples | Single-player viral games, Zoom, Referral programs. | Social networks, two-sided marketplaces, communication protocols. |

Scale Economies and the Illusion of Switching Costs

A secondary area of persistent market confusion arises when analyzing mature, highly capitalized companies. Many firms attempt to claim network effect valuation multiples by pointing to their massive physical size or their highly captive customer bases. In reality, these companies are often relying on traditional economies of scale or artificially engineered switching costs - defensibilities that are powerful, but fundamentally linear 14.

A scale effect, or demand-side economy of scale, occurs when a company's increasing volume allows it to reduce marginal unit costs, spread fixed operational overhead over a larger base, or secure superior supplier pricing 21520. Traditional linear businesses, such as manufacturing conglomerates, basic resource extractors, and direct-to-consumer (DTC) retail brands, rely almost entirely on scale effects 15. If millions of consumers purchase a commodity like gold, the mining operations simply extract and sell more gold; the physical product does not functionally improve for the original buyer 15. Similarly, when consumers purchase inventory directly from a retailer, they benefit from the retailer's massive fulfillment infrastructure and bulk purchasing power - a scale effect, not a network effect 2. Scale effects operate linearly on the cost side, whereas true network effects operate non-linearly on the value side 220.

Switching costs represent the friction, financial expense, or operational penalty a consumer faces when migrating from one provider to another 14. While robust network effects inherently create high switching costs (because leaving the network means abandoning accrued connections and marketplace liquidity), switching costs frequently exist entirely independently of network effects 614.

Switching costs generally manifest in three distinct forms 15: 1. Financial Switching Costs: Contractual penalties, early cancellation fees, or the loss of accrued financial loyalty points (e.g., airline miles, long-term pipeline infrastructure contracts). 2. Procedural Switching Costs: The operational time, effort, and learning curve required to adopt a new system. Executing a complex data migration, onboarding a new corporate accounting software suite, or migrating a workforce from Apple's iOS ecosystem to Google's Android represent massive procedural friction 141516. 3. Relational Switching Costs: The loss of established interpersonal business relationships and institutional knowledge, such as terminating a specialized consulting firm or long-term B2B supplier 15.

Unlike network effects - which typically trigger winner-take-all market dynamics and tip the ecosystem to a single leader - switching costs allow multiple incumbents to comfortably coexist within an oligopoly 1416. Economic models of dynamic price competition demonstrate that without viable outside options, high procedural switching costs lead firms to extract value from captive users via a "fat-cat" effect 16. Firms with large, locked-in customer bases intentionally set higher prices to harvest current customers, relying on the high friction of switching to prevent churn, rather than competing aggressively for new market share 16.

The distinction between true network effects and mere scale or switching costs is not merely academic; misidentification leads to catastrophic valuation collapses. The financial analysis detailed in The Platform Delusion chronicles how companies like Blue Apron (meal delivery) and Casper (bedding) went public with tech-style valuations, implicitly or explicitly promising network-driven exponential growth. However, their market capitalizations evaporated rapidly when they were revealed to be standard linear businesses subject to fierce, commoditized competition .

The fitness hardware company Peloton provides a stark legal and operational example of this dynamic. In its public filings and marketing campaigns, Peloton frequently touted its "ever-growing" library of live and on-demand fitness classes as a compounding moat 171825. This was fundamentally a scale effect wrapped in the language of a network effect: Peloton was funding a massive, centralized content library to attract users. However, in 2018 and 2019, following copyright infringement litigation initiated by the National Music Publishers' Association over unlicensed songs, Peloton was forced to abruptly purge more than half of its digital catalog 1718.

Because the catalog was a function of centralized corporate spending (scale) rather than decentralized user generation (a true network effect), the platform's value proved highly fragile 17. Subscribers initiated class-action lawsuits under New York General Business Laws for deceptive practices and false advertising 25. While several legal claims were eventually curbed by federal judges ruling that the company's forward-looking risk disclosures were adequate, or that plaintiffs failed to prove Peloton explicitly anticipated the mass deletion when the marketing statements were made, the underlying economic reality remained unchanged: Peloton's defensibility was rooted in licensed content scale, not an autonomous, compounding network effect 172627.

Typology of Multi-Sided Platforms and Ecosystem Synergies

For the estimated 35% of technology unicorns that do possess genuine network effects, the underlying network architecture varies significantly. Researchers have identified upwards of 16 distinct sub-types of network effects, categorized broadly by whether they are direct, indirect, or multi-sided 123.

Direct (or same-side) network effects occur when users derive value from the addition of the exact same type of user to the platform 19. Telephone networks and messaging platforms like WeChat operate primarily on direct network effects 1629. Conversely, indirect (or cross-side) network effects manifest in multi-sided platforms, where two or more distinct groups of users interact. The classic example is a two-sided marketplace: the platform becomes more valuable to buyers only when more sellers join, and it becomes more valuable to sellers only when more buyers participate 61920. Unlike direct network effects, in indirect networks, density and curation consistently trump pure scale. The simple addition of more users is irrelevant if those users are not high-quality, relevant matches for the opposite side of the marketplace 6.

The pricing strategies of these multi-sided platforms are often modeled using stylized Hotelling models, which analyze how heterogeneous taste preferences and cross-side network externalities dictate user participation 1921. Platforms must constantly adjust subsidies and charges based on whether users engage in single-homing (using only one platform) or multi-homing (using several). When cross-side network effects are highly asymmetric - for example, if sellers value access to buyers much more than buyers value access to marginal sellers - the platform will optimize revenue by posting a heavy charge to the sellers while heavily subsidizing the buyers 19.

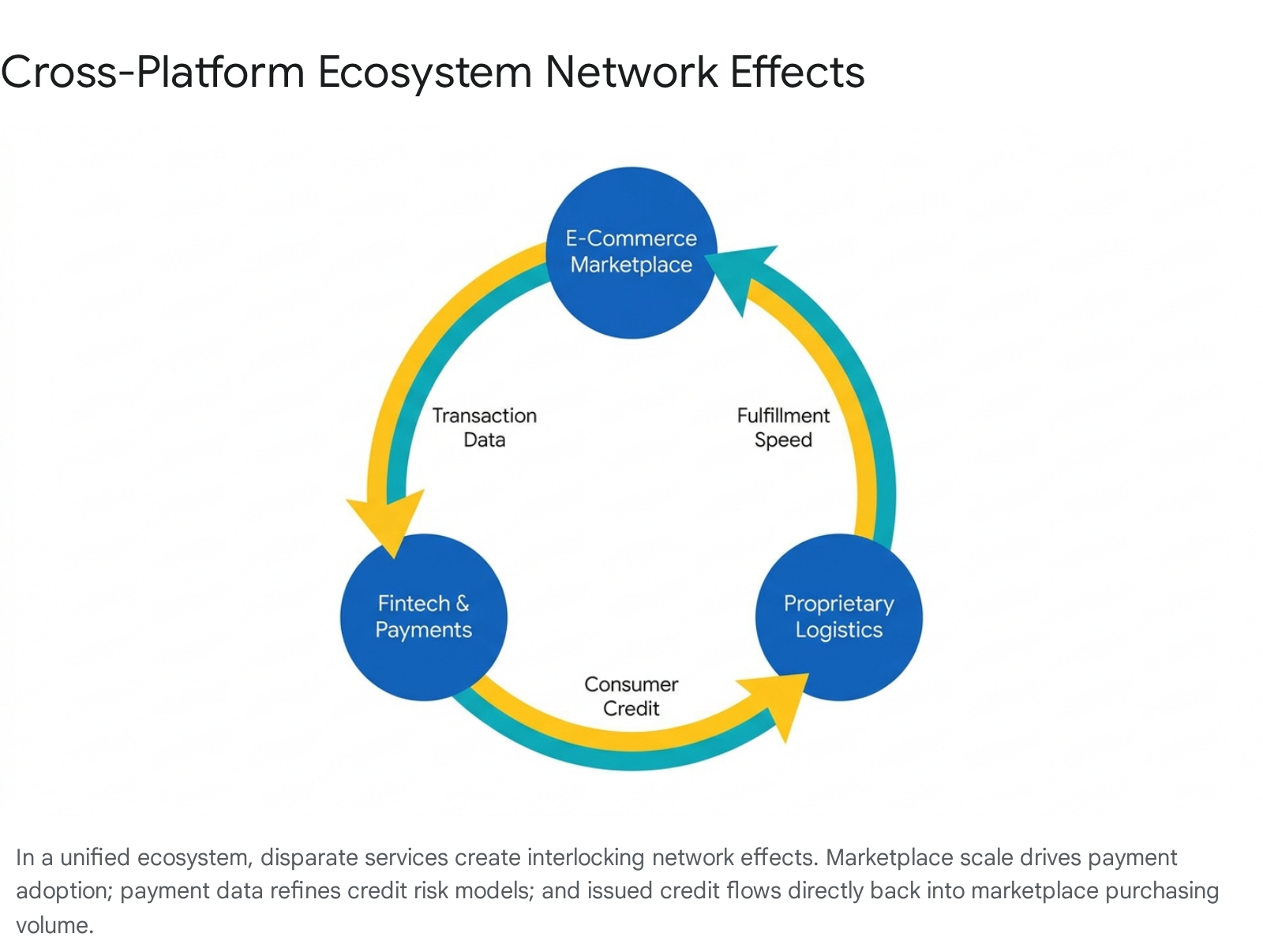

Ecosystem Synergy: MercadoLibre versus Amazon

The most defensible platforms layer multiple types of network effects into an interconnected ecosystem, creating cross-platform network effects where one core platform service inherently subsidizes and strengthens another 20.

This complex architectural strategy is evident in the competitive divergence between Amazon and MercadoLibre in Latin America 322234. While Amazon relies predominantly on its monumental global fulfillment scale, MercadoLibre has successfully constructed an integrated, tripartite network effect combining its core e-commerce marketplace, its proprietary logistics network (Mercado Envios), and its dominant fintech arm (Mercado Pago) 323435.

MercadoLibre's cross-platform synergies generate massive non-linear advantages. As the e-commerce marketplace attracts unique buyers (exceeding 100 million in 2024), it drives natural adoption of Mercado Pago to facilitate transactions in regions characterized by vast underbanked populations 323637. Mercado Pago, which processed $83.7 billion in volume and serviced 78 million monthly active users by late 2025, acts as a massive data collection engine 3236. This transaction data feeds directly into proprietary credit scoring models, allowing the platform to confidently extend working capital loans to marketplace merchants and consumer credit lines to buyers 3738. The expanded credit access immediately cycles back into higher gross merchandise volume (GMV) on the retail marketplace 34.

This continent-level interlocking network effect explains why MercadoLibre trades at premium valuation multiples and successfully defends its territory against deep-pocketed global entrants. By Q3 2025, despite Amazon boasting a superior global net margin of 11.76% and robust cloud infrastructure revenue, MercadoLibre's tight regional integration allowed it to command total payment volume growth of 41% and maintain dominance in Brazil, Mexico, and Argentina, despite operating on a tighter 5.68% net margin 223435. The infrastructure cost and regional data history required for a competitor to replicate MercadoLibre's integrated three-node network is prohibitive 34.

Similarly, Tencent's WeChat demonstrates the power of functional integration. Expanding from a pure messaging protocol, WeChat integrated mobile payments and "Mini Programs," allowing thousands of offline and online businesses to leverage the platform's infrastructure without requiring users to download standalone applications 2923. The more businesses that deploy Mini Programs, the greater the convenience for users; the more users rely on WeChat, the more necessary it becomes for businesses to integrate, creating a pervasive ecosystem moat across mainland China 29.

Network Vulnerabilities and Multi-Homing Dynamics

A platform's absolute aggregate size does not guarantee the persistence of its network effects; the geometric structure and interconnectivity of the network nodes are equally critical 24. Research into platform economics reveals that highly clustered networks, even those boasting hundreds of millions of users, are remarkably fragile 2425.

If a network consists of a massive number of isolated, highly segregated local clusters, the overall platform is highly susceptible to targeted, asymmetrical competition 2425. The ride-sharing industry exemplifies this structural vulnerability. Uber, despite its massive global scale, operates on hyper-localized network effects. The presence of dense rider and driver liquidity in San Francisco provides zero functional utility to a user opening the application in Singapore or Manila 925. Consequently, entering a highly interconnected network is prohibitively expensive, but local entrants can easily target isolated clusters 25. Regional operators like Grab in Southeast Asia and Didi Chuxing in China were able to specialize, reach local atomic density, and out-compete Uber's localized clusters. Grab, for instance, integrated hyper-local features such as customer service in eight local Philippine dialects and automated chat translation - nuances Uber's monolithic global algorithm failed to prioritize 26. By 2016 and 2018, Uber was forced to retreat and sell its operations in China and Southeast Asia to these respective local incumbents 26. A network's ultimate defensibility is only as strong as the interconnectivity between its clusters 25.

Furthermore, network defensibility is fundamentally eroded by the presence of multi-homing. Multi-homing occurs when consumers use more than one platform for the exact same or a highly similar service 202127. For example, a driver keeping both the Uber and Lyft applications open simultaneously, or a consumer maintaining active profiles on multiple dating applications, engages in multi-homing 2028. Increased consumer exposure to substitutes weakens reliance on any single platform, effectively transferring pricing power back to the user and intensifying competition 2427.

| Platform Configuration | Buyer Behavior | Seller Behavior | Market Dynamic & Pricing Impact |

|---|---|---|---|

| SH-SH (Pure Monopoly/Duopoly) | Single-Homing | Single-Homing | Maximum lock-in. Market shares remain rigid; platforms dictate high extraction pricing. |

| SH-MH (Supply Multi-Homing) | Single-Homing | Multi-Homing | Buyers are locked in, forcing sellers to adopt multiple platforms to reach the total addressable market. Platforms typically subsidize or lower prices for sellers to ensure inventory. |

| MH-SH (Demand Multi-Homing) | Multi-Homing | Single-Homing | Sellers are locked in, allowing buyers to shop across platforms for the best price. Platforms must subsidize buyers to maintain traffic. |

| MH-MH (Fragmented Market) | Multi-Homing | Multi-Homing | Weakest network effects. High churn, intense price competition, and minimal platform defensibility. |

Table data synthesized from platform economics and Hotelling model analysis 1921.

Generative Artificial Intelligence and the Degradation of Data Flywheels

For the past decade, a major subset of network effect theory centered on "Data Network Effects" or "Data Flywheels" 345. The premise was straightforward: a digital product collects user data, utilizes that data to train machine learning models, improves the product's performance based on the training, attracts more users due to the improved performance, and subsequently generates even more data 345. This virtuous cycle was viewed as an impenetrable moat; an entrant simply could not match the incumbent's algorithm without the requisite years of historical user interaction data 45.

However, the rapid acceleration of Generative AI throughout 2024 and 2025 has begun to fundamentally erode the defensibility of traditional data network effects 4629.

The Proliferation of Synthetic Data

The primary technological threat to the proprietary data flywheel is synthetic data generation 46. Synthetic data refers to artificially generated datasets that accurately mimic real-world distributions, nuances, and statistical properties without relying on organic human generation 46. By the end of 2024, industry analysts estimated that over 60% of all data utilized to train AI models was synthetically generated, representing a massive shift from less than 1% in 2021 46.

Synthetic data bypasses the Cold Start Problem entirely for algorithmic products. Startups no longer need years of organic user interactions to build a sufficiently large dataset to train a highly capable machine learning model. Instead, leveraging foundation models, organizations can generate vast arrays of highly accurate, labeled datasets at scale, significantly accelerating product development across industries from healthcare to automotive autonomous systems 46. This technological shift democratizes access to high-quality training inputs, diminishing the proprietary advantage of legacy incumbents who spent years harvesting organic data 4630. Consequently, what was once considered a robust, compounding data network effect is increasingly being revealed as a temporary scale advantage that is easily leapfrogged by advanced synthetic generation capabilities and rapid fine-tuning methodologies 34649.

Multi-Model Orchestration and Agentic Hubs

Furthermore, the enterprise adoption of Generative AI demonstrates that foundation models themselves are fragmenting rather than consolidating into a single winner-take-all network effect 2930. The software ecosystem is trending rapidly toward a multi-model, open-source architecture 2930.

Enterprise CIOs report that they are no longer relying on a single monolithic provider. Instead, they increasingly mix and match closed-source frontier models (such as those from OpenAI, Google, and Anthropic) with highly capable open-source alternatives (like Llama and Mistral) depending on the specific use case, required latency, and data security compliance 2931. Advanced generative media pipelines, for instance, operate not on a single model, but on complex orchestration workflows that chain together an average of 14 distinct models to generate, refine, and edit digital assets 31. The open-source community's ability to rapidly close the capability gap with proprietary models prevents any single AI infrastructure provider from achieving total ecosystem lock-in 2931.

However, while underlying model infrastructure is commoditizing, the deployment of AI agents deployed within organizations is actively altering human and corporate networks. Research indicates that GenAI tools act as "translators" and "knowledge catalysts," drastically reducing the friction of interpersonal collaboration 32. Paradoxically, this may flatten internal collaboration networks, as junior or highly specialized employees leveraging GenAI experience outsized gains in network centrality compared to veteran generalists 32. Concurrently, legal and economic scholars warn that dominant, highly capable autonomous AI agents could eventually consolidate external market negotiations. By acting as the primary intermediaries for complex procurement and scheduling tasks, these agents could drive market concentration through traditional (non-data) network effects, forming powerful, scale-free B2B hubs that lock out competitors lacking equivalent negotiation leverage 33.

Regulatory Interventions and Interoperability Mandates

Beyond technological shifts, the structural defensibility of digital platforms is currently undergoing a severe regulatory stress test, primarily driven by the European Union's Digital Markets Act (DMA). The explicit legislative goal of the DMA is to enhance the contestability of digital markets by forcibly lowering switching costs and breaking the proprietary network effects of designated "gatekeepers," most notably Apple and Google 3435.

The DMA, fully applicable to gatekeepers since March 2024, targets the structural advantages of dominant mobile ecosystems through two critical mechanisms 3435: 1. Data Portability (Article 6): Gatekeepers are required to provide comprehensive, wireless transfer solutions enabling users to migrate their entire digital identities - including contacts, calendar events, messages, photos, and saved passwords - between rival operating systems (e.g., seamlessly moving from iOS to Android) 3536. In response, providers have developed infrastructure like Apple's AppMigrationKit and cross-platform eSIM transfer protocols, which directly attack the procedural switching costs that previously locked users into specific hardware ecosystems 35. 2. Horizontal Interoperability (Article 7): The legislation mandates that dominant messaging services open their closed architectures, allowing users of third-party, alternative messaging applications to communicate directly with users trapped inside the gatekeeper's proprietary network 3437.

Economic theory models the competitive impact of these interventions through the lens of multi-homing 2124. Under normal market conditions, dominant platforms design proprietary networks to force single-homing, maximizing their leverage over pricing and user attention by creating walled gardens 19. By legally mandating interoperability, regulators aim to facilitate seamless multi-homing, preventing an incumbent from utilizing a locked-in user base as an insurmountable barrier to entry 2427.

However, platform economists note a regulatory paradox: horizontal interoperability obligations can inadvertently generate anti-competitive side effects 27. If users can access the full communication features of a rival entrant without ever leaving the dominant incumbent's platform, they have zero incentive to fully migrate 2757. Consequently, interoperability may merely allow competition in the market while fundamentally preventing competition for the market, ensuring the incumbent maintains its status as the central, indispensable hub 27.

Initial reviews of the DMA by the European Commission in mid-2026 indicate that consumers have shown less practical interest in cross-platform messaging interoperability than originally anticipated by legislators 37. As a result, regulators have paused plans to extend interoperability mandates to broader online social networking services, choosing instead to investigate potential cloud computing interoperability by 2027 37. This empirical outcome suggests that while regulatory pressure can alleviate procedural and technical switching costs, the psychological, relational, and social graph stickiness of a well-established network effect remains highly resilient 363757.

Measurement Metrics and Valuation Premiums

The extreme focus on network effects in venture capital and public equities is directly correlated with valuation multiples. Investors actively seek out network-driven companies because their distinct financial profile generates highly asymmetric, outsized returns upon market maturity 258.

Standard software-as-a-service (SaaS) businesses, IT service providers, and hardware manufacturers face linear or gradually degrading unit economics as they scale. They must continually invest heavily in sales, marketing, and R&D to acquire the next marginal customer 2059. By contrast, companies exhibiting strong, cross-border network effects experience improving unit economics. Evaluating the true health of a network effect requires analyzing specific metrics: the ratio of organic to paid users, cohort retention over time, and localized Customer Acquisition Cost (CAC) 17. Once a networked platform passes its tipping point, the organic share of new users increases dramatically relative to paid acquisition 17. The existing user base essentially executes the marketing and onboarding functions autonomously, driving the blended CAC down, while the expanding utility of the dense network drives Customer Lifetime Value (LTV) upward 131720. Theory dictates that newer user cohorts joining a mature network should exhibit higher retention rates than older cohorts who joined when the network lacked density, though real-world market saturation often complicates this metric 17.

Because of these structural margin advantages and exponential growth patterns, financial markets award massive valuation premiums to verified network effect businesses. Extensive M&A and public market data analyzed through mid-2025 demonstrates that while asset-heavy hardware companies trade at a median of 1.4x Enterprise Value-to-Revenue (EV/Revenue) and IT services languish at 1.3x EV/Revenue, software platforms - where network effects are most heavily concentrated - command a median of 3.0x EV/Revenue 59. Top-tier network platforms regularly exceed 6.0x to 10.0x EV/Revenue during high-growth phases due to their high capital efficiency 59.

In private markets and early funding rounds (Series A - C), the valuation dispersion is even more pronounced. Fintech companies operating multi-sided marketplaces or neobanks utilizing integrated network infrastructure trade at average multiples of 13.7x (private) to 14.4x (M&A) revenue, significantly outpacing the broader public fintech sector average of 8.8x 6061. These astronomical multiples are supported by the "fat-cat" pricing dynamics discussed earlier; once users are locked into the network, the platform enjoys immense, highly predictable cash flow extraction 61.

This stark valuation reality inherently incentivizes corporate management teams to dress up linear, low-margin business models in the vocabulary of network economics. If a company can convince the financial market that it possesses a compounding network effect, it can access significantly cheaper capital, fund aggressive global expansion, and secure a premium exit valuation before the fundamental lack of underlying defensibility is exposed to the public markets 2.

Conclusion

Network effects remain the undisputed apex of digital competitive strategy, responsible for the vast majority of technology sector value creation since the commercialization of the internet. However, true network effects are exceptionally rare, notoriously difficult to ignite due to the Allee threshold of the Cold Start Problem, and mathematically distinct from standard viral marketing or linear economies of scale.

The frequent failure of founders, investors, and industry analysts to correctly identify the presence of a network effect stems from a systemic conflation of growth mechanics with defensibility mechanics. A digital platform that scales rapidly due to frictionless viral acquisition or massive centralized content licensing does not inherently possess a network effect. Without the decentralized, compounding utility generated directly by user-to-user interactions, these platforms remain highly vulnerable to capital-rich competitors and shifting consumer preferences, regardless of their aggregate user count.

Looking forward, the fundamental architecture of digital defensibility is shifting. Tightly integrated, cross-platform ecosystems that fuse marketplace liquidity with proprietary fintech and logistics infrastructure currently offer the most resilient moats, successfully fending off both global monopolists and regional upstarts. Conversely, traditional data flywheels are rapidly deteriorating under the computational pressure of generative artificial intelligence and the proliferation of synthetic data generation. Navigating the modern digital economy requires stripping away the marketing rhetoric surrounding tech platforms and rigorously evaluating the mathematical laws, structural clustering, and true procedural switching costs that ultimately dictate long-term market survival.