Market category creation and capture

The strategic dichotomy between creating a new market category and capturing market share within an existing ecosystem represents a fundamental divergence in corporate strategy, cognitive positioning, and capital allocation. Traditional market capture operates within established paradigms, requiring firms to compete on incremental feature improvements, price efficiency, and distribution. In contrast, category creation involves defining a novel problem space, educating the market on its parameters, and positioning a firm as the inevitable solution. Understanding how categories are built and maintained requires a synthesis of cognitive psychology, market sociology, empirical financial data, and global macroeconomic conditions. The mechanisms that drive market categorization determine how consumers evaluate products, how investors deploy capital, and how emerging technologies or geographic nuances reshape established industries.

Cognitive Mechanisms of Market Categorization

The formation and acceptance of a market category are fundamentally cognitive processes. Before a product can capture market share, the market audience - consumers, analysts, and investors - must be able to process, evaluate, and classify it into a mental framework.

Category Learning and Schema Processing

Cognitive categorization is a fundamental human ability involving the conceptual differentiation of experiences, objects, and ideas 1. Categorization theorists often analyze the classification of objects using taxonomies characterized by hierarchical levels of abstraction: superordinate, basic, and subordinate levels 12. Prevailing psychological models of category learning include prototype theory, which posits that humans learn a category by internalizing its idealized prototype, and exemplar theory, which suggests that categorization relies on recalling specific past examples 1.

The neural mechanisms underlying category learning are complex and distributed across multiple brain systems. The COVIS (COmpetition between Verbal and Implicit Systems) theory, proposed by Ashby et al., indicates that explicit, rule-based category learning relies heavily on a broad neural network encompassing the prefrontal cortex, anterior cingulate, and medial temporal lobes 3. In contrast, implicit, information-integration categorization depends on the striatum and premotor cortex 3. During the transition from initial category exposure to deep expertise, face-selective inferotemporal cortex, lateral prefrontal cortex, and the dorsal striatum are highly responsive to stimuli situated near category boundaries 4. This heightened neural activity reflects the cognitive effort required to classify ambiguous market entrants, indicating that educating a market on a new category demands substantial cognitive resources from the audience 45.

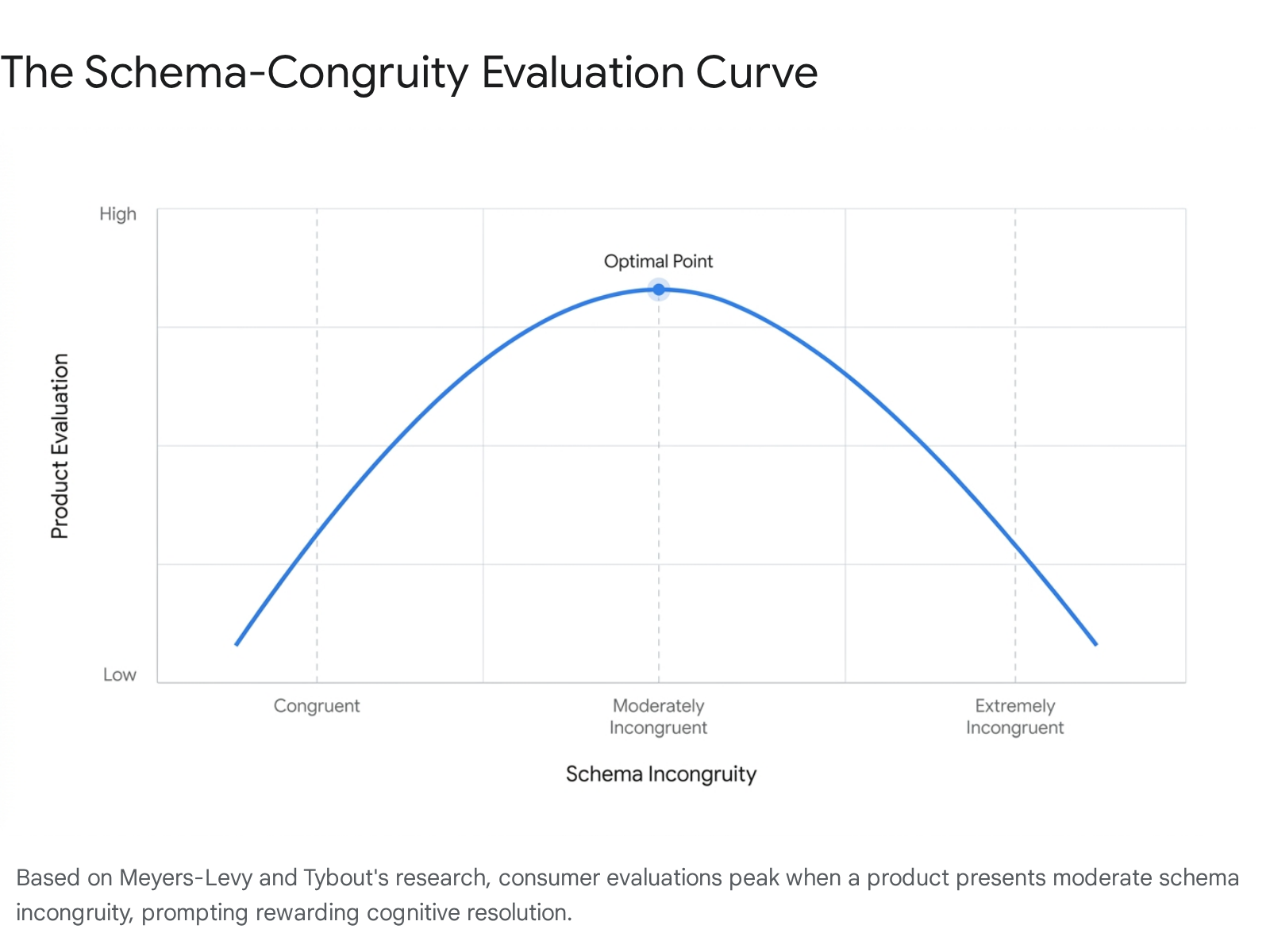

Schema Congruity and Product Evaluation

In a commercial context, consumers use category knowledge to access mental representations, or schemas, which define the core features of a product class and set a baseline of expectations 12. When novel products enter the market, they are evaluated based on their alignment with these existing schemas.

Schema-congruity theory, advanced by researchers Meyers-Levy and Tybout, posits that the level of congruity between a product and a general product category schema directly influences information processing and subsequent evaluation 678. Empirical research demonstrates that products presenting moderate incongruity - a partial match that blends familiar category attributes with novel elements - stimulate cognitive processing that leads to more favorable evaluations than products that are perfectly congruent or extremely incongruent 689.

A perfect match represents a pure "me-too" product that is easily processed but generates little excitement or differentiation. Conversely, an extreme mismatch triggers confusion and negative affect, as the consumer cannot resolve the categorization 9. Moderate incongruity, however, prompts a cognitive resolution process. When a consumer successfully resolves this tension through subtyping resolution, the psychological experience is rewarding, resulting in heightened positive affect and superior product evaluation 89.

Sociological Dynamics and the Categorical Imperative

Beyond individual cognition, categorization serves as a critical social sorting mechanism that dictates resource allocation and market viability.

Intermediary Labeling and the Illegitimacy Discount

In mediated markets, the categorization of products by intermediaries - such as securities analysts, industry critics, or procurement officers - is critical to efficient interaction between producers and consumers 10. Sociologist Ezra Zuckerman conceptualized the "categorical imperative," which dictates that products and firms must align with established categories to be evaluated by market audiences 1112. When an entity spans multiple categories or fails to fit neatly into an existing taxonomy, it imposes high cognitive costs on evaluators. Consequently, it risks being ignored or penalized with an "illegitimacy discount" 101213.

The history of the microwave oven illustrates this imperative. Initially marketed in electronics departments alongside amplifiers as a "brown good," the device faced severe market friction because consumers lacked a framework for evaluating an electronic box as an oven . It was only when manufacturers repositioned the microwave as a "white good," placing it in home appliance departments alongside stoves and refrigerators, that it acquired a fixed identity and achieved mainstream market success .

Distinctiveness and Specificity in Label Assignment

Category creation is the deliberate social construction of a new evaluative standard. Novel categories redraw the boundaries of market attention, bringing about new interpretations and enacted practices 14. Research on how mediators assign labels suggests that moderate levels of specificity, combined with moderate or maximal distinctiveness, allow mediators to economize on cognitive costs while still differentiating the product 10.

While spanning categories is historically penalized under the categorical imperative, modern sociological research indicates that hybrid categories can sometimes be utilized as strategic devices 11. Categorical purity becomes less critical to evaluators when they operate independently of previous category norms, or when the status and past performance of the producer provide alternative screens of evaluation, granting them the freedom to experiment with unconventionality 1115.

Strategic Paradigms in Category Theory

The distinction between creating a market and capturing existing market share defines a firm's operational trajectory and long-term valuation potential. Market capture strategies operate within the "existing market trap," where demand is proven, and firms compete on incremental differentiation, leading to hyper-competitive environments characterized by feature parity 171816.

The Category Design Framework

Category creation requires reframing the market around a new class of solutions by exposing a previously unarticulated problem 1721. The methodology popularized by the "Play Bigger" framework insists on the simultaneous execution of product design, company design, and category design - a triad referred to as the "Magic Triangle" 2223.

Rather than engaging in comparison marketing, category designers execute a "No Ocean Strategy," attempting to eliminate the concept of competition entirely by establishing a space where no direct comparisons exist 23. This process relies heavily on narrative design and market evangelism. Effective category leaders use strategic language to name the problem, borrowing scientific credibility (e.g., "Nootropics," "Cosmeceuticals") or defining a specific pain point (e.g., "Decision Fatigue," "Inbound Marketing") 1825. By articulating a provocative Point of View (POV), the creator establishes a framework wherein their specific product becomes the only logical solution 222519.

The table below outlines the conceptual differences between established strategic market paradigms:

| Strategic Paradigm | Primary Objective | Market Assumption | Competitive Dynamic | Cognitive Mechanism |

|---|---|---|---|---|

| Market Capture | Maximize share of existing demand. | Demand is known and finite. | Zero-sum; competes on features, price, and efficiency. | Leverages existing product schemas. |

| Blue Ocean Strategy | Create uncontested market space. | Demand can be unlocked through value innovation. | Makes competition irrelevant by altering value curves. | Modifies existing schemas incrementally. |

| Category Design | Define a net-new problem and solution space. | Demand does not exist until the problem is evangelized. | Establishes a monopoly by becoming synonymous with the category. | Forces subtyping resolution and new schema formation. |

The Commoditization Cycle

Even successfully designed categories inevitably face market saturation. The commoditization cycle dictates that competitive advantage erodes across four predictable phases 20: 1. Functionality: A firm introduces a novel technique or process that solves a problem. 2. Reliability: As credible competitors emerge, differentiation shifts to consistent performance and uptime. 3. Convenience: With multiple functional and reliable options, customers differentiate based on user experience, ecosystem integrations, and service efficiency. 4. Price: Once products achieve parity in functionality, reliability, and convenience, the market transitions into a zero-sum pricing battle 20.

To sustain market dominance, category leaders must continually engage in new category creation, evolving their offerings to act as an internal blueprint that guides subsequent product roadmaps and prevents the firm from sliding into the terminal pricing phase 21.

Empirical Outcomes of Entry Timing

A pronounced tension exists in empirical research regarding the financial viability of category creation versus fast-follower market capture.

Academic Perspectives on First-Mover Failure

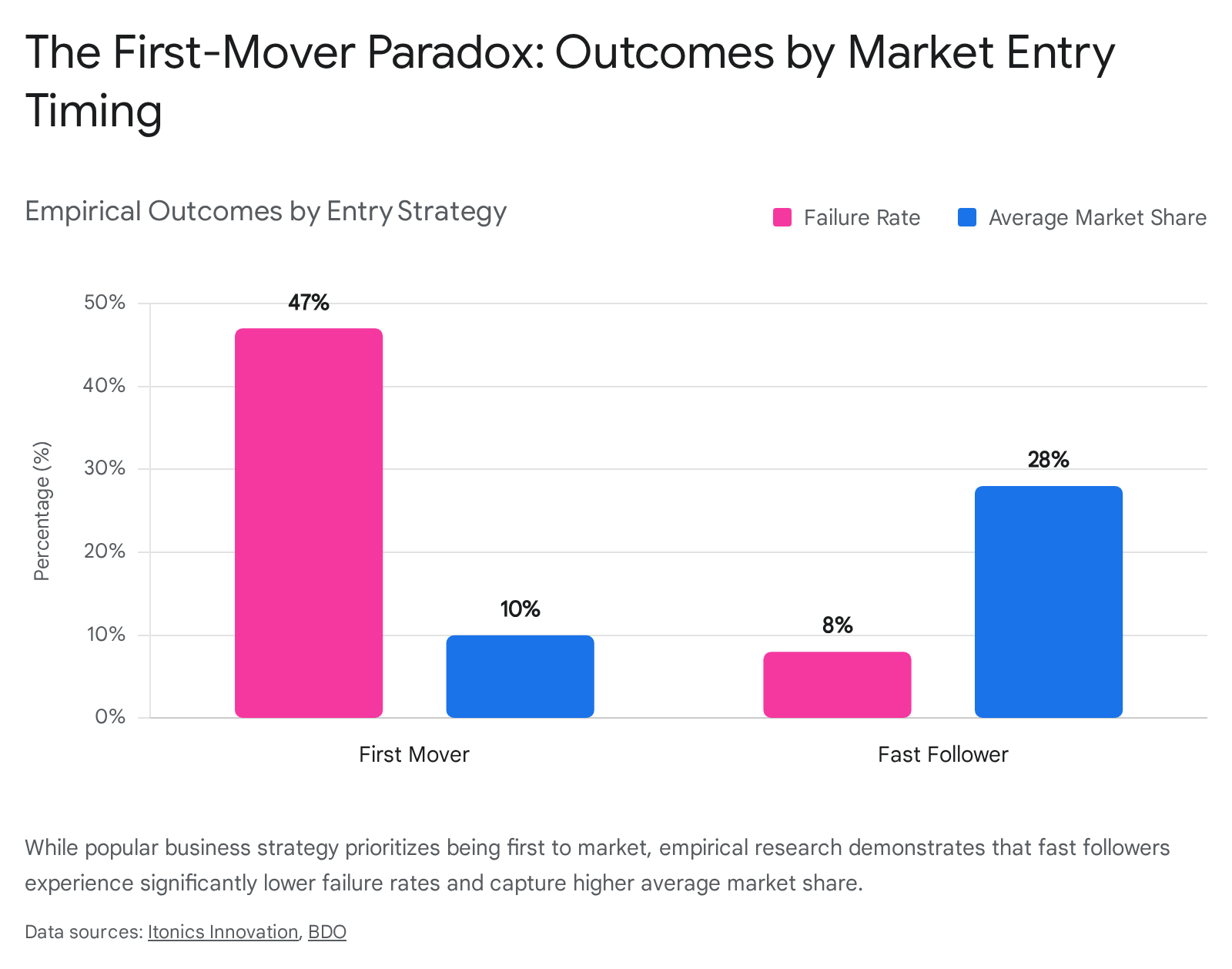

Proponents of the category design framework argue that the dominant "Category King" ultimately captures 76% of the total market capitalization within a given space, leaving competitors to fight over the remaining 24% 172122. This statistic underpins the motivation for massive venture capital investments in early-stage category creators.

However, academic studies on market entry timing present a conflicting reality for initial innovators. Research by marketing professors Peter Golder and Gerard Tellis, which analyzed hundreds of brands across multiple product categories, found that strict first-mover companies suffer a 47% failure rate and capture an average market share of only 10% 2324. In contrast, early market followers exhibit a failure rate of just 8% and capture an average of 28% market share 2324.

The Fast-Follower Advantage

This statistical discrepancy highlights the immense capital and cognitive costs of market education borne by the first mover 25. If a pioneering firm lacks the learning velocity required to adapt to market feedback, it burns capital subsidizing market infrastructure without retaining leadership 2333. Fast followers leverage proven demand, monitor the first mover's mistakes, and allocate their capital toward product refinement and competitive positioning 25.

Harvard Business School research corroborates this dynamic, indicating that first-movers achieve sustainable competitive advantage in only 37% of new market categories, whereas fast-followers demonstrate superior long-term profitability in 42% 2325. Creating a category and ultimately capturing its value requires a firm to possess not just speed to market, but the organizational maturity to maintain infrastructure scale as the category evolves 23.

Macroeconomic Influence on Category Financing

The financial viability of category creation is inextricably linked to macroeconomic conditions, dictating how aggressively firms can subsidize the high costs of market education and customer acquisition.

The Transition from Zero Interest Rate Policy

For more than a decade following the 2008 Great Recession, the technology and venture capital sectors operated under a Zero Interest Rate Policy (ZIRP) environment 2627. ZIRP dramatically lowered the cost of capital, giving investors a massive appetite for speculative bets and allowing startups to run at a loss for years to subsidize rapid expansion 2627. Venture capital models heavily prioritized the "Belief Rate" - the conviction that a company could eventually monopolize a category and generate outsized future cash flows 26. This artificially sustained the Minimum Viable Product (MVP) model, enabling firms to launch underdeveloped products and iterate post-launch without immediate financial penalty 28.

The conclusion of the ZIRP era, driven by persistent inflation and interest rate hikes, dismantled this operational playbook 2728. With the risk-free rate of return rising nearly tenfold, the cost of capital spiked, compressing venture valuations and shifting investor focus aggressively toward profitability and business fundamentals 262829. In a post-ZIRP environment, founders can no longer outspend competitors simply to capture market share if the unit economics are structurally unsound. Quality and operational efficiency have replaced pure revenue growth as primary differentiators 2829.

Stage-Based Financial Metrics and Capital Allocation

In this capital-constrained ecosystem, tracking appropriate stage-based metrics is critical for validating whether a firm is successfully building a durable category 29. Vanity metrics heavily promoted by advertising platforms (such as high click-through rates) often mask highly inefficient growth, leading to unpredictable spikes in Customer Acquisition Cost (CAC) 38.

Venture capital and growth equity currently assess category leaders through stringent operational benchmarks across different growth stages:

| Financial Metric | Primary Function | Target Benchmark | Market Implication |

|---|---|---|---|

| LTV:CAC Ratio | Measures the lifetime value (LTV) expected from a customer versus the cost to acquire them (CAC). | > 3:1 | Indicates sustainable acquisition economics. Ratios below 1:1 signal terminal value destruction 3040. |

| Net Revenue Retention (NRR) | Measures revenue growth from existing customers, factoring in upsells and churn. | > 100% | High NRR indicates durable product value, high switching costs, and category staying power 2930. |

| Burn Multiple | Assesses how much capital is burned to generate one net new dollar of Annual Recurring Revenue (ARR). | < 1.0x | A multiple under 1.0x demonstrates highly efficient capital allocation and operating leverage 30. |

| Gross Margin | Calculates revenue minus cost of goods sold. | > 70% (SaaS) | Proves that scaling the business improves underlying economics rather than exacerbating losses 29. |

Technological Disruptions in Market Categorization

The rapid advancement of artificial intelligence is currently forcing a real-time reconfiguration of enterprise software categories. Capital deployment in recent years demonstrates a massive concentration in AI infrastructure and vertical-specific applications 3132.

The Shift from Copilots to Autopilots

Venture capital allocation reflects a systemic belief that the entire computing stack is being rewired for AI workloads. Major venture firms, such as Andreessen Horowitz (a16z), have allocated billions specifically toward foundational AI infrastructure, under the premise that storage, compute, and orchestration are being rebuilt from the ground up 3344.

At the application level, a fundamental category transition is occurring from "Copilots" to "Autopilots." Initially, AI software was positioned as a Copilot - a traditional software-as-a-service (SaaS) tool sold to a professional (e.g., a lawyer, programmer, or designer) to augment their productivity, leaving ultimate judgment to the human user 34.

However, as foundational models develop advanced reasoning, the market is shifting toward Autopilots, which sell the completed work product directly to the end consumer 34. This shift from standard SaaS to "Services as Software" fundamentally expands the Total Addressable Market (TAM). Because corporate budgets for human labor and outsourced services are estimated to be six times larger than budgets for software tools, Autopilots bypass traditional software procurement entirely to capture labor spend 34.

Vertical Software and Incumbent Vulnerability

The Autopilot category wedge is proving most effective in high-volume, low-judgment roles - such as indirect procurement, IT support, and basic recruitment screening - capturing immediate value where human labor is inefficient 34. Firms competing in this environment face the classic innovator's dilemma. Existing Copilot providers hesitate to fully transition to Autopilots because selling an automated outcome actively disintermediates their own human software users 34. This hesitation creates an opening for pure-play vertical AI startups to define completely new categories of intelligent, autonomous enterprise execution, securing venture capital on terms that favor localized monopoly creation over broad, horizontal software competition 3234.

Geographic Divergence in Category Evolution

Market creation dynamics are heavily contingent on regional regulatory frameworks, legacy infrastructure, and cultural attitudes. Innovations that dominate in one hemisphere often fail or take entirely different forms in another.

Emerging Economy Copycats and Innovation Trajectories

In developing regions, market category emergence frequently begins with Emerging Economy Copycats (EECs). Rather than inventing net-new categories with high failure rates, these firms initially scale by imitating proven Western business models and applying them to local markets 3536. Early iterations of firms like Careem, Souq, and Talabat in the MENA region thrived not through pure invention, but through deep localization - adapting global models to accommodate unique regional payment methods, delivery infrastructure gaps, and specific cultural preferences 36.

Over time, successful EECs follow a trajectory from duplicative imitators to creative innovators 35. Utilizing the CHAIN framework (Combinative, Hardship-surviving, Absorptive, Intelligence, and Networking capabilities), these firms leverage their vast domestic markets and organizational resilience to evolve into globally competitive entities 35. China's technological evolution exemplifies this shift, transitioning from pure manufacturing imitation to pioneering complex digital ecosystems, electric vehicle infrastructure, and advanced artificial intelligence 3537.

Addressing Non-Consumption in Latin America and Africa

In emerging markets, the most profound category creation strategies focus heavily on "non-consumption" - identifying populations that possess an acute need for a service but lack access due to prohibitive costs, structural exclusion, or geographic barriers 3839.

Nubank in Brazil: In 2013, the Brazilian banking sector was a heavily concentrated oligopoly where five major banks controlled roughly 80% of total assets 5140. Consumers faced 400% annual interest rates, excessive monthly fees, and 45-day wait times to open basic accounts, effectively locking massive portions of the population out of the formal credit system 3951. Nubank created a new category of digital-first, zero-fee banking. By operating entirely without physical branches, Nubank generated unparalleled operating leverage, serving customers at a fraction of incumbent costs 51. By designing a product specifically to eliminate the friction points of the legacy system, the company captured over 100 million customers across Latin America, becoming the region's largest financial institution by customer count 5140.

M-Pesa in Kenya: Launched in 2007 by Safaricom in partnership with Vodafone, M-Pesa created the mobile real-time payment category in Africa 5341. Rather than competing with traditional banks for the small fraction (18.9%) of Kenyans who had formal financial access, M-Pesa targeted the massive unbanked population 4142. The platform's success was driven by utilizing Safaricom's existing 80% telecom market share and converting its vast network of airtime resellers into cash-in/cash-out agents, entirely bypassing traditional banking infrastructure 5341. M-Pesa's category creation pulled millions into the formal economy, evolving from a simple remittance tool into a comprehensive financial ecosystem offering savings and credit services 42.

The Asian Super-App Phenomenon

The emergence of "super-apps" - omnibus applications bundling messaging, digital payments, ride-hailing, e-commerce, and healthcare into a single platform - represents a significant geographic divergence in digital category evolution. In China and Southeast Asia, platforms like WeChat, Alipay, and Grab functionally define the digital lifestyle 4344.

The dominance of the super-app category in Asia is rooted in specific institutional and structural contexts. Large populations completely bypassed traditional credit card infrastructure, adopting mobile payments via QR codes en masse 43. Furthermore, Asian consumers generally exhibit higher trust in large conglomerates dominating daily life, and early regulatory environments permitted loose data privacy and competitive practices 43.

Conversely, US and Western attempts to create super-apps face immense friction. Legacy payment rails based on credit and debit cards are deeply entrenched, mitigating the necessity for mobile-first financial wallets 43. Additionally, Western consumers tend to view massive technology conglomerates with intense suspicion regarding antitrust and data privacy concerns 43. While US platforms continually integrate adjacent services, full category realization of the omni-purpose super-app remains structurally limited by these divergent historical trajectories 4345.