Impact of artificial intelligence on jobs and skills in 2026

Introduction: The Structural Reallocation of Labor

By 2026, the global labor market has definitively transitioned from the speculative hype of the early artificial intelligence boom into a phase of profound, empirical structural realignment. The widespread deployment of generative artificial intelligence (GenAI), advanced predictive algorithms, and sophisticated robotic automation has catalyzed one of the most significant reallocations of human capital in modern economic history. However, the empirical reality of this transition diverges sharply from the early, often sensationalized dystopian narratives of mass human obsolescence. A rigorous analysis of 2024 - 2026 data from impartial international institutions - including the International Labour Organization (ILO), the Organisation for Economic Co-operation and Development (OECD), the International Monetary Fund (IMF), and peer-reviewed economic literature - reveals a highly nuanced and complex landscape. Artificial intelligence functions fundamentally as a task-disrupting technology rather than a purely occupational-destroying force, setting off a cascade of secondary and tertiary economic effects across global markets 112.

The integration of AI into the global economy is characterized by distinct polarities and paradoxes. It has fundamentally upended traditional paradigms of skill-biased technological change. Cognitive, white-collar roles - historically shielded from automation - are now positioned at the epicenter of disruption, while the physical demands of building out AI infrastructure have inadvertently fueled a renaissance in specialized blue-collar trades 3. Geopolitically, the technological acceleration threatens to drastically widen the chasm between advanced Western economies, which are leveraging AI to offset aging demographics and shrinking workforces, and the Global South, where a severe lack of digital preparedness risks stranding a burgeoning youth population and disrupting established development models 47. Furthermore, within the modern enterprise, a severe crisis of technological governance has emerged. The organic, bottom-up proliferation of "shadow AI" continues to outpace top-down corporate strategy, creating a fractured, two-tier workforce divided between hyper-productive algorithmic "super-users" and an increasingly anxious, alienated general employee base 59.

This comprehensive research report provides an exhaustive, data-driven analysis of the future of work in 2026. By prioritizing impartial institutional data and peer-reviewed labor economics over speculative corporate consultancy forecasts, the analysis deconstructs the empirical realities of how AI is reshaping jobs, redefining critical skills, and altering the trajectory of global careers.

Deconstructing the Lump of Labor Fallacy: Task Automation Versus Occupational Elimination

Public discourse and early corporate anxieties regarding artificial intelligence have been disproportionately influenced by the "lump of labor" fallacy. This enduring macroeconomic misconception posits that there is a fixed, finite quantum of work to be performed within an economy, and that any technological automation of this work inherently results in a direct, one-to-one reduction in human employment 611. Consequently, media reporting has frequently conflated the technical capability to automate specific tasks with the imminent destruction of entire professions. For example, early studies indicating that 80% of the United States workforce could have at least 10% of their work tasks affected by large language models (LLMs) were routinely misinterpreted in popular media as a projection that 80% of all jobs would be eliminated 6.

Macroeconomic data aggregated through 2025 and early 2026 systematically dismantles this paradigm, highlighting the critical distinction between localized task automation and systemic occupational elimination.

The Dynamics of Task Reallocation and Employment Growth

According to updated research from the ILO and recent working papers from the National Bureau of Economic Research (NBER), technical exposure to AI - even highly concentrated exposure - does not automatically equate to job destruction. The ILO strictly defines "exposure" as a measure of the technical feasibility of an AI system to assist with, or autonomously execute, specific tasks within a broader occupational portfolio, rather than a definitive prediction of human displacement 12. While up to 30% of workers in advanced economies could see at least 50% of their daily tasks disrupted or handled by generative AI, overall aggregate employment figures have not witnessed commensurate, economy-wide declines 23.

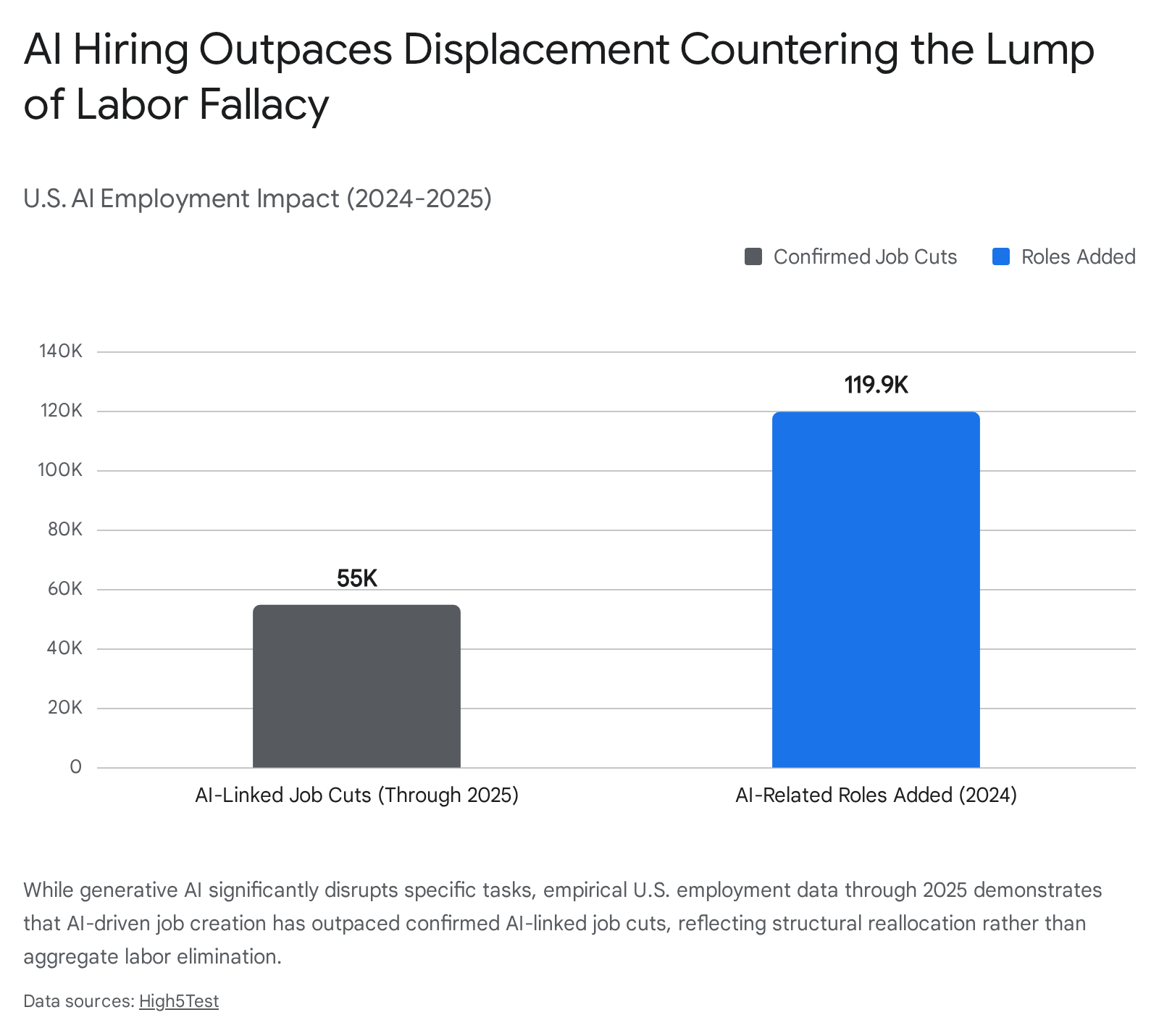

The empirical evidence indicates that as AI absorbs routine, repetitive cognitive tasks - such as basic data entry, preliminary code generation, standard communications, and document summarization - human labor is systematically reallocated toward higher-value, complementary activities that require strategic oversight. The Stanford Digital Economy Lab and the Yale Budget Lab, tracking labor market indicators through late 2025, found virtually no evidence of immediate, economy-wide job loss or wage decline directly attributable to AI adoption 2. In fact, hiring data throughout 2024 revealed that AI-related job creation in the United States, which added approximately 119,900 specialized roles, vastly exceeded the roughly 55,000 confirmed, AI-driven job cuts tracked through 2025 1.

Labor economists, notably David Autor of MIT, utilize the concept of "one-way fungibility of expertise" to explain this phenomenon. Autor's framework illustrates that while automation can replace experts in routine, highly structured domains, it simultaneously augments expertise by elevating the baseline of human capability and allowing workers to pivot to tasks requiring complex judgment 7. Historically, when productivity gains from technological integration lower the unit cost of a service, it frequently induces higher market demand for that service or adjacent services, thereby sustaining or even increasing net labor demand. Furthermore, the deployment of AI generates entirely new categories of necessary tasks - ranging from context engineering and algorithmic auditing to AI systems integration and ethics compliance - which expands the total volume of economic activity 81415.

Skill Compression and Total Factor Productivity Growth

A defining characteristic of the 2026 labor market is the phenomenon of "skill compression." Controlled field experiments and randomized trials documented in peer-reviewed economics journals repeatedly demonstrate that AI tools deliver disproportionately large productivity and quality benefits to less-experienced or historically lower-performing workers 2. Across highly analytical domains such as legal research, software development, customer support, and professional writing, studies report 15% to more than 50% reductions in task-completion times when utilizing generative AI 2. By artificially raising the floor of baseline technical competency, AI algorithms actively narrow the performance gap between novices and seasoned experts. This dynamic challenges traditional, hierarchical wage premiums that were historically based purely on the accumulation of rote execution experience, forcing a revaluation of what constitutes unique human expertise.

From a macroeconomic modeling perspective, the integration of generative AI is projected to significantly impact Total Factor Productivity (TFP) growth, though economists debate the timeline and magnitude. Structural models, such as those analyzed by Acemoglu (2025), estimate that if approximately 4.6% of tasks are profitably replaced by AI, yielding a 27% increase in productivity due to labor cost savings, it will lead to TFP gains of roughly 0.7% over the next decade 24. More aggressive baseline scenarios modeled by the IMF suggest that rapid AI integration could raise global TFP by 0.8% to 2.4% over a similar time horizon, potentially expanding global GDP by nearly 4% under high-growth assumptions 4. However, achieving these macroeconomic gains is heavily contingent on an economy's structural composition, capital investment, and its institutional readiness to retrain and adapt its human capital to a radically restructured task environment 4. Disagreements in the macroeconomic literature frequently reflect the well-documented "productivity J-curve," where the initial costs of technological implementation and organizational redesign temporarily depress measured productivity before long-term, exponential gains are realized 2.

The Paradigm Inversion: Generative AI (White-Collar) vs. Predictive Robotics (Blue-Collar)

Historically, technological automation has followed a predictable pattern of "skill-biased" technological change. Throughout the late 20th and early 21st centuries, automation primarily substituted for routine, physical, and manual skills common in middle- and low-wage blue-collar jobs, such as manufacturing assembly and basic clerical work. Conversely, this same technology complemented the non-routine cognitive skills of highly educated, higher-paid white-collar professionals, cementing a widening income inequality gap 3. The advent of advanced large language models and generative AI has radically upended and inverted this historical precedent.

The Cognitive Automation Wave and White-Collar Exposure

Generative AI demonstrates a unique, unprecedented capacity to parse, synthesize, and execute non-routine, cognitive, and text-based tasks at scale. Consequently, the occupations most heavily exposed to immediate disruption in 2026 are high-paying fields that traditionally required advanced university degrees. These include finance and accounting, legal services, software architecture, journalism, and administrative corporate management 39. Recent capability-based measurements from the ILO and the OECD identify business professionals, actuaries, mathematicians, and senior corporate managers as exhibiting the absolute highest gradients of AI exposure 110.

Because the core functions of these white-collar roles are primarily digital and information-based, the friction involved in applying an LLM to their daily workflows is minimal. Tasks such as drafting complex legal briefs, synthesizing quarterly financial reports, writing boilerplate software code, and generating targeted marketing copy have seen massive, immediate efficiency gains 9. The ability of AI to seamlessly replicate these cognitive tasks has led to a fundamental restructuring of the knowledge-worker economy, primarily manifesting not as mass layoffs of senior staff, but as a severe contraction in entry-level hiring pipelines.

The Blue-Collar Boom and the Demands of AI Infrastructure

In stark, paradoxical contrast to the white-collar experience, generative AI has a negligible immediate impact on non-routine physical labor. Barring sudden, currently unscaled breakthroughs in the commercial deployment of autonomous, general-purpose humanoid robotics, male-dominated, manually intensive blue-collar sectors face the absolute least exposure to current AI paradigms 3. The movement, physical discipline, and spatial awareness required in advanced manufacturing, plumbing, electrical work, and complex construction cannot currently be replicated by large language models 9.

Far from making manual labor obsolete, the proliferation of artificial intelligence has triggered a massive, unforeseen surge in demand for skilled blue-collar and trade workers. The exponential scaling of AI necessitates unprecedented physical infrastructure buildouts, specifically hyperscale data centers, advanced liquid cooling systems, and massive upgrades to national electrical grids to support the immense energy consumption of AI computations. By early 2026, the demand for specialized robotics technicians had spiked by 107%, HVAC engineers by 67%, and specialized construction roles by 30% relative to the pre-GenAI baseline .

The United States data center workforce alone - comprising power electronics specialists, substation construction crews, and network technicians - reached 500,000 in 2023 and is actively projected to grow by an additional 30% to 650,000 workers by the end of 2026 18. Furthermore, economic modeling indicates that each specialized data center job generates an additional 3.5 indirect local jobs, fueling regional economic booms in hardware-adjacent sectors 18. This dynamic is fundamentally redefining the concept of the "skilled trade." Modern blue-collar jobs are increasingly specialized, digital-first positions where workers utilize predictive (rather than generative) AI to optimize physical outputs - for example, utilizing digital twins for structural maintenance or relying on predictive algorithmic models for complex supply chain logistics 14. As a direct result, specialized blue-collar careers are arguably standing on a more solid, automation-resistant, and economically lucrative footing in 2026 than many mid-tier, white-collar knowledge roles.

The Entry-Level Squeeze and the Graduate Crisis

One of the most alarming and structurally disruptive labor market phenomena verified by 2025 - 2026 data is the disproportionate impact of AI on early-career professionals and recent university graduates. Peer-reviewed economic literature and large-scale employment surveys demonstrate a stark, widening divergence in employment trends based on age and experience level within occupations that are highly exposed to AI.

Research aggregating online job postings and administrative payroll data reveals that while senior employment remains remarkably robust, entry-level hiring in fields vulnerable to AI substitution has contracted severely. An exhaustive study analyzing over 285 million online job postings indicated a 12% to 18% decline in labor demand for occupations with high AI-substitution scores, with these losses heavily concentrated in entry-level positions that require neither advanced degrees nor extensive prior experience 11. Similarly, analysis of United States Current Population Survey (CPS) and ADP payroll data confirmed that workers aged 22 - 25 operating in highly exposed occupations experienced up to a 16% decline in employment relative to established historical trends 2812. The technology sector has been particularly aggressive in this restructuring; for instance, UK tech companies slashed traditional graduate roles by 46% between 2023 and 2024, with projections suggesting a further 53% contraction by the end of 2026 21.

This contraction is not driven by a general economic recession, but by employers explicitly internalizing AI's capability to automate the routine, execution-based tasks historically assigned to junior staff. As companies deploy AI agents to handle basic research, document formatting, and initial coding, they no longer need to hire vast cohorts of recent graduates solely for task execution 2223. Instead, employers are now hiring for judgment, strategic context, adaptability, and complex human collaboration 23.

This structural shift has generated a profound psychological and practical crisis for recent university graduates. Extensive surveys conducted in 2026 reveal that an overwhelming 89% of new graduates explicitly fear that AI will replace entry-level jobs (a sharp increase from 64% in 2025), and 51% of young workers report high anxiety regarding their immediate job security 1314. A brutal paradox has emerged in early-career hiring: while employers are significantly reducing total entry-level headcounts due to automation efficiencies, over one-third of the remaining entry-level job descriptions now explicitly demand advanced AI skills 15. Consequently, young professionals are caught in a vicious structural bottleneck. They are required to possess advanced technological fluency and mature strategic judgment to secure the few remaining entry-level roles, yet they are systematically being denied the traditional, execution-focused stepping-stone positions that were historically required to cultivate that exact expertise.

Categorization of Roles: Displacement Risk vs. Augmentation Potential

The divergence between occupational displacement and labor augmentation is highly nuanced and sector-specific. Jobs defined primarily by repetitive information processing, rote data manipulation, and basic text synthesis face intense contraction. Conversely, roles that leverage AI to amplify complex decision-making, deeply empathetic interpersonal interaction, or intricate physical manipulation are expanding rapidly.

The following table categorizes specific occupational roles by their immediate risk of displacement versus their potential for AI-driven augmentation, reflecting verified 2025 - 2026 labor market realignments and the corresponding skills required to pivot into the augmentation category 14281630.

| Industry / Sector | High Displacement Risk (Task Automation) | High Augmentation Potential (Emerging/Evolving Roles) | Core AI Skills Required for Augmentation 153132 |

|---|---|---|---|

| Administrative & Clerical | Data Entry Clerks, Basic Bookkeepers, Executive Secretaries, Payroll Processors | AI Systems Integrators, Workflow Automators, AI Governance & Compliance Officers | AI Literacy, Workflow Automation (e.g., LangChain), Agent Configuration, AI Ethics |

| Technology & Engineering | Junior/Basic Coders, Routine QA Testers, Standard Tech Support Agents | MLOps Specialists, AI Ethicists, Human-AI Collaboration Specialists, Data Center Engineers | RAG (Retrieval-Augmented Generation), LLM Fine-tuning, Context Engineering, Deployment |

| Marketing & Content | Basic Copywriters, Routine Graphic Designers, Translators | Content Strategists, Prompt Engineers, Brand Voice Architects, AI Campaign Managers | Advanced Prompting (RTCROS framework), Context Layering, Creative Synthesis |

| Finance & Legal | Junior Analysts, Compliance Clerks, Paralegals (Document Review) | Strategic Advisors, Algorithm Auditors, Complex Negotiators, Risk Managers | Analytical Thinking, AI Risk/Security Auditing, Strategic Judgment, Business Process Alignment |

| Manufacturing & Trades | Assembly Line Workers (Routine Physical/Fixed Location) | Robotics Maintenance Techs, Digital Twin Specialists, HVAC Engineers, Grid Engineers | Predictive Maintenance interpretation, MLOps for physical systems, Power Electronics |

The Evolving AI Skill Set and the Human Premium

As demonstrated in the categorization above, the requisite technical skills for economic survival and career progression are shifting at an unprecedented velocity. In 2023 and 2024, basic "prompt engineering" was heralded as the definitive, future-proof AI skill. By 2026, raw, simplistic prompting has rapidly devolved in value as foundational AI models have become more intuitive and capable of understanding natural, unstructured language 15.

The most highly compensated and secure roles now demand expertise in highly specialized, second-generation AI disciplines. These include Context Layering and Engineering (the ability to provide LLMs with deep, proprietary institutional knowledge and nuanced operational constraints), Creating Skills for AI (building and packaging autonomous AI agents capable of executing complex, multi-step workflows with minimal human oversight), and MLOps (the deployment, maintenance, and continual monitoring of machine learning models at the enterprise scale) 153132. For example, the global market for Retrieval Augmented Generation (RAG) - a technique that grounds AI outputs in specific, real-time enterprise data - is projecting a staggering 49.9% compound annual growth rate, making it one of the most lucrative technical skills of 2026 33.

Furthermore, as AI rapidly commoditizes technical execution and basic analysis, the premium on durable "human" skills has skyrocketed. Organizations are increasingly selecting candidates based on critical thinking, complex stakeholder communication, emotional intelligence, and cross-disciplinary adaptability. Leadership recognizes that even the most advanced AI systems function optimally only when guided by nuanced human judgment, rendering hybrid professionals - those who blend AI literacy with high emotional intelligence - the most valuable assets in the 2026 labor market 233134.

The Global AI Divide: Advanced Western Economies vs. The Global South

While the macroeconomic and technological impacts of AI are inherently global, the distribution of its benefits and the severity of its disruptions are highly asymmetrical. Exhaustive data from the IMF, the World Bank, and the OECD reveals a rapidly widening structural chasm between the Global North and the Global South. This divide is primarily driven by vast disparities in foundational digital infrastructure, human capital readiness, R&D ecosystems, and the historical nature of local labor markets 41718.

The IMF AI Preparedness Index (AIPI)

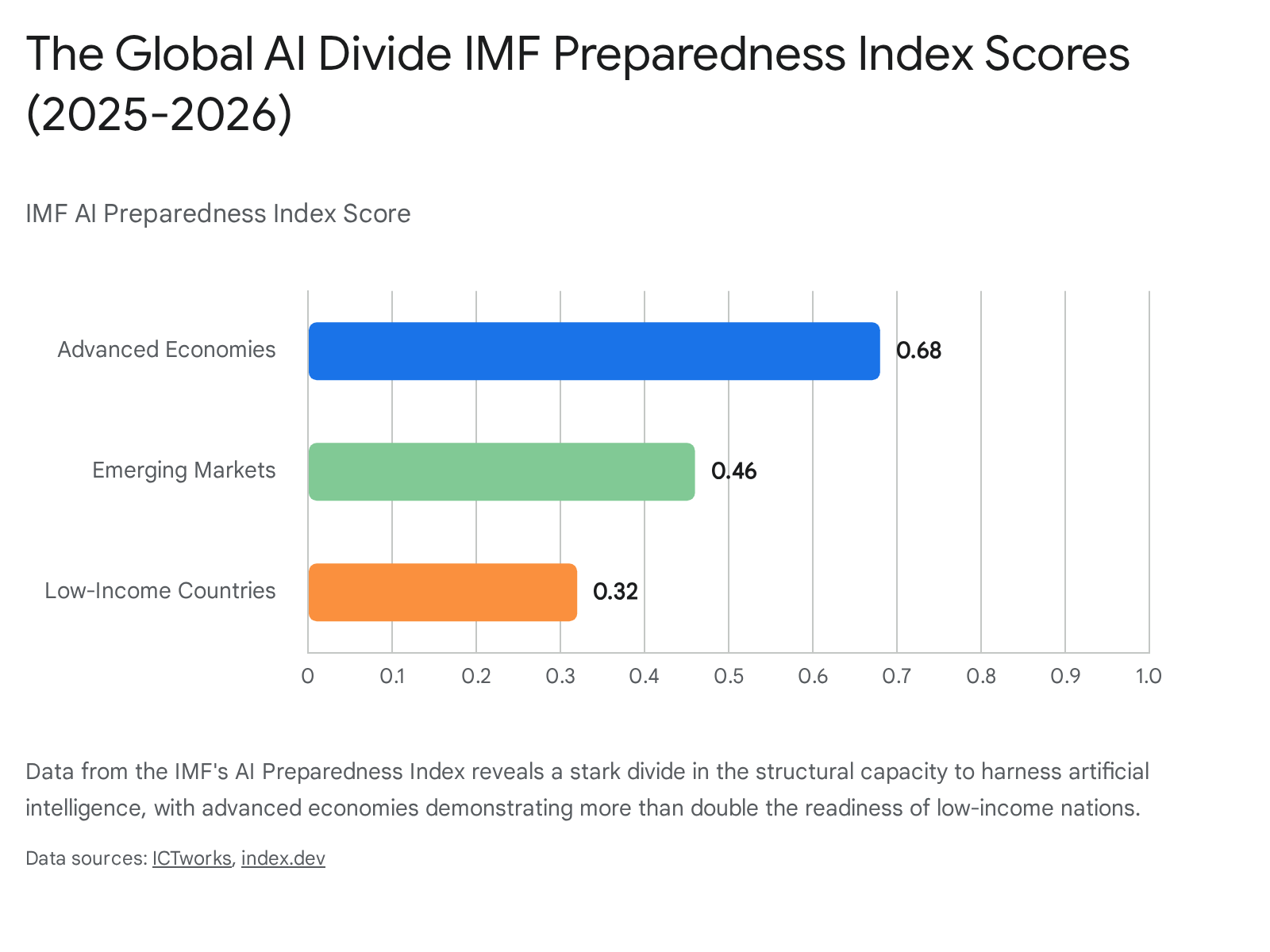

To quantify this disparity, the International Monetary Fund introduced the AI Preparedness Index (AIPI) for 2025/2026, which rigorously assesses 174 economies across four interdependent pillars: digital infrastructure, human capital and labor market policies, technological innovation and economic integration, and regulation and ethics frameworks 1920. The statistical disparities revealed by the AIPI are stark and concerning. Advanced Western economies currently average an AIPI score of 0.68, with nations like the United States, Singapore, South Korea, and the United Kingdom leading globally with scores frequently exceeding 0.79 739. In contrast, emerging markets average a score of 0.46, and low-income countries languish at a highly vulnerable 0.32 7.

In advanced Western economies, AI is largely viewed as a critical demographic counterweight and a catalyst for sustained economic dominance. Facing aging populations, shrinking active labor forces, and sluggish historical productivity growth, these economies view their high (60%) occupational exposure rate to AI not as a threat, but as a vital opportunity to sustain GDP growth despite severe demographic headwinds 40. In these regions, high AI adoption strongly correlates with significant wage increases in exposed sectors, as the labor force successfully pivots to complementary, higher-value tasks 2122. By late 2025, nearly 25% of the working-age population in the Global North was actively utilizing generative AI tools on a regular basis, further accelerating the region's technological diffusion and skill acquisition 23.

The Threat to the Global South's Traditional Development Model

Conversely, the Global South faces a multifaceted, existential economic crisis triggered by the AI revolution. The ILO and World Bank note that while approximately 40% of total global employment is exposed to AI disruption, in emerging markets, this exposure strikes directly at the heart of their traditional, proven development models 40.

For several decades, developing economies - most notably India, the Philippines, Kenya, South Africa, and Vietnam - successfully leveraged youthful demographic dividends and lower comparative labor costs to build massive Business Process Outsourcing (BPO) and IT service export sectors 22. These roles, which encompass call centers, basic data entry, junior coding, and routine back-office administration, represent the exact highly structured, routine cognitive tasks that Generative AI automates most efficiently and cost-effectively.

Over the next decade, while AI is unlikely to trigger immediate mass layoffs in the poorest regions (where informal, small-scale physical work still constitutes up to 61% of total labor), it severely and permanently truncates the traditional pathway from poverty to the formal middle class 22. Entry-level knowledge jobs will inevitably shrink, and global service supply chains will rapidly rewire as routine administrative work is either absorbed by intelligent algorithms or "reshored" back to leaner, AI-augmented, hyper-productive teams based in the West 22.

Furthermore, a massive infrastructure gap actively prevents the Global South from capitalizing on the productivity gains that AI offers. The IMF's AIPI exposes the reality that many developing nations lack the physical prerequisites to run modern AI. Sub-Saharan Africa, for instance, requires an estimated $418 billion in capital investment to achieve affordable universal broadband - representing 4.5% of regional GDP, compared to just 0.02% required in advanced economies 7. The challenge is compounded by prohibitive data costs (mobile data consumes roughly 20% of per capita income in Sub-Saharan Africa versus 1% in North America) and severe power grid constraints (only 22% of primary schools in the region have reliable access to electricity) 7. Additionally, R&D spending in emerging markets falls drastically below the 2-3% of GDP common in advanced economies, rendering the Global South entirely dependent on importing AI models embedded with Western cultural and operational biases 7. Without immediate, massive interventions in compute capacity, connectivity, and contextual data localization, the productivity gap between the digital "haves" and "have-nots" will inevitably widen, risking a severe exacerbation of global income inequality 72218.

The Corporate Governance Crisis: Bottom-Up "Shadow AI" vs. Top-Down Strategy

While macroeconomic data tracks aggregate, global employment shifts, the microeconomic reality occurring within individual enterprises is currently defined by a severe, escalating crisis of governance. The adoption of artificial intelligence in the modern workplace has fundamentally inverted the traditional paradigm of corporate IT rollouts. Historically, technology adoption was strictly top-down: executive management selected a tool, the IT department secured it, integrated it, and employees were formally trained on its usage. In 2026, AI adoption is aggressively bottom-up, driven primarily by individual employees seeking immediate, personal productivity gains in high-pressure work environments 2445.

The Rise and Risks of Shadow AI

"Shadow AI" refers to the unauthorized use of artificial intelligence tools, large language models, and AI-powered applications by employees without formal organizational approval, IT oversight, or adherence to corporate data governance frameworks 4647. Extensive 2026 workplace studies, including Lenovo's global survey of 6,000 employees, indicate that over 70% of global workers use AI tools weekly, with up to one-third doing so entirely outside the purview of their IT departments 5. Other security-focused studies, such as those from BlackFog, estimate that over 80% of workers globally engage in unapproved AI usage, and nearly 60% deliberately bypass enterprise-approved AI platforms in favor of free, public AI tools because they perceive them to be faster, more capable, or more accessible 4548.

Employees are driven to Shadow AI by immense corporate pressure to increase output and meet stringent deadlines. Roughly 60% of workers explicitly admit they are willing to accept the cybersecurity risks of unsanctioned AI if it accelerates their workflow, and teams utilizing Shadow AI report up to 40% faster initial task completion rates 454648. However, this pervasive "speed outweighs security" mindset creates catastrophic corporate vulnerabilities.

Unlike traditional "Shadow IT" (such as employees using unauthorized Dropbox accounts to transfer files), generative AI models inherently "learn" from input data. They possess the capability to retain, synthesize, and inadvertently regurgitate sensitive information. When employees upload proprietary software source code, unreleased financial forecasts, or highly regulated patient data into public LLMs to summarize or format it, they introduce severe risks of intellectual property leakage and massive non-compliance with stringent regulatory frameworks like GDPR or HIPAA 454647. High-profile incidents - such as engineers at Samsung leaking proprietary 3nm semiconductor code to ChatGPT, resulting in hundreds of millions in mitigation costs - underscore the severity of the threat 4625. Consequently, by 2026, the average financial cost of a shadow AI-related data breach has escalated to an astonishing $4.2 million per incident 45.

The Corporate Strategy Disconnect and the Two-Tier Workforce

Compounding the Shadow AI crisis is a profound, systemic failure in top-down corporate execution. Despite the fact that 90% of large enterprises have significantly increased their AI procurement budgets, 75% of executives privately admit in surveys that their corporate AI strategy is "more for show" than a set of actionable, integrated operational guidelines 924. Astonishingly, only 29% of companies currently report seeing a significant Return on Investment (ROI) from their official enterprise AI deployments 9.

This strategic vacuum has inadvertently birthed a fractured, "two-tier workforce" within most large organizations. On one end of the spectrum are the AI "laggards" - employees who remain overly cautious, rely solely on outdated workflows, and are passively waiting for formal corporate training that frequently never arrives. Current data shows that only 32% of employees receive formal, structured AI training from their employers, leaving the majority to navigate the technological shift independently 545.

On the opposite end of the spectrum are the "super-users." Representing approximately 40% of employees in core knowledge functions (marketing, sales, HR), these proactive individuals have independently mastered advanced AI workflows, built custom agents to automate their specific tasks, and entirely bypassed sluggish IT bureaucracies 9. The economic advantage enjoyed by these super-users is immense: they report saving nearly 4.5 times as much time each week compared to laggards, and they are up to three times more likely to receive both promotions and significant pay raises 9. The defining operational challenge for C-suite leadership in 2026 is bridging this dangerous divide. Organizations must transition away from rigid, reactive, and ultimately futile prohibitions of Shadow AI, and instead implement adaptive, secure governance frameworks that actively institutionalize the workflow innovations pioneered by their rogue super-users.

The Psychological Toll: Worker Sentiment vs. Leadership Priorities

The acute disconnect between bottom-up AI adoption and top-down corporate strategy is starkly mirrored in the profound dissonance between how frontline workers and organizational leaders perceive the ongoing AI transition. While institutional economics focuses broadly on metrics like productivity enhancements and TFP growth, sociological data derived from comprehensive 2025 - 2026 workplace surveys reveals a global workforce operating under immense, escalating psychological strain.

A marked, highly consequential shift occurred in public sentiment between 2024 and 2026 regarding AI optimism. In 2024, a solid plurality of workers believed AI would ultimately do more good than harm for society and their careers. However, by early 2026, that sentiment had completely inverted: 44% of workers now believe AI is doing more harm than good, compared to only 38% who still view it as a net positive 26. Furthermore, overall optimism about AI's positive impact on workers specifically plummeted by 10 percentage points over a single year, dropping to a mere 39% 26.

The following table contrasts the lived realities and immediate, visceral concerns of the workforce against the strategic priorities and frequent blind spots of executive leadership. This synthesis is derived from major 2025 - 2026 workplace barometers, including expansive surveys conducted by PwC, McKinsey, SHRM, Beautiful.ai, Mercer, and Jobs for the Future (JFF) 2627532829.

| Dimension | Worker Sentiment & Immediate Concerns | Leadership Priorities & Strategic Perspectives | The Resulting Organizational Disconnect |

|---|---|---|---|

| Primary Utility & Goal of AI | Survival & Workload Management: Workers utilize AI primarily to cope with perceived massive increases in workload (64% report significantly heavier workloads) and to avoid falling behind peers in a hyper-competitive environment 2430. | Efficiency & Productivity Scaling: 77% of managers and executives adopt AI tools specifically to enhance worker productivity, improve operational efficiency, and drive higher baseline output 5357. | Leaders fundamentally view AI as a tool to continuously expand capacity and output; workers view it as a desperate lifeline to manage existing burnout. Consequently, efficiency gains are often absorbed by higher quotas rather than shorter hours. |

| Job Security & Wages | High & Escalating Anxiety: 70% of managers believe employees fear AI will eventually lead to them being fired (a 12% increase from 2025). Moreover, 52% of managers now fear AI will depress their own managerial wages 5328. | Reorganization over Downsizing: Only 9% of leaders cite direct downsizing or saving money on salaries as the primary goal of AI. Most prefer internal mobility, redeploying staff from automated tasks to higher-value functions 3053. | A severe, systemic communication failure. While mass layoffs aren't the primary corporate intent for existing staff, the lack of transparent, guaranteed AI roadmaps leaves employees assuming the absolute worst regarding their financial security. |

| Skills & Competency Development | Fear of Professional Obsolescence: 37% of employees worry that an overreliance on AI will erode their foundational expertise 30. Only ~35% feel their employer provides the adequate training needed to adapt 26. | Assumed Readiness & Delegated Responsibility: Leaders significantly underestimate employee readiness while simultaneously failing to provide adequate, structured, enterprise-wide training pipelines 5. | Employees are forced into highly stressful, self-directed learning (fostering dangerous Shadow AI usage), while leaders wait for enterprise-wide ROI that cannot possibly materialize without structured, systemic upskilling. |

| Overall Sentiment & Cultural Health | Growing Pessimism & Alienation: Only 39% feel optimistic about AI's impact. Women (49% net negative) and early-career workers report the absolute highest levels of pessimism and career disruption 26. | Aggressive Market Optimism: Leaders face intense, unrelenting pressure from boards and financial markets to deploy capital into AI, maintaining high public optimism regarding long-term disruption and competitive market share 2729. | Executives risk aggressively pushing transformative, high-stress AI initiatives onto a psychologically fragile and deeply cynical workforce, leading to severe resistance, disengagement, and sub-optimal technological integration. |

The aggregated data emphatically reveals that the speculative "uncertainty phase" of artificial intelligence has ended; workers now clearly comprehend AI's practical capabilities and have deeply internalized the associated economic and professional threats 53. To harness AI's full macroeconomic potential without fracturing fragile corporate cultures, human resources departments and executive leadership must urgently pivot their focus. Procuring software is no longer the primary challenge; aggressively managing the human transition is. Radical transparency regarding future compensation models, explicit corporate guarantees detailing how AI-driven efficiency will be financially rewarded (rather than penalized via job cuts or stagnant wages), and the total restructuring of career development ladders for junior talent are paramount for organizational survival in 2026 28.

Conclusion

The future of work in 2026 is defined not by the apocalyptic eradication of human labor, but by its radical, high-velocity, and often painful structural reallocation. Generative AI has unequivocally proven its capacity to automate routine cognitive tasks, permanently collapsing the traditional boundaries of white-collar professional progression and placing intense, unprecedented pressure on entry-level hiring and recent university graduates. Concurrently, the massive physical and energy demands of computing infrastructure have revitalized skilled blue-collar trades, entirely flipping historical economic assumptions about which demographics are most vulnerable to technological disruption.

However, recognizing that the "lump of labor" fallacy is indeed an economic fallacy does not negate the acute, localized transitional pain currently experienced by the global workforce. While structural macroeconomic models correctly project aggregate productivity gains, Total Factor Productivity growth, and eventual net job creation, these benefits are neither geographically, demographically, nor socioeconomically uniform. Advanced Western economies are uniquely positioned to reap the benefits of AI to offset their aging populations, while the Global South faces the perilous, immediate erosion of its traditional service-export development models due to stark, systemic deficits in digital infrastructure and capital investment.

Within the modern enterprise, the unchecked, exponential proliferation of "shadow AI" exposes a critical, perhaps fatal, lag in institutional governance. Companies are currently capturing efficiency gains almost exclusively through the decentralized, unauthorized ingenuity of rogue "super-users," while simultaneously incubating immense cybersecurity risks and alienating the broader, unsupported workforce.

To navigate the remainder of the decade successfully, a profound paradigm shift in both global public policy and corporate strategy is strictly required. Policymakers must focus aggressively on international digital infrastructure equity and championing adaptive education models that emphasize complex human reasoning, contextual synthesis, and emotional intelligence over rote execution. For corporate leadership, the mandate is equally clear: artificial intelligence strategy can no longer be relegated strictly to the IT procurement department. It must be seamlessly embedded into the very core of human capital strategy, prioritizing secure, adaptive governance, proactive and continuous upskilling, and psychological safety to ensure the global workforce is elevated - rather than exhausted and discarded - by the algorithmic era.