Creator Economy Size Income Distribution and Sustainability in 2026

Macroeconomic Environment and Market Valuations

The global creator economy operates within a broader macroeconomic environment that has demonstrated significant resilience heading into 2026. According to early 2026 analyses by major financial institutions, including Citigroup and Barclays, the global economy has absorbed persistent inflation, elevated energy costs, and geopolitical supply chain disruptions while maintaining steady growth 123. Corporate profitability remains robust, buoyed by accommodative monetary policies and targeted fiscal easing in the United States and Europe 14. A critical driver of this resilience is an acyclic capital expenditure cycle, heavily weighted toward artificial intelligence and technology infrastructure, with top technology firms on track to spend approximately $700 billion on capex in 2026 2.

This favorable macroeconomic backdrop provides a solid foundation for digital advertising and the creator economy. Influencer marketing and creator-led campaigns have transitioned from experimental digital tactics into core infrastructure components of global marketing strategies 56. Chief Marketing Officers increasingly demand the same rigor, repeatability, and measurable performance from creator partnerships as they do from search and programmatic advertising 57. Consequently, global influencer marketing spend reached $32.55 billion in 2025, a 35.6% year-over-year increase, with projections indicating it will surpass $40.51 billion by the end of 2026 69. In the United States alone, creator ad spend is forecasted to hit $43.9 billion in 2026 78.

Total Addressable Market Estimates and Projections

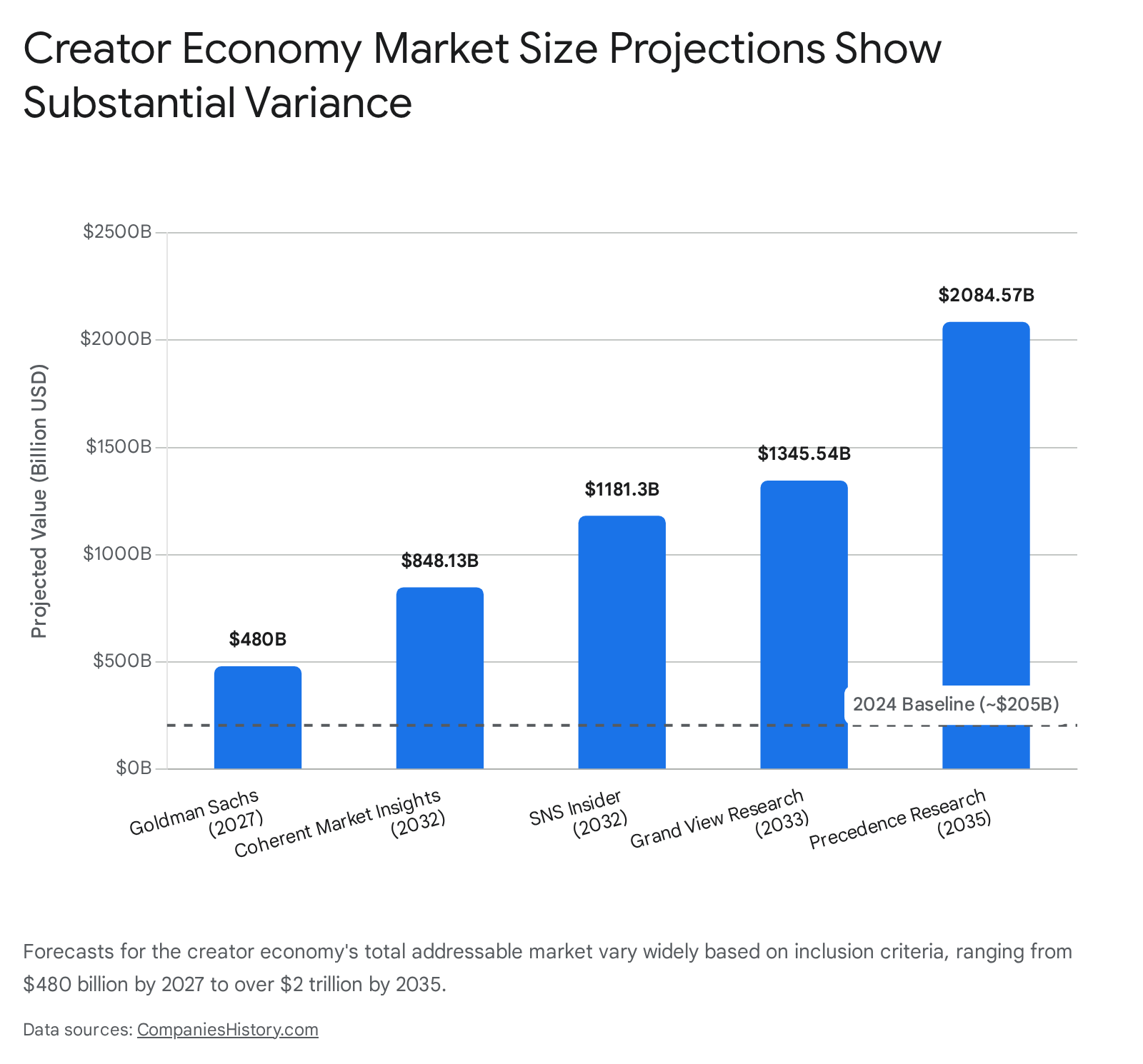

As institutional capital flows into the sector, the overall valuation of the creator economy has scaled dramatically. Aggregate data from major market research institutions places the baseline value of the global creator economy between $205.25 billion and $214.37 billion as of 2024, with estimates for 2025 settling in the $234.65 billion to $254.4 billion range 6910141112.

Projections for the sector's long-term total addressable market point to sustained, aggressive expansion, characterized by compound annual growth rates consistently reported between 22.4% and 26.5% 1112131415. Goldman Sachs Research offers one of the more conservative near-term models, projecting the total addressable market will approach $480 billion by 2027 67132016. Conversely, maximalist forecasts from firms such as Precedence Research and Coherent Market Insights project the sector will breach the $1 trillion threshold by the early 2030s, potentially reaching $1.35 trillion to $2.08 trillion by 2035 699111420.

Methodological Critiques of Valuation Models

The sheer scale of these trillion-dollar projections necessitates a critical examination of market sizing methodologies. Independent analysts observe that maximalist valuations often conflate distinct economic layers, resulting in a potentially inflated representation of creator prosperity 1723.

Historically, creator economy market sizing was limited to direct creator income, such as brand deals, platform advertising payouts, and direct subscriptions 17. However, the $314 billion to $1 trillion forecasts circulating in 2026 rely on a maximalist definition that bundles direct creator income with downstream digital commerce, such as the gross merchandise value processed through TikTok Shop or affiliate networks, as well as the overarching software-as-a-service infrastructure 17. This infrastructure layer encompasses creator tooling platforms, talent management agencies, venture-backed fintech payment processors, and analytics software 1617.

Funding deals targeting creator-economy infrastructure crossed $670 million in the twelve months leading up to April 2026, with average funding rounds exceeding $42 million 17. By absorbing the enterprise value of these software vendors into the total addressable market, researchers present an industry characterized by staggering wealth 23. Yet, this methodology obscures the fact that the platform and infrastructure layers are capturing an increasingly dominant share of the revenue 2318. The assumption embedded in maximalist reporting is that platform growth inevitably lifts all creator incomes 23. In reality, the capitalization of the infrastructure layer often outpaces the aggregate wage growth of the creators supplying the foundational labor 2318.

Creator Workforce Demographics and Income Distribution

Workforce Scale and Professionalization

The global population of content creators has expanded rapidly, moving well beyond the industry's early "side hustle" origins. In 2026, over 207 million individuals globally identify as content creators across various digital platforms 6101213. YouTube alone hosts approximately 61.8 million creators, while Instagram and TikTok support 64 million and tens of millions of monetizing accounts, respectively 619.

Within this massive cohort, an estimated 45 million to 50 million individuals operate as professional or semi-professional creators, treating content generation as their primary business venture rather than a casual hobby 10141220. In the United States, there are currently 27 million paid creators, representing 14% of the population aged 16 to 54 13. This domestic workforce features distinct operational tiers: 44% function as full-time content creators (approximately 11.6 million people), 32% operate on a part-time gig basis (8.5 million), and the remaining 24% identify as hobbyists (6.5 million) 13. The professionalization of the sector is further evidenced by shifting attitudes toward the work; only one in ten creators globally view their content strictly as a hobby, signaling a broad recognition of digital content as an active entrepreneurial pursuit 1321.

Income Disparities and the Power Law

The distribution of capital within the creator economy is characterized by severe structural inequality, following a steep power law where a fractional minority captures the vast majority of available revenue 91822. Despite the macro-valuations of the industry, the median financial reality for the individual creator remains precarious.

Data for the 2025 and 2026 periods reveals that between 48.7% and 50% of all creators earn less than $15,000 annually, a metric that has slightly increased from previous years as the influx of new market entrants outpaces the expansion of available advertising inventory 6723. Furthermore, 73% of creators report annual earnings below $30,000, placing the majority of the workforce beneath professional living wage thresholds in developed economies 22. The concentration of capital is particularly acute in advertising revenue; in 2025, the top 10% of creators captured 62% of all ad payments, while the top 1% secured 21% of the total volume 1622.

Conversely, the industry is witnessing the gradual formation of a "creator middle class." Currently, 45.6% of active creators earn between $10,000 and $100,000 annually 723. Only an estimated 4% to 5.7% of creators globally manage to surpass the $100,000 annual income threshold, effectively establishing the boundary for high-tier professional viability 671322.

| Annual Income Bracket | Estimated Share of Creator Population | Contextual Insight |

|---|---|---|

| Under $15,000 | 50.0% | Represents the baseline majority; median global earnings sit near $3,000 annually. 6722 |

| $10,000 - $100,000 | 45.6% | The emerging middle tier; requires multifaceted monetization beyond standard ad revenue. 723 |

| $100,000 - $150,000 | 9.7% | High performers; typically reliant on 3 or more distinct, owned revenue streams. 6 |

| Over $200,000 | 5.7% | Enterprise-level creators; functions as independent media holding companies. 67 |

Note: Data derived from aggregated 2025/2026 industry surveys. Bracket overlaps reflect statistical variances in reporting methodologies across differing platform ecosystems 6723.

Algorithmic Precarity and Labor Dynamics

The structural disparities in income are compounded by the fundamental nature of platform-based labor. Academic and labor policy analyses, including the American Influencer Council's 2026 "Creator Labor Gap" report, frame content creators as a massive independent workforce operating entirely without traditional job security, collective bargaining mechanisms, or employer-sponsored health and retirement benefits 93024.

Creators function within privatized digital infrastructures where algorithms, monetization eligibility, and content visibility are unilaterally governed by technology conglomerates 924. Because engagement-based algorithms are engineered to maximize consumer watch time and ad inventory, creators are subjected to a continuous production cycle. This dynamic systematically blurs the boundaries between life and work, normalizing extreme precarity and chronic fatigue 7925. In 2026, 62% of full-time creators reported experiencing clinical or sub-clinical burnout, largely driven by the psychological pressure of algorithmic volatility and the constant threat of shadowbanning or sudden drops in reach 726.

Further embedding this inequality is a persistent gender pay gap within the digital ecosystem. While female creators represent approximately 70% of the active influencer market and dominate highly profitable lifestyle and consumer sectors, male creators continue to command significantly higher compensation 2224. In 2025, male creators earned an average of $69,922 annually, nearly double the $37,065 average reported by female creators 622. Male creators also secure a 40% premium per brand collaboration, indicating systemic undervaluation of female-led content within corporate influencer marketing budgets and algorithmic ad-bidding auctions 22.

Platform Monetization Mechanics and Unit Economics

Advertising Revenue Shares and Yield Variability

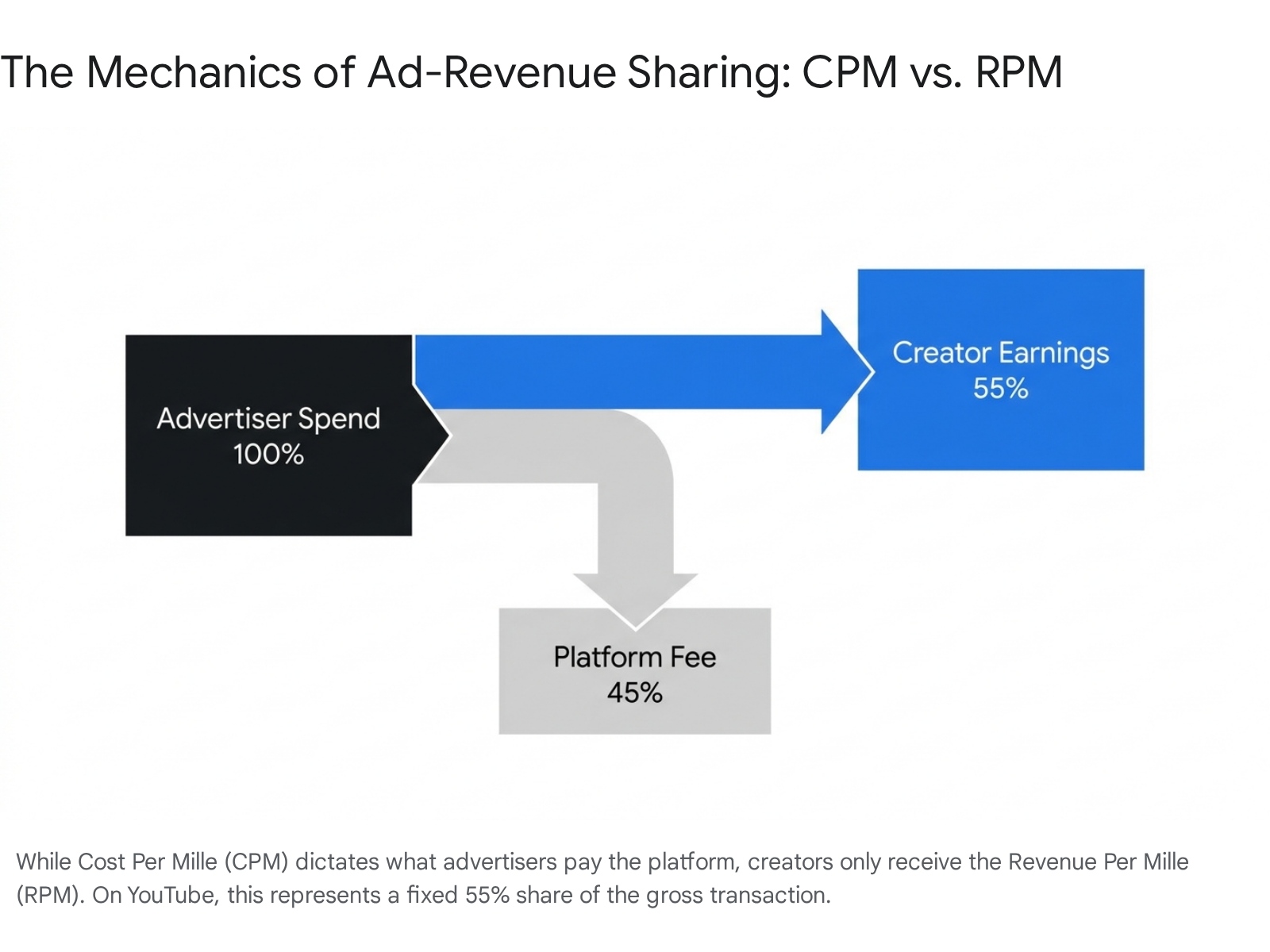

For the first decade of the creator economy, advertising revenue-sharing programs functioned as the primary, and often sole, mechanism for creator compensation. In 2026, YouTube remains the premier platform for ad-revenue sharing through its Partner Program, maintaining a standard 55/45 split model where the creator retains 55% of the advertising revenue generated against their content, while Google retains 45% 18272829.

However, raw view counts provide a highly distorted picture of actual creator income. Compensation is governed by the metric RPM (Revenue Per Mille), which isolates the net take-home pay a creator receives per 1,000 views after the platform extracts its 45% cut and after accounting for non-monetized views 282930. RPM acts as a volatile market clearing price, fluctuating heavily based on seasonal advertiser demand, the format of the content, the specific niche, and the geographic location of the audience 2938.

For instance, a creator operating within the personal finance or enterprise technology niche can command premium RPM rates ranging from $9 to $11, as advertisers for high-margin financial products or software bid aggressively for access to that specific demographic 2829. A finance channel accumulating 500,000 monthly views could realistically net between $7,000 and $9,000 per month from AdSense 2829. Conversely, an entertainment or gaming channel - which typically attracts a younger or broader demographic - might yield an RPM of just $1 to $3. The same 500,000 views would generate only $1,200 to $1,500 282930. Audience geography serves as the most rigid determinant of RPM; viewership originating from emerging markets such as India, Indonesia, or Nigeria typically generates a fraction of the ad rates seen in the United States, often yielding multipliers as low as 0.15x to 0.30x of Western rates 2930.

Direct Subscription Models and the Platform Tax

Recognizing the volatility of algorithmically driven advertising, creators are aggressively migrating toward recurring, direct-to-consumer subscription models 101726. Substack, Patreon, and community platforms like Circle have normalized the concept of paying directly for niche expertise and parasocial access 182631.

On Substack, the mathematics of the subscription model present a compelling alternative to ad dependency. A creator charging a standard rate of $5 per month to 1,000 dedicated subscribers generates a gross monthly revenue of $5,000 31. Substack extracts a flat 10% platform fee, while payment processor Stripe levies approximately 2.9% plus a $0.30 fixed fee per transaction 3132. After factoring in a secondary billing fee for newer subscribers, the total platform tax amounts to roughly 13% to 16% 3132. The creator nets approximately $4,325 per month, equivalent to nearly $52,000 annually - a full-time median wage secured without requiring millions of passive views 31.

However, the fixed-percentage fee structure becomes increasingly punitive as creators scale their operations. A creator grossing $50,000 per month surrenders $5,000 monthly simply to host a newsletter and manage a subscriber list 32. Consequently, many mid- to high-tier creators eventually migrate to fixed-cost Software-as-a-Service (SaaS) providers. Platforms such as Beehiiv offer flat monthly rates starting around $43, allowing creators to keep 100% of their subscription revenues, substantially improving unit economics at scale 32.

Digital Product Commerce and Infrastructure Costs

Digital products - encompassing eBooks, downloadable software templates, aesthetic presets, video courses, and high-ticket B2B consulting packages - now represent the most reliable and fastest-growing monetization pathway for independent creators 2641. By selling owned digital assets, creators capture aggressive profit margins of 70% to 90%, bypassing platform ad-revenue splits and the complex negotiations required for brand sponsorships 41. In 2026, 67% of monetizing creators rely on digital products for a portion of their income 41.

The infrastructure facilitating these transactions varies significantly in cost and capability. Gumroad, historically the dominant entry-level marketplace for digital downloads, operates on a zero-upfront-cost model, instead extracting a flat 10% platform fee (which includes payment processing) plus a fixed $0.50 transaction charge 4243. This structure removes all financial barriers to entry, making it highly attractive for creators testing their first products 4243. Yet, as with Substack, the percentage-based fee acts as a regressive tax on growth. Industry analysts identify a "Gumroad cliff" that occurs when a creator reaches between $2,000 and $5,000 in monthly revenue; at this threshold, surrendering 10% becomes mathematically inefficient 43.

For course creators and knowledge entrepreneurs scaling beyond initial sales, platforms like Kajabi and Teachable offer more robust alternatives. Teachable targets the mid-market, offering entry plans at $39 per month, though it retains a 5% transaction fee on lower-tier accounts 33453447. Kajabi, positioning itself as a premium, all-in-one operating system, charges a flat fee beginning at $149 per month with strictly zero transaction fees across all tiers, integrating native payment gateways, email marketing, and affiliate management directly into the backend 33344735.

| Digital Commerce Platform | Primary Value Proposition | 2026 Pricing and Fee Structure | Target Creator Demographic |

|---|---|---|---|

| Gumroad | Instant deployment of digital product storefronts. | 10% flat fee per transaction (inclusive of payment processing) + $0.50. | Early-stage creators testing products with zero upfront financial risk. 4243 |

| Teachable | Dedicated, user-friendly course hosting and learning management. | $39/month baseline; 5% transaction fee on basic plans, 0% on Pro tiers. | Course creators seeking advanced LMS features without enterprise-level SaaS costs. 453447 |

| Kajabi | Comprehensive business operating system (marketing, courses, funnels). | $149/month baseline; 0% transaction fee across all plans. | Established knowledge entrepreneurs managing multi-product digital businesses. 333435 |

| Beehiiv | Fixed-cost newsletter publishing and subscription management. | Flat monthly SaaS fee (e.g., $43/month); 0% revenue share. | Scaling writers seeking to avoid the percentage-based "platform tax" of competitors. 32 |

Market Expansion in Developing Regions

While North America accounts for approximately 33% to 40% of the global creator economy, growth rates have stabilized. The fastest expansion is occurring in emerging markets across Africa, Latin America, and the Asia-Pacific, fueled by rising smartphone penetration, youth demographics, and increasing digital connectivity 61112141536.

Structural Challenges in the African Creator Economy

The African creator economy represents a massive but structurally hindered market, currently valued at roughly $3 billion with projections to reach $17.8 billion by 2030 2137. Despite commanding enormous regional and diaspora audiences, African creators operate within an ecosystem heavily excluded from direct platform monetization 513853.

Global technology platforms have historically designed their monetization parameters - including eligibility thresholds and payout infrastructures - around Western markets where advertising yields are highly concentrated 3839. In 2026, TikTok's Creator Rewards Program explicitly excludes creators in major African digital hubs such as Nigeria and Kenya 3839. Instagram's native monetization features, including Subscriptions and Reels Bonuses, are largely inaccessible across the continent, while X's Creator Revenue Sharing model lacks support for most African banking jurisdictions 38. Furthermore, even on platforms where monetization is technically available, such as YouTube, the domestic RPM payouts are fractions of pennies compared to Western equivalents due to the lower purchasing power of local advertisers 3839. Consequently, survey data reveals that approximately 60% of African creators earn less than $100 per month directly from their creative output 2153.

To survive these systemic barriers, African creators have engineered a robust "workaround economy" 38. Rather than waiting for platform integration, creators rely primarily on direct brand sponsorships - which historically accounted for up to 60% of top-tier revenue - and direct-to-consumer digital product sales 213738. This shift toward "creator commerce" is facilitated by regional fintech solutions such as Paystack and Flutterwave, which enable secure processing of local currencies (Naira, Cedis, Rand, Shillings) for digital downloads and consulting services 3940. Additionally, new financial infrastructure platforms like Spondula and OneDosh have emerged, providing borderless digital wallets and S-handles that allow creators in Lagos or Nairobi to collect payments directly from global audiences without the complex legal requirement of incorporating a United States-based LLC 3841.

African creators also utilize strategic geographic targeting. An analysis of the "Audience Anchor Ratio" (AAR) demonstrates that top creators in Nigeria and South Africa function as highly efficient export engines 53. By optimizing their content language, subtitling, and thematic relevance, these creators purposefully capture viewership in high-RPM Western markets, successfully converting local production into global, high-yield revenue streams 53.

Social Commerce Integration in Latin America and Asia

In regions featuring deeper integration between digital content and native e-commerce, the creator economy is fundamentally reshaping traditional retail. Latin America, propelled by Brazil, is experiencing rapid adoption of creator-led live commerce. E-commerce giant Mercado Libre committed a record $11 billion investment in Brazil for 2026, explicitly aimed at expanding its proprietary logistics networks and its fintech arm, Mercado Pago 574243. This infrastructure investment is designed to capture the transaction volume generated by social commerce, providing the fulfillment speed and credit access required to convert creator influence into immediate physical sales 574244.

Similarly, platforms in Asia demonstrate the commercial efficiency of bridging content and retail. Xiaohongshu (RedNote), a Chinese lifestyle and social commerce platform boasting over 300 million monthly active users, operates seamlessly as both a peer-to-peer recommendation network and a direct e-commerce storefront 4562. To aggressively capture market share and incentivize creator-led brands, Xiaohongshu introduced a policy waiving all commissions on the first 1 million RMB in sales per merchant from September 2025 through August 2026, applying only a nominal 0.6% payment processing fee 454647.

Concurrently, Chinese video-sharing platform Bilibili optimized its creator revenue-sharing models while deploying AI-generated advertising tools to better match creators with brands. This strategy yielded a 27% year-over-year increase in advertising revenues in late 2025 and early 2026, driving the company's adjusted net profit margins to 10.6% and proving the viability of deeply integrated, creator-subsidized commercial ecosystems 484950.

Strategic Pathways to Financial Sustainability

As the creator economy matures, the original influencer paradigm - characterized by the pursuit of viral vanity metrics and a precarious reliance on ad-hoc brand sponsorships - is being systematically replaced by rigorous small business fundamentals. Sustainability in 2026 is defined by operational independence and revenue control.

Revenue Diversification and the Holding Company Model

The correlation between financial sustainability and revenue diversification is absolute. Creators who rely exclusively on a single monetization channel, such as platform ad-revenue or singular brand deals, remain acutely vulnerable to algorithmic shadowbanning, shifting platform policies, and economic downturns in advertising budgets 641. In 2025, creators maintaining three or more distinct revenue streams earned an average of $75,000 more annually than those operating single-stream businesses 6.

The most successful creators are abandoning the concept of a "channel" entirely, evolving instead into micro-media holding companies 51. These entities leverage their initial audience trust to launch standalone consumer packaged goods, proprietary software tools, specialized newsletters, and premium educational cohorts 131851. By shifting the economic relationship from an indirect sale (renting attention to a third-party brand) to a direct sale (selling owned products directly to a loyal community), creators insulate themselves from the volatility of algorithmic reach 172351.

The Ascendance of Mid-Tier Creator Influence

Simultaneously, the corporate approach to creator partnerships has matured. Marketers have largely determined that investing millions in mega-celebrities or macro-influencers often yields diminishing returns regarding active consumer conversion. In 2026, the performance "sweet spot" for brand capital lies firmly with mid-tier creators - channels possessing between 100,000 and 500,000 highly engaged, niche subscribers 8283051.

These mid-tier entities offer vastly superior engagement rates (averaging 4% to 8%, compared to the 1% to 2% typical of macro-influencers), maintain reliable, professional production schedules, and provide access to highly targeted, high-intent consumer demographics 2051. Consequently, brand collaborations have evolved from transactional shout-outs into complex, performance-based marketing infrastructure deals, increasingly managed through automated creator project management platforms rather than manual agency spreadsheets 5651.

Artificial Intelligence and Operational Automation

The widespread adoption of artificial intelligence is the final pillar enabling creator sustainability in 2026. Rather than threatening to replace the human creators who hold parasocial trust, generative AI has become a mandatory operational force multiplier. According to industry surveys from late 2025 and early 2026, between 86% and 91% of professional creators now actively utilize AI tools 9751.

These technologies are deployed across the backend of the business: generating A/B tested thumbnails, outlining scripts, translating audio for global syndication, automating video editing cuts, and analyzing audience retention data 235152. By minimizing the labor hours traditionally lost to operational friction, automation effectively closes the production gap between independent solopreneurs and heavily capitalized media corporations 23. This efficiency allows creators to reallocate their limited labor capacity toward high-value activities - deepening community relationships, developing owned digital products, and executing long-term business strategies 265152.

Ultimately, the creator economy of 2026 has shed its gold-rush mythology. It is a highly competitive, structurally unequal, yet deeply entrenched macroeconomic sector where financial survival requires creators to transition from being mere tenants of platform capitalism into definitive owners of their own digital infrastructure.